South Africa has been the sleeping giant of emerging markets for many years. While emerging European ECM issuance was rampant from 2005 on, South Africa was a rare source of interest. Yet volumes are climbing while Russia slumbers and 2007 totals are now in sight. Owen Wild reports.

The sound of vuvuzelas has passed in South Africa following the world cup, but the country is now buzzing to a different sound: visiting equity capital market bankers rushing around to pitch to potential issuers. Bankers are keen to ensure they are involved in the resurgence in emerging market activity.

For years South Africa has been viewed as a market that under delivers, with a flow of issuance well below its potential. The focus has been on emerging Europe, Russia and the Middle East for emerging market ECM bankers in the past five years. When attention has turned to Africa, it is Kenya and Nigeria that have aroused the most interest. When the Johannesburg Stock Exchange witnessed its largest ever IPO this year, for Life Healthcare at R4.78bn (US$627m), it still fell short of the KSh50bn (US$765.9m) float for mobile operator Safaricom in Kenya in June 2008.

Yet banks are positive on the prospects in the country.

“Government policy and black empowerment has facilitated the emergence of a broader middle class and a redistribution of wealth,” said George Pavey, co-head of emerging markets ECM at Credit Suisse. “Robust population growth and an emerging middle class, coupled with a rebound in demand for commodities, are fuelling economic growth and helping the performance of South Africa’s equity market.”

During the heyday in 2004–2007, South Africa was overshadowed by faster growing emerging markets such as Russia, CEE and Kazakhstan, Pavey said. But the financial crisis focused investors away from growth to risk. “South Africa has emerged from the financial crisis as a winner, attracting a disproportionate share of inflows into emerging markets courtesy of the quality of many companies in SA, the strong corporate governance, transparency, relatively conservative balance sheet structures. South Africa is a lower beta market, but it is a good place to put money,” Pavey added.

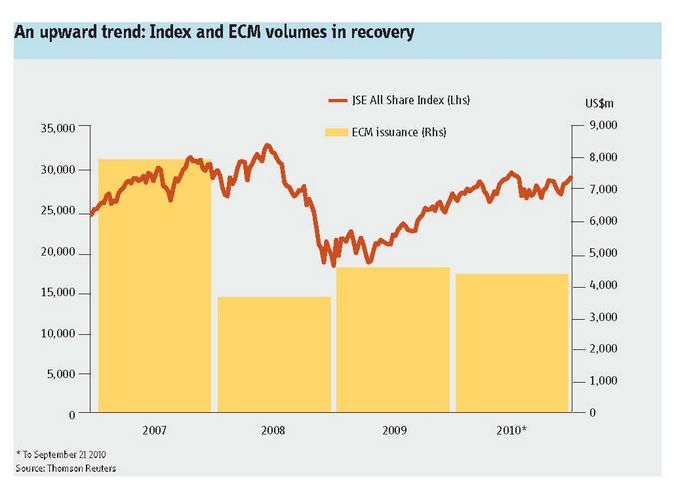

The positive mood is reflected in the build out of investment banking operations. While Credit Suisse had no bankers in the country three years ago, it is now in the process of building a team of around 60 bankers to cover Southern Africa. In 2007 South African ECM volume was strong with nearly US$8bn raised through 24 deals. As a relative measure in the same year, UK volume was about US$50bn. However the importance of South Africa dropped in 2008: the number of deals was flat but volume dropped to US$3.7bn, putting the country sixth against the rest of Africa and the Middle East. Significantly, the number of deals rose to 36 in 2009, thanks to a stream of rights issues, and the year to-date total in 2010 is already flat to the full-year of 2009.

Stay local

One reason that South Africa has previously provoked less interest than some emerging European countries is the lack of companies heading to South Africa from other countries. Poland has become the most important country in emerging Europe thanks to a flow of privatisations, but also its ability to attract companies from other countries, such as the Czech Republic, to list in Warsaw.

The Johannesburg stock exchange could have taken advantage of its more developed systems to become a hub market for sub-Saharan Africa. But building a stock exchange is seen as a crucial part of developing the frontier markets, and the JSE has acknowledged this by avoiding competing for listings.

The JSE did set up the Africa Board to attract cross listings from across Africa, with the lure of its trading and settlement systems and wider investor base. But the initiative has not been successful. Trustco Group Holdings of Namibia was the first company to list on the Africa Board in February 2009. Botswana safari firm Wilderness Holdings followed in April 2010. The two remain the only constituents of the Africa Board.

