The easing of the eurozone crisis has encouraged sovereign bond investors to start differentiating between peripheral countries that had once been lumped in one basket.

Three years ago when the euro appeared on the brink of disintegration, paranoid bond investors could be forgiven for adopting a simple pair of trades: dump debt of peripheral countries and buy core sovereign paper.

Yields on sovereign bonds of countries on the southern and western edge of the single currency area soared to historic highs while borrowing costs for Triple A rated debt of the core countries plunged almost to zero.

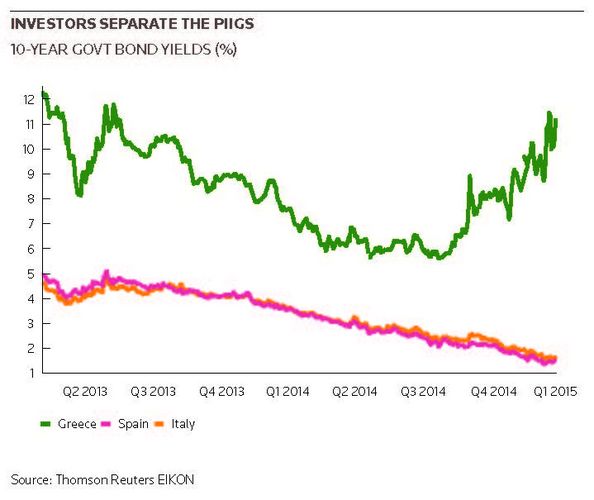

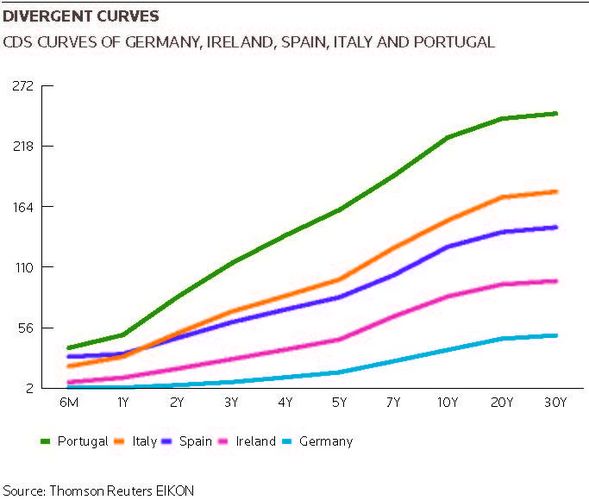

Since then spreads have narrowed. But while there is still a gulf between the “safe” core and the periphery, recently gaps have opened up between Portugal, Italy, Ireland, Greece and Spain.

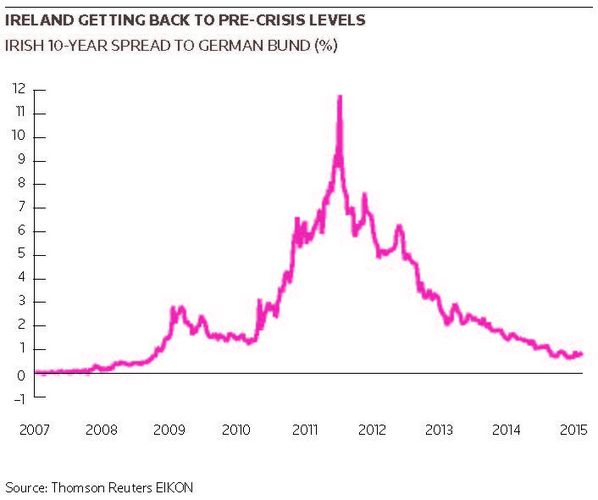

A key moment was in early December when Standard & Poor’s cut Italy’s sovereign credit rating from BBB to BBB–, just one notch above junk, on the same day that it raised Ireland’s credit rating to Single A, rewarding the former bailout recipient for what it said was solid economic growth.

Ireland embarked on a tough austerity programme, which caused great misery in terms of falling house prices and rises in unemployment.

Frank Gill, director of European sovereign ratings at S&P, points out that Ireland was better able to cope as an open economy where exports are about 100% of GDP compared with Portugal or Spain, whose export weighting is closer to 30%. “One of the features of implementing tough fiscal consolidation – austerity – is that the multiplier effects in an open economy are much smaller than in a closed economy,” he said.

This distinction is reflected in the bond markets, said Sean Taor, head of debt capital markets Europe at RBC Capital Markets. Portugal’s 10-year bonds are at 2.60% compared with Ireland’s 10-years at 1.15%.

“Ireland is trading much tighter than Portugal, Italy and Spain, because investors have seen what the country has done and its commitment to reform,” Taor said. “The Irish had a painful crisis but they quickly addressed the issues and reformed, and then recovered very quickly. That is harder in other parts of Europe.”

Strong fundamentals

According to an analysis of credit default swaps carried out by S&P for IFR, investors have actually moved ahead of ratings agencies. Prices of CDS on Italian debt indicated a rating of BBB– several weeks before S&P cuts its rating, while Irish investors now see Ireland as an AA rated country.

Cagdas Aksu, European rates strategist at Barclays, agreed that Ireland is seen as separate from the periphery and closer to the core, saying: “It has shown the market its strong fundamentals and it has gained the confidence of investors in terms of its ability to come back to the market very successfully. In that sense Ireland is in the same bucket as Italy and possibly some of the semi-core countries.”

Russel Matthews, senior portfolio manager on the investment-grade desk at BlueBay Asset Management, said investors were looking at countries that had reduced their deficits and were now in a strong position.

“We would point to Ireland but also point to some of these Eastern European countries such as Slovakia, Latvia, Lithuania and Slovenia as countries that over the medium and long term would perform better in that scenario.”

