IFR: The first thing I wanted to pick up on was the fact that there seems to be very good demand for Gilts, even with 10-year yields below 3%. How does the panel see ongoing demand? Are there technical issues behind the inflows? Do you feel the level of interest in Gilts and sterling assets will change within the next three to six months? Sam, can you get us going with a strategic perspective?

Sam Hill, RBC Capital Markets: Well it’s definitely true that in the context of another large year of supply, digestion of that supply has been comparatively easy. We’ve funded over £90bn so far this fiscal year, and yields have fallen 100bp since the peak in the 10-year sector. I think this reflects a number of concerns about sentiment, prospects for growth and the potential for deflation outside of the UK. But I think if we look within the UK, and the domestic factors influencing Gilt yields, we are facing a period in the next few months where inflation is going to continue to be above target, and growth is going to be low but still positive, in which case 10-year Gilt yields at just below 3% look fairly unattractive.

We’re also in the run-up to the government’s public sector spending review, and given the potential for opposition to the spending cuts that are coming along, it may well be that the strong total returns that investors have realised in 2010 so far are vulnerable if there is a perception that the opposition to spending cuts requires a bit more risk premium in yields to compensate for the chance that the government might not be able to force through those spending cuts as easily as they expect to.

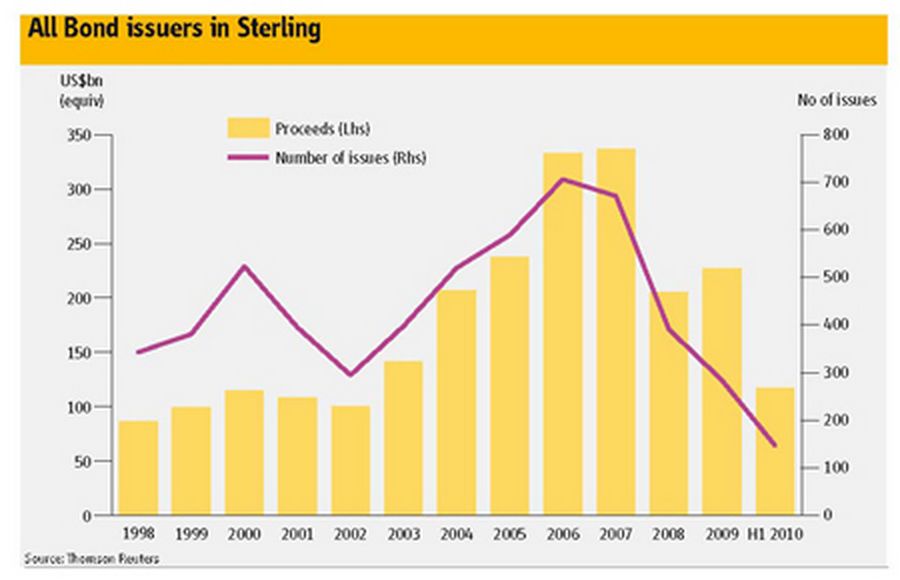

All Bond issuers in Sterling

IFR: So inflows into Gilts may be short lived, depending on what happens?

Sam Hill: Six-month rolling returns in the Gilt market are up over 8%, and that’s a very rare position to be in. And given that unfavourable imbalance between ex-post returns and ex-ante returns as implied by current yields, it does look as though we’re probably due a correction in the short term, heading into year-end.

IFR: Do you buy that, Steve?

Steven Major, HSBC: It’s not unreasonable to think about a correction. And I can imagine that we might get better buying opportunities than at present, but that’s really more of a tactical issue so maybe some of the more cyclical data might support that. I buy the idea that we do have some implementation risk for the austerity measures.

But on a longer-term basis, and thinking into 2011, I think it’s important to appreciate how we’ve actually got where we are. And there is this secular deleverage that we can be half-way through. And at half-way, we could move three to four years into a seven to eight-year secular deleverage, whereby people are increasing their savings and paying down debt around the world, and the UK especially. And that I think is consistent with recalibrating expectations for return. One year ago, people could rightly look for a 4% to 6% return with quite low risk. Now, it’s more likely to be 2% to 4%. So where do you go to get 2% to 4%? You need investment-grade credit as well as some longer-dated Gilts.