An IPO market has always struggled establish itself in South Africa. South African companies tend to be reserved when it comes to financing, and have always been well served by local banks. Many markets where local banks provided financing to small and medium enterprises were hit by the financial crisis, but because of strict foreign exchange controls banks did not blow up and Tier 1 ratios are high. Liquidity has fallen a little however as some international bankers needed to retrench.

There are currently prospects that appeal to investors but it is not always an attractive prospect for the issuers, said bankers. “If a company is growing at 20%–25% per annum, as some are, then why IPO today if the market is not going to pay you for that growth?” said one EM banker.

One co-head of CEEMEA ECM said: “Companies have mandated for IPOs that could come to market this year, but some are likely to push back into next year. Before any company is willing to push the button on a deal they need to see something else in the region complete on a fully-marketed basis.”

Life lesson

The IPO of Life Healthcare was a clear illustration that investors were not going to rush to new issues, however rare the opportunity.

As a new benchmark in South African IPOs the deal could be expected to attract attention from local investors. The scale of the deal meant it would be hard to ignore, considering the inevitable weighting in local indices. Yet it was domestic accounts that were most difficult to attract to the deal.

Initial pricing offered a discount to Mediclinic through the range and a discount to the less favoured peer (by the lead banks) of Netcare in the bottom half of guidance. These multiples were based on EV/Ebitda multiples that international accounts were happy to use. Domestic accounts insisted on using P/E multiples irrespective of sector, where the discount turned into a premium to peers.

Another issue for the deal to contend with was that the driver was a sell down by several large shareholders. Bookrunner Rand Merchant Bank was the largest seller in the all-secondary deal.

The result was that, on the last day of bookbuilding, pricing was revised from R14.50–R17 to R13.50–R14.50, while the number of shares to be sold was reduced by nearly 18%. The deal successfully completed at the bottom of revised guidance to raise R4.78bn, ahead of the 2003 IPO of Telkom that raised R3.86bn. The move had a dramatic impact: the final book saw 75% of demand come from domestic investors and the top 10 accounts took two-thirds of the deal. Credit Suisse, Morgan Stanley and Rand Merchant Bank were joint bookrunners.

On Optimum Coal, the other sizeable IPO in South Africa this year, locals were fundamental to getting the deal away from early on. This was reflected in a long three-week pre-marketing period that was designed to give local accounts more time to consider the issue. The final book reflected the approach, as just a handful of international accounts were involved. In part this was because international accounts had to take a view on exchange rates. Again the price guidance was cut, with the R34–R37 range abandoned in favour of a R32 fixed price, to raise R1.37bn. JP Morgan, Morgan Stanley and Rand Merchant Bank were bookrunners.

Until mid-September both issues were below issue price, but Life Healthcare then jumped from R13.16 to R14.45 in the space of two weeks. On September 21 Optimum was trading at R26.10, down 18.4%.

Life Healthcare priced in June and Optimum Coal in April, both when IPOs were cancelled in other countries.

“Both IPOs that have launched this year have managed to price, which you have to view as positive,” said Richard Stout, head of ECM at Barclays Capital’s South African business, Absa Capital. “You can dwell on the fact that both deals priced below their ranges, but you have to remember that they were up against a challenging backdrop globally and at a time when IPOs were being cancelled in other markets across the region.”

Converting into deals

Mid-September not only saw a recovery in stock prices, but a brace of convertible bonds from South Africa. AngloGold Ashanti raised US$1.58bn through straight equity and mandatory convertible bonds, while within 24 hours furniture company Steinhoff had raised €345m through its third convertible issue.

The AngloGold deal was sold into the US, while the Steinhoff bonds largely went to European accounts, illustrating the strength of international demand for the right South African paper. Local accounts were not in either deal.

North American demand for AngloGold’s deal was so strong that the bookbuild was closed much earlier than planned. Launching after the US-listed ADRs closed, the intention was to run for up to 24 hours, with the hope to close earlier. In the end the deal closed before European sales teams could even get involved.

While European accounts were disappointed to be excluded the opportunity to close early and remove any risk around the deal was leapt on. Accounts that missed out were quickly pacified by the positive message shown to AngloGold by the rapid completion.