Oil prices have rallied 80% since the middle of February, but the recovery seems to have come too late for many US and Canadian energy firms struggling to survive a global supply glut that has destroyed the business plans of much of the industry.

Bankruptcies have surged over the past few months, and are now coming at the rate of about three a week – triple the rate seen last year. And many big names are joining the list of casualties: Linn Energy and SandRidge Energy, for example, both filed for bankruptcy in recent days.

But the rise in bankruptcies isn’t all it seems. Few of the companies have been pushed to the wall because they can’t pay their debts. Rather, management and creditors are using the process as a tactic of one-upmanship over rivals or to oust other stakeholders.

“Very few of these companies are coming up against billion-dollar maturities,” said Brad Bell, an oil and gas analyst at Fitch Ratings. “Management is looking around seeing rivals emerge from bankruptcy in much better shape, and they don’t want to get left behind.”

Those seeking bankruptcy are taking advantage of two shifts in the industry in recent months: first, stigma around such moves is much diminished after 42 filings last year; and second, after two years of lower oil prices, fatigued creditors are more willing to take losses.

“Many banks and investors have just run out of patience,” said John Grieve, chair of the restructuring group at Canadian law firm Fasken Martineau. “They recognise that many of these companies still aren’t going to be profitable even with oil as high as US$70. They want to cut their losses and move on.”

Worst month

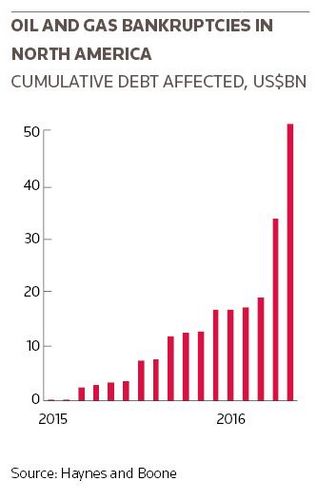

Some 35 companies have filed for bankruptcy this year, compared with 42 during the whole of 2015. Eight companies owing US$18bn have filed already this month, and May is in fact set to go down as the worst for filings in this downturn.

Linn, with just under US$6bn of debt, is so far the biggest bankruptcy. The shale oil and gas producer operates in California, Wyoming and North Dakota and has tapped capital markets several times since its US$247m IPO in 2006, issuing equity and bonds.

“Very few of these companies are coming up against billion-dollar maturities. Management is looking around seeing rivals emerge from bankruptcy in much better shape, and they don’t want to get left behind”

Under its restructuring plan, it intends to spin off Berry Petroleum, which it bought three years ago, and agree on a reduction in its debt load. The plan has the backing of senior creditors, but most junior creditors appear to have rejected the restructuring.

SandRidge, which produces oil and gas in the Oklahoma and Kansas shale fields, plans to swap about US$3.7bn of debt into equity. The proposal has the backing of the vast majority of senior lenders and bondholders, and just over half of unsecured noteholders.

“The stigma is gone: management in many of these companies is taking the view that this is the right time to file,” said Bell. “There is little to lose: very few of them are stepping down, and in many cases they are seeking significant equity stakes in the restructured business.”

Creditors are also keen to sort out the struggling companies. Banks, under pressure from regulators to avoid another financial mess, have provisioned heavily and want to draw a line under their losses before matters get worse.

Other creditors also see the potential to muscle out other stakeholders.

“There are also some opportunists, particularly among senior creditors, who see a chance to squeeze out equity and unsecured investors,” said Grieve. “They could end up owning most of a very good company in an environment where things are coming back.”

Exponential expansion

Whatever the driver, this latest increase in bankruptcies will result in big losses for many equity and bondholders that helped fund the exponential expansion of the North American oil and gas industries over the past decade.

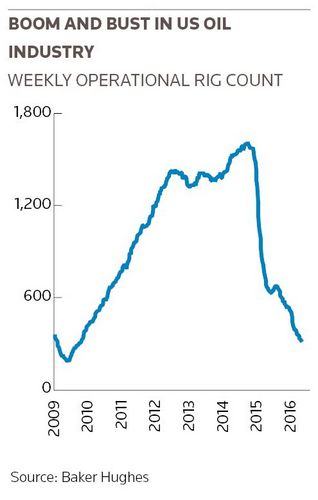

The industry has issued more than US$200bn of stock over the past five years, according to IFR calculations. In addition, it has printed more than US$250bn of high-yield bonds. The capital infusion helped fund an almost ninefold increase in the number of US oil installations between mid-2009 and mid-2014, when oil prices began to sink.

Oil prices tumbled to as low as US$26 in February, a quarter of the level two years earlier. In response, many energy producers simply stopped production and mothballed equipment. More than 80% of oil rigs in the US have ceased production since October 2014.

“Banks and capital markets just got overheated,” said Buddy Clark, a partner at Haynes and Boone in Houston. “Clearly there were a lot of dollars chasing deals. After the good deals got funded, they chased so-so deals and then bad deals which have gotten hit.”

The hope is that, once balance sheets are cleaned up, healthier companies will regain access to capital markets.

“Oil is part of life, we need it – if not for the next 100 years, then at least for the next 50,” said Grieve. “Access to capital will come back, but investors will be less zealous. They were just too eager to invest in the industry, and that is now gone.”