So I see a picture whereby money is being squeezed up the curve and I think that yields could be heading towards 2% in 2011, although I do accept the possibility that there are better buying opportunities in 2010.

Frazer Ross, Deutsche Bank: From a technical perspective, that’s quite interesting, because what we’re seeing is a huge amount of overseas bite. Year-on-year, we’ve seen huge growth in overseas holdings. We find that the overseas central banks are indifferent to yield. They have currency views that they are looking to implement. They frankly want to diversify away from euros and the US dollar, especially at the shorter end of the curve where yields are 0.25%, 0.5%, 1%; it doesn’t matter. We’re seeing huge buying from these central banks, and that’s really had a big impact on the short end of the curve.

IFR: Are those foreign inflows technical or strategic?

Frazer Ross: I think they’re strategic to be honest, because in all our discussions, we continue to have central banks that want to diversify away. If you look at what most central banks should be holding in sterling, it’s 3%, 4%, 5% if they were matching to benchmark, let’s say, in terms of the value of sterling. A lot of them hold around 10%. Why is that? Because they’ve got too much dollar, too much euro, so they’re almost overweight sterling because they are trying to reduce their overweight on euro and dollar.

And if you look at what Bill Gross said a couple months ago – [“the UK is a must to avoid. Its Gilts are resting on a bed of nitroglycerine”] – that was clearly, incorrect and I think that’s cost him some money. But the fact is this overseas buying, which according to the DMO is 30% of the market right now, is technically underpinning the market.

IFR: Georg, what do you make of the current attraction by international buyers of sterling?

Georg Grodzki, Legal & General: We’re slightly bemused by the extent of foreign interest in Gilts and sterling assets. I refer to what my co-panellists remarked on earlier about the implementation risks for fiscal consolidation, and the political stability issues which may ensue from that. I think sterling at the moment is probably a bit of a beneficiary of the even bigger headline plight of other regions, mainly in Europe, and whether this is deserved or not is of secondary importance. But right now, it’s helping the Gilt market.

It doesn’t help the economy because strong sterling is probably not in the interest of exporters and not really in the interests of the Bank of England either. As far as the risk of a correction is concerned, of course, in the back of our minds, we wonder what degree of correction the Bank of England would find tolerable. Not that I want to make it sound like we assume the Bank of England will roll out QE2 willy-nilly, but there is a bit of a sense on our side that within reason, a correction would be accepted, But at the same time, the Bank of England is keeping an eye on the commercial property market, the banks, and on the funding costs of the still sizeable government deficit.

Therefore if it was to come to a correction, we shouldn’t assume it would go unmonitored. There is probably a contingency plan in place by monetary authorities to keep it within a reasonable range. So that limits the downside somewhat. What we can’t rule out – but this is a longer term issue – is whether this big bond bubble globally will unravel at some stage. Even die-hard bond enthusiasts feel enough is enough and maybe the tipping point towards the return of inflation has come too close. And if there was a global bond sell-off, I think it would be difficult to contain no matter how much money central banks were to throw at the market. That is the Black Swan risk of our time. It may never materialise, but it’s scary to think of it.

IFR: Myles, there are risk factors everywhere. How do you see them balancing out? And how do you see the Bank of England’s room for manoeuvre?

Myles Clarke, RBS: Gilts have been a defensive play in a very difficult market. And also, there’s been a lack of alternative supply. We haven’t seen enough of the other type of issuance we would have seen throughout most of 2009. So it’s a very cash-rich investor base and defensively, they’re going to buy Gilts.

And I’d also say that bank treasuries are under pressure to reduce some of the more risky assets, and buy more Gilts.

IFR: How does all of this play out for you, Thomas? The EIB conducts a sizeable proportion of its funding in sterling. I suspect it will be a bit lower this year than perhaps previous years, because non-UK borrowers have been faced with an unfavourable basis swap all year. Bearing mind in mind what’s been said so far, how do you envisage your sterling funding evolving for the rest of this year and into 2011?

