Turkey’s government mixes a philosophical belief in the need for private ownership with a practical imperative of raising money. The resulting privatisation spree has already created quite a buzz, and will continue to drive most of the activity in Turkey’s capital markets for many years to come. Nick Lord reports.

Turkey’s privatisation agenda is one of the boldest of any country in the world. The government has a deep seated belief in the need to remove the state from the ownership and running of most sectors of the economy. It also needs the money to finance its on-going budget deficit. As a result, the government has honed a process that works effectively in transferring operating rights, as well as outright sales of assets.

However, the high profile deals of the past, such as the privatisation of Turk Telecom into a bull market, will be hard to repeat in the future. The global recession is limiting the appetite of strategic buyers and stemming the flow of international finance, needed to pay for the huge numbers of assets on the block. That means that if the government really wants to sell these assets, it will have to develop the local capital markets. Only this will allow local buyers and their financiers to raise the sums required.

Everything but the kitchen sink

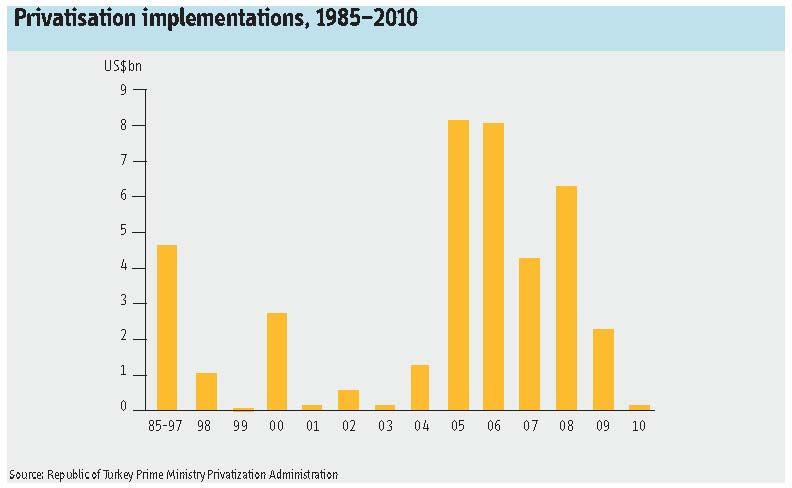

Looking at what is for sale, the scope of the government’s ambitions becomes clear. Everything is seemingly for sale. On its website the Privatisation Authority (PA) lists whole industries such as electricity generation and distribution as well as gas distribution that are being entirely sold off. All the country’s motorways and toll bridges are also being sold, as are its ports and ferry services. All told, bankers estimate that assets worth in excess of US$20bn are for sale in a process that will take some four to five years.

“We expect the vast majority of capital market deals to come out of Turkey in the next few years will be in the energy and financial services sectors.” says Murat Demirel, head of Citi’s banking business in Turkey. “In the energy sector, for instance, the volume of deals in the pipeline cannot be funded entirely by the bank market. The privatizations, upgrades and new builds in the sector will be the main driver of the debt and equity capital markets in coming years.”

The deals that the government has mentioned recently include secondary public offerings of already part-privatised companies such as Turkish Airlines or Turk Telecom. The government needs to be very careful about what it says about these deals as both are already listed, but bankers in Istanbul all say activity underway.

Likewise government owned Halk Bank is receiving attention. It is already 25% listed and the government has appointed Goldman Sachs to examine whether to try and sell the remaining 75%, either publicly or to a strategic buyer. Given that most strategic buyers would be foreign banks or private equity firms, it is likely that the government would need to go the public offering route.

Highly charged

Most privatisation activity has so far come from the electricity sector, with 20 regional distribution companies already in the process of being sold and the sale of Turkey’s generation assets in the consultation stage. In the distribution sector, eight regional companies that are part of the Tedas group have already been sold. The two biggest of these were the Bedas (Bashkent Electricity Distribution) and Sedas (Sakarya Electricity Distribution) deals.

In mid February, four more distribution companies - Uludag network, the Camlibel grid near Sivas, the Firat grid in the Eastern province of Malatya and the grid around the Eastern City of Van - were sold. From 42 pre-qualified, three Turkish companies emerged victorious: Limak Group bought the Uludag Grid for US$940m; Kolin Insaat bought the Camlibel grid for US$285m; and Aksa Elektrik Perakende Satis paid US$330m for Firat and Van.

On the generation side, the privatisation authority originally put all the country’s thermal and hydro power assets into a company called EU AS. This portfolio was then divided into six smaller portfolios but none of these received much market interest. It was then decided to put them all back into portfolio containing 45 generation assets and begin a new sale process through Citi and local firm Oyak Securities. Market sources suggest that this new company is ideal for an IPO as it is a sector that is easy to understand, where revenues are stable and the companies can afford to pay dividends. But it would be a massive undertaking.

