IFC – the private sector development arm of the World Bank – has expanded its business in response to the financial crisis, and nowhere more than in the area the IFC calls Europe, Middle East and North Africa. Using Istanbul as its second headquarters, it has responded to the crises these regions have faced. But will it maintain its relevance once the markets recover? Nick Lord reports.

In 2009 senior officials at International Finance Corporation in Washington DC decided that the organisation had to be more local. More people needed to be on the ground in the countries IFC works in, rather than trying to solve the world’s problems by sitting in long meetings in the US capital. It was decided that a second headquarters was needed and Istanbul was the chosen city. Centrally positioned, in a country where IFC is actually allowed to work (its mandate prevents it from doing deals in OECD countries), Istanbul has that mix of old and new, developed and developing, East and West, that spoke to what IFC was looking to achieve.

The timing was good. IFC already had one floor of the Kanyon office building, the most prestigious office block in Istanbul. But it would need more. As luck would have it, five floors below Morgan Stanley had decided to pull out of Turkey, part of the retrenchment of its global operation in the face of the crisis. A deal was done and IFC took over Morgan Stanley’s office.

The trouble was that Morgan Stanley had left all their furniture behind. The oversized leather chairs and expansive mahogany desks didn’t really fit IFC’s development image. So IFC decided to give most of the furniture to the local municipality which used it to furnish schools and dormitories for poor children. And now an orphanage in the grittier suburbs of Istanbul is proudly furnished with all the accoutrements of a global investment bank.

The symbolism of this story sums up what IFC is all about. It moves in where the global banks fear to tread. It brings first world financing skills to developing countries. And, at the end of the day, it all comes down to helping the poor.

Crisis Response

One of the main difficulties with such a vast geographic region is the lack of commonalities between the sub regions. The banking crises of Central and Eastern Europe require very different responses than the food crises of North Africa or the chronic lack of infrastructure in Central Asia. And yet all fall under IFC’s regional remit.

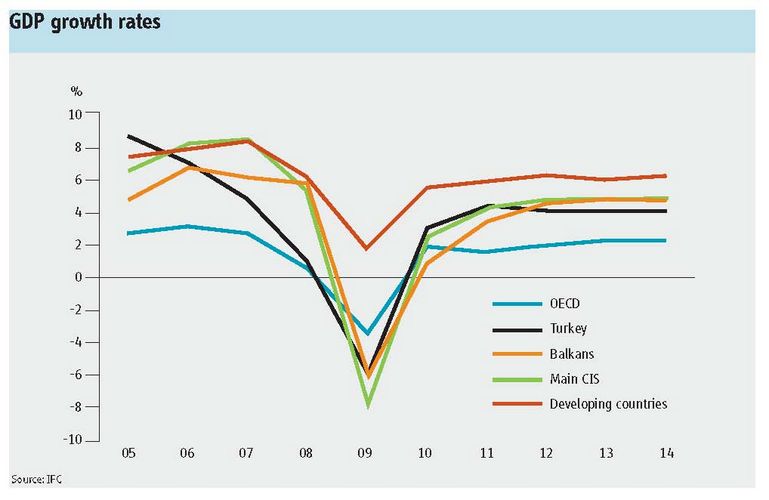

Central and Eastern Europe suffered as much if not more than Western Europe from the severity of the global financial crisis. While the western countries bemoaned 3% or 4% GDP contractions, countries in Eastern Europe like Latvia suffered a contraction of 18% in the first quarter of 2009 alone.

In response, IFC has maximised its efforts in the region. In its fiscal year from 2009-2010 it has committed a record US$3bn from its own account and mobilised an additional US$682m, supporting 105 projects. In the Middle East and North Africa, IFC has committed US$1.6bn from its own account in 58 different projects.

Many of the countries in Central and Eastern Europe were over levered and faced currency mismatches. They had effectively outsourced their banking industries to Western Banks which were threatening to pull all their money out. It was a situation that development banks were specifically created to address.

Other international financial institutions generally acknowledge that IFC has been the most proactive in responding to the secondary crises that regions such as Central and Eastern Europe have faced. Globally, IFC took the lead in re-establishing global trade finance lines through the expansion of its Global Trade Finance Programme to US$3bn and the launch of a Global Liquidity Trade Programme. It then turned its attention to cleaning up the mountain of bad debt that is clogging up the global financial system, through its Debt and Asset Recovery Programme.

While these programmes, like IFC itself, are global in approach, they have been applied very much at a local level. And nowhere have they been more applicable than in the Europe, Middle East and North Africa region.

The first deal rolled out under the DARP programme was the establishment of the €200m CEE Special Situations Fund, which was led by IFC along with EBRD and specialist restructuring group CRG Capital. This was followed in April by the establishment of the €300m ADM CEECAT Recovery Fund along with EBRD, Dutch development bank FMO and Hong Kong based distressed debt specialist ADM Capital.

Perhaps its most effective initiative has been its efforts, alongside other institutions, to keep Western banks from pulling capital out of Central and Eastern Europe, under its Joint IFI Action Plan. Conceptualised over a weekend in Athens by senior figures from IFC, the European Bank for Reconstruction and Development and the European Investment Bank, the initiative was a €24.5bn package to shore up the banking systems of Central and Eastern Europe. Part of the plan was the European Bank Coordination Initiative, or Vienna Initiative, under which Western Banks agreed not to pull their capital out of the region. Given that upwards of 40% of the region’s banking systems are controlled by Western banks, such a mass withdrawal would have had devastating consequences. That the banks have not done so, despite their existential problems at home, is testament to the efficacy of the Joint IFI Action Plan.