Thomas Schroder, EIB: This year we have a funding programme of €70bn, of which we’ve done about 80% so far. We’ve done almost £4bn in sterling, which corresponds to only 8% of our funding so far. When I say only, it’s because it’s less than the 10% of previous years. The reason for this is basically tight swap spreads, as you say, so it’s difficult for us to issue.

We’ve seen most demand in the short-term area, three, four, five years. And what is quite important this year is we have seen good demand for our floating-rate notes: 70% of our sterling funding has been floating-rate and that’s the first time that we’ve done more floaters than fixed-rate. We’ve seen good demand from banks and building societies for this product. Total volume is below other years and we’ve not done anything beyond 10 years. On the subject of the basis swap, while we are a non-UK issuer, we do have operations in the UK and we lend to UK borrowers. As such, even though we swap quite a bit into euros, we don’t have to swap everything. We haven’t done that much sterling this year but we have a relatively good balance between what we need and what we fund in sterling. So we did not have to go to the swaps market that often.

IFR: So what’s your outlook then for your sterling issuance going forward?

Thomas Schroder: We will probably be able to issue some more of the successful product which has worked so far this year, including the four and five-year floaters. We also did a £300m SONIA-floater earlier this year, which was a novelty. This is the kind of product I see for the rest of the year.

IFR: Moving to you, Samantha, as a UK-based borrower, you’re quite happy to be in sterling, but how do you look at your funding?

Samantha Pitt, Network Rail: As a UK-based company, we have a natural need for sterling. It’s our home market. Ever since we got our UK government guarantee in late 2004, the majority of our funding has been in sterling, be that nominal or inflation linked. But we do look at other markets. We look at what offers us the most attractive cost of funding on an equivalent sterling basis, and that has not always necessarily sterling. It can be other currencies like US dollar, which still remains very attractive to us. But obviously, if we do issue fixed-rate sterling, we don’t have to worry about undertaking any derivatives, and there are no associated hedging costs.

IFR: Are your funding targets fixed?

Samantha Pitt: It varies. We only borrow to fund capital investment on the railways. We don’t borrow to fund day-to-day costs of running the railways. We have been pretty predictable. We issue about £4bn per annum. It was slightly more in 2008 because we had some significant redemptions. At this point in time, it’s still predicted to be £4bn per annum for the next five years.

IFR: A lot of that issuance has been in the form of inflation linked bonds, hasn’t it?

Samantha Pitt: It has, yes. Since early 2007, we made the strategic decision to increase the proportion of inflation-linked debt in our portfolio. What you saw through 2007, 2008 and 2009 was most of our issuance in long-dated sterling inflation-linked debt, and the balance in US dollars. We now have 50% of inflation-linked debt on our books and we want to stick with that 50-50 mix. What that does mean is any new debt we raise to fund capex will be split between nominal and linker, but as all of the redemptions we’ve got coming up are nominal, they’ve got to be replaced with nominal to maintain that 50-50 ratio. So we will be issuing less sterling inflation-linked paper going forward.

