Investors waited decades for a turnaround in the German property market. But when it finally came in 2011, after more than 20 years of price declines, many couldn’t scramble together the cash to snap up bargains. Banks, their main source of finance, were too busy just trying to survive: the trough in German real estate had coincided with the peak of the eurozone crisis.

Aroundtown, set up seven years earlier by Israeli banker Yakir Gabay, who had moved to Germany to take advantage of rock-bottom property prices, was one of those caught out. As the market turned, it pushed on with the purchase of properties it had been eyeing. But its banks, preoccupied with the unfolding crisis, were unable to sign off on loans quickly enough.

“There were many opportunities, but the banks were slow … it was taking too long,” recalled one Aroundtown board member, who said that the experience pushed the company into exploring other sources of funding. “We realised in 2011 that the right thing was to approach the capital markets, get a rating so you can issue bonds and not rely solely on the banks.”

Within months, Aroundtown had spun off its residential business into a new company called Grand City Properties. It listed the subsidiary the following May, and followed up two months later with its first capital raise: new shares, equivalent to 10% of the company, were sold for €15m. More deals followed: €100m of convertible bonds in October, €36m of equity in February, and €200m of bonds the following July.

PROLIFIC ISSUER

Six years later, the deals keep on coming. Grand City and parent Aroundtown – which was listed in 2015 – have since racked up 50 bond and equity deals to raise more than €16bn, making them two of the most prolific issuers in Europe. And the pace shows no sign of slowing: this year alone, they have raised more than €2bn, including bond deals in markets as far afield as Australia and Hong Kong.

Proceeds from those deals have helped transform the two into some of the biggest real estate owners in Germany. Grand City now owns more than 86,000 properties across the country, having grown the value of its property investments 25-fold since it was listed. Aroundtown has grown its empire eightfold since its 2015 listing. Together, they currently own about €17bn of property – and have almost €2bn of cash on hand to buy more.

“We were very bullish and very outspoken about it,” said Andrew Wallis, deputy CEO of Aroundtown. “The capital markets backed our view and allowed us to raise a lot of capital. We were able to buy really strong assets in good locations with great turnaround potential. And the sentiment towards that view has shifted significantly our way.”

“Now, we’re a bit of a poster child,” he added.