The other shining beacon of the privatisation process is Igdas, the gas distribution company serving Istanbul. This deal is being undertaken by Citi, EFG and AK Securities. The company is also a candidate for an IPO followed by a block sale to a trade buyer. With a price tag of over US$4bn this would be a large deal at any time. But during these capital constrained times it is doubly so. Thus a multi stage process which involves a strategic investor plus domestic and international offerings would make the most sense. But such a complex undertaking would take time and as such no one is really expecting this to come to market until at least early 2011.

The government has just started the process for selling its transport assets, in particular the toll roads, and bridges. Bankers say the assets are worth between US$3bn and $4bn at current comparable valuations. The sale is being handled by local firm TSKB. Also for sale is IDO, the iconic ferry company that criss-crosses the Golden Horn, the Bosporus and the Sea of Marmara. Advisers for this deal are expected soon.

Also in the transport sector, ports that are for sale include the re-tendering of Izmir Port which was originally sold in 2007 for US$1.25nbn but then failed to complete when the bidders could not raise the finance due to the financial crisis. The privatisation authority is now the owner again and is likely to sell it in 2011.

One other deal that failed due to the crisis was the sale of a ten year concession to run the national lottery. The PA put a floor price of US$1.6bn on the deal but the concession terms were harsh, with limits on advertising and prize draws that would have been hard to sell in a bull market. These terms are understood to be revised and the deal could come soon. While not an IPO candidate per se, it is definitely a candidate for some local currency debt and any deal is likely to be financed in this market.

What all these deals point to is a huge supply of product coming onto the market that needs to be financed locally. This will create a virtuous circle where both the supply of good investments is matched by a liberalisation of the local capital markets, resulting in rapidly improving markets, companies and returns.

However in order to get there, the government will need to be mindful of market conditions. There is a feeling among some that it is trying to do too much, especially at a time of global market tension and heighted political worries within Turkey. The PA recognises this and is providing financing for the deals that go through, by allowing the winning bidders to pay in instalments. These are typically structured over a three year period where 25% is paid in the first year, 50% in the second and 25% in the third. Finance is provided at Libor +4% to offset the lack of foreign banks providing more than a one-year bridge. This should allow the deals to get done even if the local markets are not ready to provide the long term debt and equity finance they deserve.

| 2009 implementations | ||

| Contract date | Sales (US$) | |

| Block sale | ||

| Total block sale | 0 | |

| Asset sale | ||

| Baskent Electricity Distribution Com | 28/01/2009 | 1,225,000,000 |

| Sakarya Electricity Distribution Com | 11/02/2009 | 600,000,000 |

| Meram Electricity Distribution Com | 30/10/2009 | 440,000,000 |

| Tekel Real Estate | 2009 | 3,640,097 |

| Tedas Real Estate | 2009 | 3,678,567 |

| T Seker | 2009 | 1,314,125 |

| Sümer Holding real estate | 2009 | 138,188 |

| DMO | 2009 | 1,214,182 |

| Total asset sale | 2,274,985,159 | |

| Public offering | ||

| Total public offering | 0 | |

| General total | 2,274,985,159 | |

| Source: Republic of Turkey Prime Ministry Privatization Administration | ||

| Privitisation implementations at signature stage | ||

|---|---|---|

| Approval date | Sales (US$) | |

| TCDD Izmir Port | 03/07/2007 | 1,275,000,000 |

| TCDD Derince Port | 22/11/2007 | 195,250,000 |

| TCDD Bandirma Port | 19/09/2008 | 75,500,000 |

| TEKEL Real Estate | 30/01/2009 | 689,172 |

| TEKEL Izmir Real Estate | 30/04/2009 | 8,704,119 |

| TEKEL Istanbul Real Estate | 14/07/2009 | 198,350,893 |

| TEKEL 5 Real Estate | 25/12/2009 | 559,390 |

| TEKEL Ankara Real Estate | 05/02/2010 | 20,416,497 |

| TEKEL Izmir Real Estate | 05/02/2010 | 25,044,236 |

| TEKEL Izmir Konak Real Estate | 05/02/2010 | 5,097,319 |

| TEKEL Real Estate | 22/02/2010 | 985,238 |

| TEKEL Camalti Salt Mine | 24/03/2010 | 76,605,382 |

| TEKEL Ayvalik Salt Mine | 24/03/2010 | 5,995,204 |

| TEKEL Real Estate | 24/03/2010 | 5,921,395 |

| TEKEL Real Estate | 30/03/2010 | 8,678,787 |

| Total | 2,002,797,632 | |

| Source: Republic of Turkey Prime Ministry Privatization Administration | ||