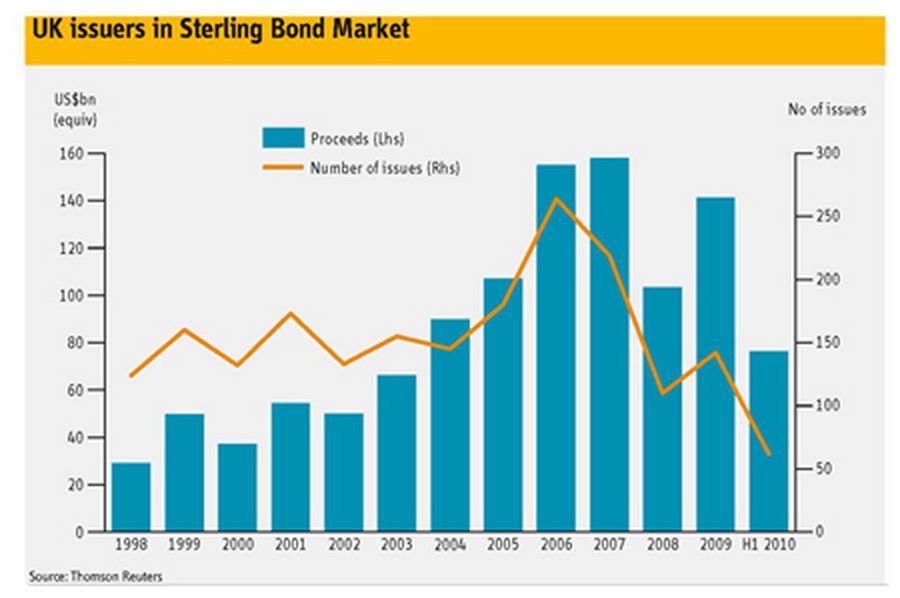

UK issuers in Sterling Bond Market

IFR: There’s a technical point at play on the inflation linked front, linked to the potential shift of final salary pension uplifts from RPI to CPI, which had quite a negative impact on the index-linked market. Is this an issue for you, given you’re the largest non-government issuer?

Samantha Pitt: The DMO has said it will enter consultation before it looks to switch to CPI. From our perspective, our revenues are linked to RPI and our regulatory asset base is linked to RPI. So we would prefer to issue RPI-linked debt. Given the volumes that we have to raise, it will have a significant impact. It’s going to open up an RPI/CPI-linked swap market.

Sam Hill: There are a number of complex issues which the July announcement has thrown up. The first one of which is clarification on the scope of the application of the policy. Before the end of this calendar year, we expect to see the introduction of legislation into the House of Commons, which will give us more information as to how different defined benefit schemes with different wordings will be affected by the proposed change.

My understanding and my hunch, if you like, at this stage is that the government has a preference for making this change as all-encompassing as they practically can. And I think that if that does turn out to be the case, then that will put sufficient pressure on the Debt Management Office to have a formal consultation, and there will be an extended period of time where we have to think about changes to the structure of the index-linked Gilt market.

But I think the most likely outcome actually is that we end up with a scenario where we have some index-linked Gilts continuing to have cashflows linked to the retail price index, and some of the new ones linked to the consumer price index rather than an outcome which invokes indexation clauses on the existing stock of debt, and forces conversion to CPI. That would mean that investors would be locked into a stream of cashflows, which if history were to repeat itself, would over time deliver a lower series of nominal cashflows under CPI than under RPI, which I think is unlikely to happen.

But a lot of this is still very uncertain at this stage. The introduction of legislation, probably out of the party conference season, will bring back to the front pages the whole issue about indexation of pension schemes.

Myles Clarke: It’s interesting, though, because the government announced the proposed shift in the middle of the DMO having mandated a new transaction, which RBS was lead managing. The disarray at the time did cause a lot of issues and volatility. But subsequently the DMO ended up doing the largest transaction they’ve ever done in the inflation-linked market. Part of that was because it did push the market a little bit lower, given the confusion around it.

But the reality is that there is structural demand for those linkers. Until there is an alternative product, it is still your best hedge to buy RPI. There’s a basis market as well between CPI and RPI where further hedging can be done. The July announcement certainly did cause some confusion, but until something else is declared, it doesn’t stop successful auctions or successful syndications of linkers. And even if you bifurcate it into CPI and RPI, there still seems to be enough cash on the sidelines to satisfy all of that supply.

Steven Major: It must be structural demand for the linker market to carry on being so strong through all of this, through all of the shenanigans surrounding it and the obvious lack of communication between the government and the DMO – I can’t imagine the DMO was delighted about having to do an auction on the same day. But the confusion surrounded by the various bases being created – you’ve potentially got three-month versus eight-month, you’ve got CPI versus RPI, you’ve got the swap market versus the cash market and then potentially, there’s the simple fact that some of the defined benefit schemes actually find a better hedge from the nominal market. So if they’re planning a transition over to CPI, it’s already been shown, I think, that convention Gilts were a better hedge.

