When two Warrington housing associations found it difficult to borrow money in 2009, they turned to the local council for help. What they proposed – that the council lend them £10m each – was highly unusual. Councillors considered the request, and appealed directly to the Secretary of State in London for special dispensation to lend the money. It was duly granted.

As far as Warrington Borough Council was concerned, that was the end of that. The global financial crisis was still playing out, and extraordinary times had called for extraordinary measures. But word soon spread and, over the next couple of years, other housing associations – this time from nearby Chester, St Helens and Crewe – began to ask if they too might be able to borrow money.

The council discussed the loan requests, and decided to go ahead. Again, it requested ministerial approval. The response was surprising: sweeping changes under the 2011 Localism Act, which had been passed by the Conservative-Liberal Democrat coalition, had swept away vast swathes of ministerial control over councils. Warrington was told it was free to do as it pleased.

Spotting an opportunity, councillors approved the three new loans and began thinking about how to expand the scheme further. The rationale was clear: Warrington could borrow money cheaply from central government; by lending it on to housing associations at a premium, it could generate a stream of income that would support local services and offset austerity cuts.

Since then, Warrington – a small town between Liverpool and Manchester in the north-west of England once famed for manufacturing steel wire and textiles – has made a name for itself as a serious lender. As of last March, it had lent out £355m to housing associations across the country with plans to lend another £556m over three years. The loans are just one piece of a growing portfolio that also includes a stake in a Hertfordshire bank, a solar park in Yorkshire and sizeable property holdings.

“In a climate of austerity cuts, people would rather you are generating income … rather than just simply making cuts to services,” said Russ Bowden, leader of the council. “Politically and ideologically, people have bought into it. This isn’t money we’ve found down the back of the sofa – we are borrowing money at preferential rates in order to generate income, which is protecting the services that people value.”

According to Bowden, by next year, the return from loans and other investments will generate £30m of additional income for the council every year – more than it collects annually in business rates and enough to cover each year’s spending on services for children and young people.

But however laudable the council’s motives, the extra revenues are underpinned by a massive rise in borrowing: from next to nothing a decade ago to a projected £1.6bn of debt by 2021. As its balance sheet has grown, so has the risk that a borrower defaulting or a fall in property prices might leave the council with a hole in its finances.

BREAKNECK PACE

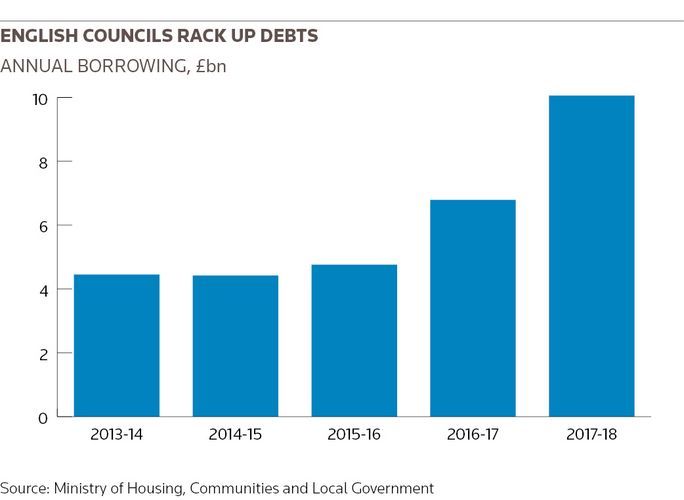

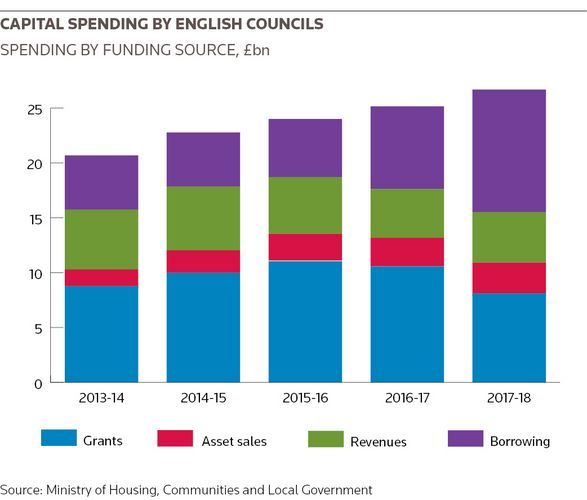

Warrington is far from unique. Across England, councils are borrowing at breakneck pace as they take full advantage of powers granted under the Localism Act. A further loosening of capital spending rules in 2016 accelerated the trend: since then, annual borrowing by local authorities has doubled to £10bn a year, with total outstanding local authority debt expected to surpass £100bn in coming months.

The rise in debt has been left largely unchecked thanks to the unusual way that UK councils borrow money. Council officials just need to make a phone call to the Public Works Loan Board, an arm of HM Treasury, stating how much they want and over what term. They don’t need to explain why they want the loan or how it will be repaid. Within two days, the money is transferred. Last month alone, the PWLB lent councils £700m.

“It’s up to local authorities to determine how much they can borrow … it’s a system of local self-policing,” said Don Peebles, head of UK policy at the Chartered Institute of Public Finance and Accounting, which has written to its members to warn that some recent borrowing is “not consistent with the requirements of fiscal sustainability, prudence and affordability”.

But the appeal to local authorities is clear. According to the Local Government Association, councils across the UK have seen their funding from central government fall by about 60% since 2010. More cuts are planned, and while councils can now keep some of the local business rates they collect, that additional revenue has been insufficient to prevent deep cuts to services. Any extra revenue they can generate is attractive.