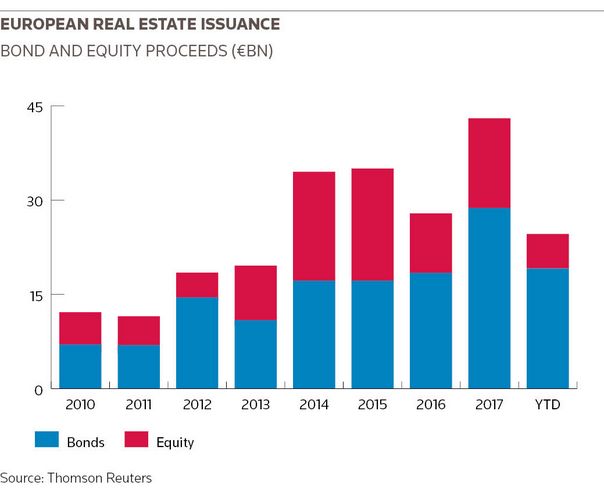

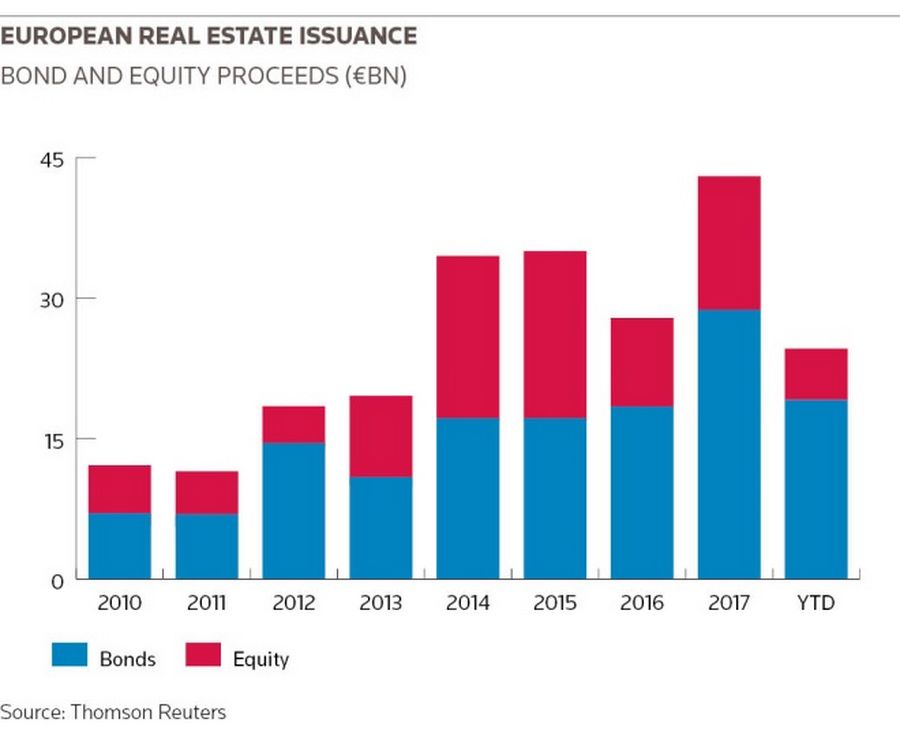

Aroundtown’s use of capital markets to fund rapid growth has inspired many others to do the same. Bond and equity issuance from European real estate companies reached a record €40bn last year, with Germany accounting for the lion’s share, and 2018 is on course to be even bigger. Companies such as Vonovia and CPI Property Group are now regular visitors to markets.

Low rates, which have driven up demand for anything with a decent coupon, have helped. So too has the European Central Bank’s corporate bond buying programme – the ECB has bought more than €9bn of real estate bonds. Such conditions have been ideal for real estate companies to diversify funding, lock in rates – and at the same time rapidly expand their portfolios.

Expansion hasn’t been solely fuelled by debt – equity accounted for about a third of all capital raised last year. That’s helped keep loan-to-value ratios down. Plus, unlike with previous bank loans, interest rates are locked in.

And the ratings agencies approve: many real estate companies have gained investment-grade ratings in recent years, helping attract yet more investors.

“The real estate industry in Europe … has grown to a point where there are an increasing number of companies of sufficient scale and quality to achieve investment grade ratings,” said David Greenbaum, chief financial officer at CPI, which has grown its portfolio tenfold in the past few years.

TESTING THE LIMITS

There are signs, however, that the sheer volumes of capital raising – particularly in bonds, where almost €20bn has been raised by real estate companies this year – may be beginning to test the limits of the market. Aroundtown had to pay a premium to get a euro bond deal over the line in April and many property companies are looking to issue in other currencies, amid concerns the euro market may be saturated.

It has also pushed up property prices to the extent that decent investments are becoming harder to find. Some companies have begun to slow the pace of acquisitions.

“Low interest rates create a great opportunity for acquisitions and further consolidation in real estate,” said Greenbaum. “However, the abundance of capital also has a downside because prices are rising quickly. In many cases, we see better value from investing in our own properties, instead of pursuing overpriced assets.”

Others are concerned about what rising interest rates might mean for the industry. While many have used the past few years to lock in low financing costs and term out their debt, real estate companies nonetheless remain exposed to rising rates – not least through the impact on property prices. Prices have doubled in some cities over the past few years and some believe a correction is well overdue.

A correction could be painful because of legal obligations in the bonds many have sold. Unusually for investment-grade companies, Aroundtown and many of its peers have had to cede ground to investors when selling bonds, agreeing to covenants that force them to stick to strict maximum loan-to-value ratios. While such covenants are common for property companies in the US, they are relatively new in Europe.

“When they were building their capital markets presence, they had to throw the kitchen sink at it to get investors comfortable,” said one banker who has done a number of deals for Aroundtown. Rising property prices – Aroundtown booked over €1bn of valuations gains on its property empire last year alone – have enabled many in the industry to take on more debt rapidly.

But if property prices plunge, that process will reverse. Some companies could find themselves nearing or in breach of covenants, which might force them into raising equity – possibly at highly dilutive levels – or disposing of their best assets. To be sure, many are a long way from their covenant levels, but bankers say that investors have begun to ask more questions about the impact of breaches of late.

“It’s not something we worry about, but it is something we are very conscious of,” said Wallis, of a possible downturn. “We’ve spent years getting our balance sheet into a very strong position because we want to be in the best position in that scenario. When others are struggling, we’ll be picking off the best assets. That’s a very flippant way of saying it, but it is basically what we’ve prepared ourselves for.”

DISTRESSED ASSETS

Another concern is that bond and equity financing has given property companies more freedom to buy distressed assets – assets banks would have traditionally been more wary about financing. Aroundtown in particular has built its business around such assets. Often, that simply means that vacancy rates are higher, or leases shorter. The company aims to add value by addressing those problems.

“You do have vacancies, you do have rents in place that are potentially very much below the market, you might have high operating costs, or where the lease term remaining is quite short; a lot of uncertainty,” said Wallis. “Those kinds of assets, the banks won’t touch it from a financing perspective, so you have to deal with those things. That’s our world, that’s our DNA – and we are just very good at it.”

Others say that the growth of the past few years merely reflects the birth of real estate as an asset class in its own right.

“Aroundtown is the poster child for the growth of real estate as an asset class in Europe,” said one banker. “A lot of the buyside is playing catch-up – until relatively recently, many didn’t have the expertise in-house, meaning that many of the early real estate deals were bought by generalist fund managers. But, as the asset class grows, many and are now bringing in the right people, building up teams of specialists.”