All of this is going on at a time when the break-even sits way below the spot CPI/RPI level anyway. So from an economic standpoint, one wonders why anyone would buy a linker. But in fact, the inflation-linked market has nothing to do with inflation, funnily enough. It’s much more about longer-term liability matching.

Sam Hill: But I definitely agree with Steven that the fact that CPI is generally lower and generally less volatile than RPI means that nominal Gilts are a less bad hedge against CPI-linked liabilities than they would have been against RPI liabilities, which would support a compression of long break-evens.

Click here for Part Two of the Roundtable.

| All bond issuers in Sterling H1 2010 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | Barclays Capital | 10,550.10 | 13.1 | 31 |

| 2 | HSBC | 9,131.50 | 11.3 | 29 |

| 3 | RBS | 7,990.10 | 9.9 | 39 |

| 4 | RBC Capital Markets | 7,820.30 | 9.7 | 19 |

| 5 | Deutsche Bank | 6,445.80 | 8 | 22 |

| 6 | Nomura | 5,652.50 | 7 | 6 |

| 7 | JP Morgan | 5,410.10 | 6.7 | 14 |

| 8 | Lloyds Banking Group | 3,884.90 | 4.8 | 14 |

| 9 | UBS | 3,471.60 | 4.3 | 7 |

| 10 | Morgan Stanley | 3,258.90 | 4 | 3 |

| Industry total | 80,791.40 | 100 | 100 | |

| Source: Thomson Reuters | ||||

| All bond issuers in Sterling 2009 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | Barclays Capital | 41,143.20 | 19.8 | 100 |

| 2 | RBS | 37,356.10 | 18 | 99 |

| 3 | HSBC | 24,707.20 | 11.9 | 76 |

| 4 | RBC Capital Markets | 13,900.10 | 6.7 | 39 |

| 5 | JP Morgan | 13,026.90 | 6.3 | 39 |

| 6 | Deutsche Bank | 11,831.30 | 5.7 | 41 |

| 7 | Goldman Sachs | 11,471.80 | 5.5 | 12 |

| 8 | Lloyds Banking Group | 7,473.90 | 3.6 | 24 |

| 9 | BNP Paribas | 7,450.70 | 3.6 | 35 |

| 10 | UBS | 7,134.90 | 3.4 | 23 |

| Industry total | 207,919.20 | 100 | 256 | |

| Source: Thomson Reuters | ||||

| All bond issuers in Sterling 2008 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | HSBC | 28,899.20 | 17.2 | 91 |

| 2 | RBS | 27,637.60 | 16.5 | 85 |

| 3 | Barclays Capital | 26,322.50 | 15.7 | 70 |

| 4 | BofA Merrill Lynch | 11,173.10 | 6.7 | 21 |

| 5 | UBS | 10,981.00 | 6.5 | 27 |

| 6 | RBC Capital Markets | 10,952.20 | 6.5 | 46 |

| 7 | Deutsche Bank | 8,996.80 | 5.4 | 36 |

| 8 | BNP Paribas | 7,485.40 | 4.5 | 31 |

| 9 | Morgan Stanley | 6,042.90 | 3.6 | 27 |

| 10 | Citigroup | 5,998.10 | 3.6 | 12 |

| Industry total | 167,915.50 | 100 | 351 | |

| Source: Thomson Reuters | ||||

| All bond issuers in Sterling 2007 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | RBS | 49,618.30 | 16 | 167 |