But the appeal to local authorities is clear. According to the Local Government Association, councils across the UK have seen their funding from central government fall by about 60% since 2010. More cuts are planned, and while councils can now keep some of the local business rates they collect, that additional revenue has been insufficient to prevent deep cuts to services. Any extra revenue they can generate is attractive.

“Given the lack of autonomy they have over setting local tax rates on council tax or business rates, this is one of the main ways that local authorities can generate additional revenues to offset spending pressures,” said Zoe Jankel, who covers the sector for ratings agency Moody’s. “It is the responsibility of the local authority to ensure that borrowing is affordable, prudent and sustainable.”

But there are concerns that the system of local oversight, twinned with the no-questions-asked loans from the PWLB, has led to some councils taking on too much risk. Many are spending heavily on commercial property: Spelthorne Borough Council in the southern county of Surrey, for example, has racked up over £1bn of debt over the past three years to buy commercial property within the borough and beyond – in central London and Reading, Berkshire.

According to Jankel, the shift of councils becoming landlords well outside their towns is a big one.

“Local authorities have always had property assets, and it would be fair to say that the sector has a very long history of managing properties,” she said, adding that buying property locally can also aid economic regeneration and sometimes lead to an increase in business rates.

“However, holding a portfolio of assets outside their jurisdiction is a relatively new development.”

CALLS FOR CHANGE

There are calls for the current system to be overhauled. Christopher Chope, a Conservative member of parliament, has sought to bring forward legislation that would curtail the use of PWLB funds to buy commercial property. But his private member’s bill needs government backing to progress, and that seems unlikely.

“You would think the government would be interested in tackling this, but they’re not,” he said. “Questions are not being asked. The whole thing is ridiculous … chief executives are being allowed to play the commercial property game at the taxpayer’s expense.

“And it’s all being waved through by local councillors who are often totally inadequate and not in a position to exercise any proper scrutiny.”

Central government has long toyed with the idea of shutting down the PWLB, a 200-year-old institution. In 2010, the then-coalition government announced that the body would be dissolved, and in 2016 a consultation was launched on the subject. The Treasury told IFR that it remains the government’s intention to “abolish the PWLB at the earliest opportunity”.

One major hurdle is what might come in its place. Commercial banks have for many years been pulling back from lending to local governments, although bankers believe that there is huge appetite from bond investors to buy paper issued by UK local authorities, which are considered to be a safe bet because of the implicit guarantee of central government.

One major hurdle is what might come in its place. Commercial banks have for many years been pulling back from lending to local governments, although bankers believe that there is huge appetite from bond investors to buy paper issued by UK local authorities, which are considered to be a safe bet because of the implicit guarantee of central government.

But efforts to wean councils off the PWLB and fund themselves in markets have largely come to nothing. Dozens of councils – including Warrington – pooled resources to set up the UK Municipal Bond Authority, which was supposed to be the future of local authority financing, helping councils raise funds together in the market. A bond deal has supposedly been imminent for the last four years, but nothing has come. The UKMBA didn’t respond to requests for comment.

One banker involved in discussions said bringing the first UKMBA deal was “like herding cats”. Councils generally like to raise small amounts as and when they need it, but bond investors typically expect a minimum £100m deal size. The plan was that councils might pool their needs and come together – until they realised that would make them collectively responsible for each other’s debt.

ADDITIONAL COSTS

And while the PWLB remains in existence, bankers and councillors say it makes no sense to go to the difficulty - and pay the necessary fees – to tap bond markets.

“The whole sector lies in the shadow of the PWLB, which is a really easy and cheap source of liquidity,” said Matt Thomas, a UK debt banker at Barclays. “It should be ripe for the public and private bond markets, where investors are very keen to lend to the sector, but the PWLB has made that very difficult … It comes back to the same problem of pricing and of costs.”

Many believe that a move to a more market-based system of funding might also instil a little more discipline into local governments, and add an extra layer of scrutiny – in terms of ratings agencies, bond analysts, investor roadshows and pricing metrics – that could feed back into the council decision-making process and local politics, and help flag financial issues well ahead of time.

At present, the PWLB system, where loans are issued with a fixed interest rate determined by the Gilt yield that day, doesn’t reward or punish councils for the state of their finances.

FINANCIAL PROBLEMS

Recent problems in Northamptonshire County Council, which got into financial difficulties last year and was taken over by administrators, are a reminder of just how precarious council budgets are. Its finances were criticised in a post-mortem report for being “an exercise of hope rather than expectation”. The concern is that the same might be true at other councils that are much more leveraged than Northamptonshire.

Problems could come in many forms: a fall in commercial property prices, or the default of a single housing association that has borrowed money, would lead to writedowns that would hit a council’s annual budget. It would be local people – rather than the PWLB or private bondholders – that would be first hit, since there is at present no legal channel for a local authority to declare bankruptcy or restructure its debts.

Still, with further cuts to budgets coming, and the PWLB still meeting all requests that come its way, the incentives for continuing the current borrowing-to-invest practice remain high.

For Warrington council leader Bowden, the choices are clear.

“Councils don’t want to be doing this,” he said. “It’s been born out of necessity due to austerity cuts. We would never have had the time or inclination – or necessary skills – at that time to pursue this kind of agenda if we’d been properly funded to do the day job, which is providing services to the people of the town."

“In the same way that austerity is a political choice, this is our political choice to look at generating income rather than be passing cuts on to residents.”