While all peripheral countries are weighed down by high debts, the issue for investors is how serious the periphery countries are in undertaking the reforms, particularly to labour markets, needed to reduce their deficits.

Christian Schulz, senior European economist at Berenberg Bank, said investors were now looking at which countries were serious about undertaking the far-reaching economic reforms. “There is a divergence in the periphery between those that had reform programmes and those that did not,” he said.

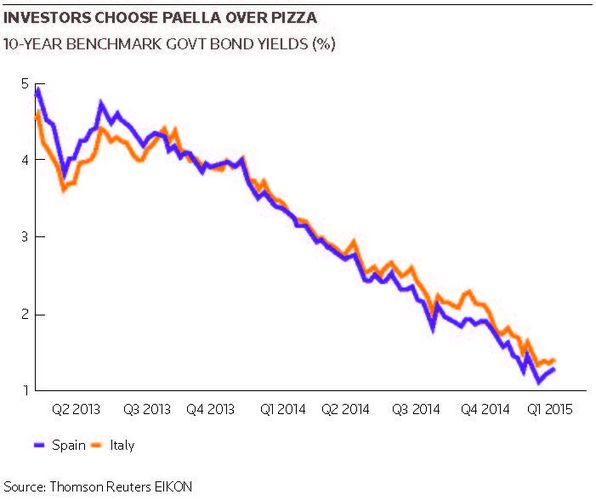

One example is Italy, which managed to avoid a bailout but has also dodged serious economic reforms, and Spain which had to go cap in hand to the eurozone’s bailout fund, the European Stability Mechanism, but which has managed to push through a tough reform package.

“For months and months Italy has been paying significantly more than Spain and that used to be different, so there has been some crossover,” Schulz said.

In December 2013, 10-year Italian debt carried a yield of 4.11% compared with Spain’s 4.13%. Within a few months that position had reversed and by December Spanish debt was 21bp lower at 1.78%.

There is evidence of employment growth, which Gill said was something investors would look at to differentiate countries. While Spain managed to cut its admittedly high level of youth unemployment between 2013 and 2014, in Italy that dole queue lengthened.

There is a similar story for unit labour costs. The strongest adjustments have taken place in peripheral countries – Spain, Portugal, Greece. Wage moderation has boosted corporate margins in Spain in particular. In contrast, wages in France and Italy have continued to increase.

“Excluding Greece, non-core Europe peripheral countries have performed in similar ways but there are still some very big differences. There are still big differences between how investors are pricing the periphery,” said Taor.

“Political risk is significant in 2015 and we face a political cycle that has a lot of uncertainties and a negotiating phase with the Greek government that will be very difficult and tortuous”

Spain was rewarded in January with €22.8bn of demand for a 10-year bond issue that raised €9bn at a record low coupon of 1.6%.

Ultimately, what bond investors look for is debt sustainability. Many factors go into this but the most crucial is nominal growth. “If you ever want to repay your debts then growth is a pretty important prerequisite,” said Schulz. “Italy has never really got out of stagnation and, given its very high debt pile, growth is very important.”

The standout example of differentiation is Greece. (For more on Greece, see ”Watching, waiting, worrying” and “Under new management”.)

A survey of 40 academic economists by the UK’s Centre for Macroeconomics found six out 10 did not think that the Syriza victory would cause interest-rate spreads for other countries in the eurozone periphery to increase significantly or for a sustained period.

One factor that helped keep all eurozone bond yields compressed over recent months – and much lower than they were during the crisis – was the speculation over the launch of quantitative easing by the European Central Bank at its January meeting.

“Maybe while under normal circumstances if there had been no prospect of QE prospects whatsoever, these spreads would not necessarily be good value for investors,” said Aksu. “So despite the fact the debt/GDP ratios of these countries are still very high, markets have not been questioning that because the likely portfolio impact of the ECB’s QE was dominating market sentiment.”

Homework rewards

The bank will not start buying bonds until March but already all eurozone sovereign bond yields have started to fall.

“Spain, Ireland, Italy and Portugal are continuing to see their yields come down because of expectations around QE,” said Taor. “They have access to the bond markets, at record low yields, and have each issued very successful syndicated benchmarks in January alone. The market believes they are taking the required measures, and are continuing to reform and prosper because of it.

“If you look realistically at what investors have to buy and can buy, and what the alternatives are, they have to put their money somewhere when German government yields are negative up to six years from now.”

Cagdas said the trigger for a new round of differentiation could come in months later if markets decide QE has not succeeded in reversing deflationary risks in the euro area.

“If investors decide that Europe is going to continue to head towards deflation, then debt sustainability questioning might come back to the table,” he said. “If you combine this broadly weak growth together with very low inflation expectations, your debt sustainability profile is going to look worse.

“Markets will reward the countries who have done their homework and used the time bought by the prospects and implementation of QE to do the structural reforms. It is the timing and how much homework has been done that will determine who benefits and who suffers when the debt sustainability concerns return.”

In the meantime, the uncertainly created by negotiations between the new Greek government and the Troika of the ECB, European Commission and the IMF could be exacerbated by the prospect of elections in Spain and Portugal later this year.

Gill at S&P pointed out that Spain’s rising eurosceptic party Podemos advocates a “citizen’s audit” of public and private debt and a default on debt that is deemed “illegitimate”.

“Political risk is significant in 2015 and we face a political cycle that has a lot of uncertainties and a negotiating phase with the Greek government that will be very difficult and tortuous,” added Matthews at BlueBay.

“You have the political cycle on the one hand and immensely powerful force of the ECB on the other, they will drown out the fundamental economic differentiation on a standalone domestic idiosyncratic basis.”

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.