| 2 | Barclays Capital | 47,996.20 | 15.5 | 137 |

| 3 | HSBC | 30,762.40 | 9.9 | 103 |

| 4 | Deutsche Bank | 29,927.90 | 9.7 | 79 |

| 5 | Alliance & Leicester | 21,050.20 | 6.8 | 1 |

| 6 | BofA Merrill Lynch | 15,341.10 | 5 | 33 |

| 7 | Morgan Stanley | 15,198.10 | 4.9 | 37 |

| 8 | UBS | 14,730.60 | 4.8 | 48 |

| 9 | JP Morgan | 14,699.20 | 4.7 | 43 |

| 10 | Citigroup | 12,709.80 | 4.1 | 24 |

| Industry total | 310,230.90 | 100 | 609 | |

| Source: Thomson Reuters | ||||

| UK issuers in Sterling Bonds H1 2010 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | Barclays Capital | 8,038.00 | 14.6 | 17 |

| 2 | RBC Capital Markets | 4,747.50 | 8.6 | 5 |

| 3 | Nomura | 4,398.00 | 8 | 2 |

| 4 | HSBC | 4,319.30 | 7.9 | 8 |

| 5 | JP Morgan | 3,842.70 | 7 | 9 |

| 6 | RBS | 3,754.80 | 6.8 | 18 |

| 7 | Lloyds Banking Group | 3,735.60 | 6.8 | 13 |

| 8 | Deutsche Bank | 3,520.40 | 6.4 | 8 |

| 9 | Morgan Stanley | 3,014.80 | 5.5 | 1 |

| 10 | UBS | 2,897.90 | 5.3 | 4 |

| Industry total | 55,049.90 | 100 | 40 | |

| Source: Thomson Reuters | ||||

| UK issuers in Sterling Bonds 2009 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | RBS | 25,562.90 | 20.7 | 57 |

| 2 | Barclays Capital | 25,141.30 | 20.3 | 45 |

| 3 | HSBC | 16,294.30 | 13.2 | 38 |

| 4 | Goldman Sachs | 10,438.30 | 8.4 | 8 |

| 5 | JP Morgan | 8,028.60 | 6.5 | 17 |

| 6 | RBC Capital Markets | 5,607.70 | 4.5 | 10 |

| 7 | Lloyds Banking Group | 5,222.40 | 4.2 | 18 |

| 8 | Deutsche Bank | 4,658.40 | 3.8 | 12 |

| 9 | UBS | 3,894.20 | 3.2 | 11 |

| 10 | Citigroup | 3,815.30 | 3.1 | 8 |

| Industry total | 123,649.80 | 100 | 121 | |

| Source: Thomson Reuters | ||||

| UK issuers in Sterling Bonds 2008 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | RBS | 14,801.90 | 20.3 | 28 |

| 2 | HSBC | 14,080.90 | 19.4 | 27 |

| 3 | Barclays Capital | 11,355.30 | 15.6 | 22 |

| 4 | UBS | 7,345.90 | 10.1 | 10 |

| 5 | BofA Merrill Lynch | 5,390.50 | 7.4 | 6 |

| 6 | Lloyds Banking Group | 3,745.20 | 5.2 | 8 |

| 7 | RBC Capital Markets | 3,672.00 | 5.1 | 12 |

| 8 | BNP Paribas | 2,542.90 | 3.5 | 11 |

| 9 | Citigroup | 1,913.00 | 2.6 | 5 |

| 10 | Credit Suisse | 1,397.40 | 1.9 | 2 |

| Industry total | 72,756.40 | 100 | 86 | |

| Source: Thomson Reuters | ||||

| UK issuers in Sterling Bonds 2007 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | Barclays Capital | 21,567.30 | 15.1 | 38 |

| 2 | Alliance & Leicester | 21,050.20 | 14.7 | 1 |

| 3 | RBS | 19,516.10 | 13.7 | 55 |

| 4 | Deutsche Bank | 12,478.10 | 8.7 | 25 |

| 5 | HSBC | 10,867.50 | 7.6 | 28 |

| 6 | Morgan Stanley | 8,857.40 | 6.2 | 15 |

| 7 | Lehman Bros Intl (Europe) | 8,688.90 | 6.1 | 16 |

| 8 | BofA Merrill Lynch | 6,578.00 | 4.6 | 16 |

| 9 | Citigroup | 6,050.70 | 4.2 | 12 |

| 10 | Credit Suisse | 5,699.60 | 4 | 6 |

| Industry total | 142,860.10 | 100 | 195 | |

| Source: Thomson Reuters | ||||

| UK Bond issuers – All currencies H1 2010 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | Barclays Capital | 23,018.10 | 15.2 | 39 |