Another of IFC’s major global initiative is the IFC Asset Management Company. This has seen the creation of a fund management company running a number of funds, including one for private equity investments in developing market banks and one for private equity investments in Latin America and Africa. So far, AMC has raised more than US$3bn from other governments, sovereign wealth funds, corporate pension plans and central banks. They are attracted by the high levels of returns that IFC has made out of previous crises. By piggy backing on the back of deals that IFC does, they can share in the upside, while also engaging in development activities.

One of the first deals done from the AMC’s bank capitalisation fund was an investment in a Serbian Bank called Komercijalna Banka ad Beograd. The €120m investment, in conjunction with EBRD and the German and Swedish development banks, was invested in a new class of nonvoting preferred shares, convertible after three years into ordinary shares of the bank. AMC is also in the process of setting up a Russian bank capitalisation fund, again showing the local application of these global initiatives.

From defence to offence

As the crisis mellowed, so IFC has changed tack. Firstly it was a question of triage: staunching the capital flows let loose by the crisis through initiatives such as those mentioned above. But now it is moving to a secondary phase, trying to rebuild the financial sectors of many of those countries that have been hit hardest.

While looking forward, it is clear that the region is not out of the woods yet. “It does seem like the situation has stabilised and is starting to improve,” said Rashad Kaldany, vice president of Asia and EMENA at IFC in Istanbul. “The withdrawal of deposits has stopped and liquidity is starting to improve, but there is still difficulty in accessing long term funds and pricing of credit is still very high.”

Kaldany is the most senior IFC staffer in the region, having moved to Istanbul from Washington in February 2010. His presence, along with a regional management team, brings decision-making to the field. It is an indication of how seriously the organisation takes its localisation policy, and the emphasis it puts on Istanbul as its second global hub. Kaldany is now leading an office which was 50 people a year ago and will be 200 by the end of next year.

Once the worst of the crisis has past, such expansion has to be backed by on-going relevance. Development banks have a tricky time justifying their existence in middle income countries during bull markets such as 2004-2007. They cannot be active where the private sector banks operate but they still need to be at the forefront of overall systemic financial sector developments. However, their presence in frontier markets – of which there are many in the EMENA region – is relevant throughout the cycle.

In these frontier markets, IFC is maintaining its core development work such as financing microfinance institutions in Azerbaijan and infrastructure in the Middle East. But in many ways that is what the regional development banks such as EBRD or the Black Sea Development Bank do. IFC needs to do more than just dole out capital to worthy development projects.

The problem with relevance is one that Kaldany admits concerns him. In the financial markets arena, IFC is looking to focus on helping governments develop their own local capital markets. After the Asian crisis in 1997-1998, IFC undertook just this role, helping governments to extend out their yield curves and build up local capital markets. They are looking to do the same now.

In 1998 IFC helped rebuild confidence in the recently defaulted Russian economy by issuing a rouble denominated bond in its own name. It is in discussions with the Russian authorities about issuing a similar bond aimed at local institutions.

Another such deal this year closed in the UAE, where IFC issued a US$100m sukuk based on underlying leases that it owns in the region’s health and education sectors. According to Michael Essex, a (now retired) director of the Middle East and North Africa Region at IFC who did the deal, the intention was to help develop the regional Islamic finance market. Indeed it was IFC’s second such deal, coming after its 2004 Malaysian ringgit sukuk, which did kick start the remarkably vibrant Malaysian Islamic debt market.

Perhaps the country where it could have the biggest impact is its new home of Turkey. The Turkish government has a curiously cross-eyed approach to the development of its local capital markets. On the one hand it trumpets its desire to make Istanbul the next international financial centre. And then on the other it bans its banks from issuing local currency debt as it wants to have the market to itself to fund its growing budget deficit.

IFC has been in discussions with the Turkish government about issuing a Turkish lira bond in its own name, but there is no indication that it will happen. According to Edward Strawderman, IFC’s senior manager for financial markets based in Istanbul, part of the problem is on the demand side, rather than on the supply. Regulations only allow Turkish pension plans to invest a tiny proportion of their plans outside Turkish government debt. Loosening up regulations on the demand side would have as big an impact as issuing a vast supply of new paper.

“In many of our markets there is a lack of demand for local currency bonds because there is a lack of long term investors,” said Strawderman. “Stimulating this investment demand will be a key step to helping these local bond markets develop.”

Kaldany concured. “Regulators need to find the confidence to open up,” he said. “The key to developing the long term debt markets is developing long term investors.”

Advisory business

IFC’s search for relevance is therefore about more than providing capital. The advisory services side of the business employs more people than the investment side. These are the people who are travelling the region, advising businesses on corporate governance and risk management, or banks on how to expand into new products such as renewable energy. They also advise governments on how to set up credit scoring bureaus, or establish PPP structures for infrastructure development.

Kaldany highlights a project in Jordan where IFC advised the government on a new PPP law that would attract private sector finance into its infrastructure. That structure was then used for the development and finance of a new US$800m Queen Alia Airport in the country, to which IFC provided finance. That deal is now being translated into the Jordanian power sector and across the region for instance with the Pulkovo Airport deal in St Petersburg, Russia’s first major PPP deal.

“Capital is not the only constraint in the region,” said Kaldany. “The regulatory environment and policy frameworks can also be a hindrance to development so we address that through our advisory work.”

Overall, timing and geography have combined to provide a perfect storm for what IFC is trying to achieve. The crisis provided a catalyst which allowed IFC to work with other IFIs to deploy capital that was being withdrawn by the private sector. The crisis also highlighted the need for many of the countries in the region to substantially reform the structure of their financial markets.

Time will tell if IFC has been successful in meeting its goals. But in the meantime, the organisation will remain one of the dominant forces in the region’s financial markets. Just ask the Turkish orphans: they might be sitting in Morgan Stanley chairs, but those chairs came from IFC.