| 2 | RBS | 15,441.70 | 10.2 | 44 |

| 3 | HSBC | 13,045.30 | 8.6 | 36 |

| 4 | Lloyds Banking Group | 10,844.10 | 7.2 | 22 |

| 5 | JP Morgan | 8,757.00 | 5.8 | 32 |

| 6 | Deutsche Bank | 7,161.10 | 4.7 | 22 |

| 7 | BofA Merrill Lynch | 5,585.30 | 3.7 | 11 |

| 8 | UBS | 5,250.40 | 3.5 | 11 |

| 9 | Citigroup | 5,189.10 | 3.4 | 13 |

| 10 | RBC Capital Markets | 4,996.90 | 3.3 | 8 |

| Industry total | 151,006.30 | 100 | 222 | |

| Source: Thomson Reuters | ||||

| UK Bond issuers – All currencies 2009 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | Barclays Capital | 60,536.10 | 20.8 | 83 |

| 2 | RBS | 46,390.30 | 16 | 82 |

| 3 | HSBC | 31,421.30 | 10.8 | 75 |

| 4 | Goldman Sachs | 18,863.80 | 6.5 | 23 |

| 5 | JP Morgan | 16,823.10 | 5.8 | 39 |

| 6 | Deutsche Bank | 15,107.60 | 5.2 | 37 |

| 7 | Citigroup | 11,967.70 | 4.1 | 24 |

| 8 | BNP Paribas | 10,640.90 | 3.7 | 39 |

| 9 | Morgan Stanley | 10,327.20 | 3.6 | 26 |

| 10 | Lloyds Banking Group | 9,958.60 | 3.4 | 25 |

| Industry total | 290,467.70 | 100 | 322 | |

| Source: Thomson Reuters | ||||

| UK Bond issuers – All currencies 2008 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | RBS | 45,976.60 | 18.9 | 75 |

| 2 | Barclays Capital | 40,539.20 | 16.7 | 68 |

| 3 | HSBC | 29,840.00 | 12.3 | 60 |

| 4 | UBS | 13,845.40 | 5.7 | 39 |

| 5 | JP Morgan | 13,298.50 | 5.5 | 30 |

| 6 | Deutsche Bank | 13,055.10 | 5.4 | 41 |

| 7 | BofA Merrill Lynch | 12,798.50 | 5.3 | 30 |

| 8 | BNP Paribas | 10,947.60 | 4.5 | 61 |

| 9 | Citigroup | 10,092.80 | 4.2 | 24 |

| 10 | Credit Suisse | 7,059.50 | 2.9 | 18 |

| Industry total | 242,819.60 | 100 | 348 | |

| Source: Thomson Reuters | ||||

| UK Bond issuers – All currencies 2007 | ||||

|---|---|---|---|---|

| Bookrunner | Proceeds (US$m equiv) | Mkt. share (%) | No of issues | |

| 1 | Barclays Capital | 88,835.10 | 15.9 | 133 |

| 2 | RBS | 79,828.40 | 14.3 | 151 |

| 3 | Deutsche Bank | 49,676.30 | 8.9 | 122 |

| 4 | HSBC | 42,496.50 | 7.6 | 102 |

| 5 | Citigroup | 34,055.60 | 6.1 | 51 |

| 6 | Lehman Bros Intl (Europe) | 31,938.20 | 5.7 | 33 |

| 7 | Morgan Stanley | 28,635.30 | 5.1 | 58 |

| 8 | BofA Merrill Lynch | 26,163.70 | 4.7 | 62 |

| 9 | Credit Suisse | 23,825.30 | 4.3 | 33 |

| 10 | JP Morgan | 21,458.80 | 3.8 | 51 |

| Industry total | 559,174.90 | 100 | 890 | |

| Source: Thomson Reuters | ||||