It has been a huge year for the covered bond market, which has taken up the slack left by the disintegration of parts of the sovereign debt market. Established markets have seen record-breaking issuance while newer jurisdictions, from the US in the west to Australia in the East, have been busy preparing the ground, hoping to join the party. Peter Carvill reports.

To view the digital version of this report, please click here.

In July 2008, following nearly a year in which the world’s financial markets went through a period more tumultuous than any other in living memory, Henry Paulson, then US Secretary of the Treasury, declared: “We are at the early stages of what should be a promising path, where the nascent US covered bond market can grow and provide a new source of mortgage financing.”

Paulson’s predictions of growth have largely born fruit. In the foreword to the European Covered Bond Council’s 2010 European Covered Bond Factbook, Antonio Toro, chairman of the ECBC, and Annik Lambert, secretary general of the European Mortgage Federation, wrote: “Against a backdrop of ongoing turbulence in capital markets, the covered bond market continues to expand. In 2009, total outstanding covered bonds grew five per cent to €2.4trn, over 30 new issuers joined the market in 2009 to bring the total number of issuers to more than 300 and, today, at least ten countries are considering the introduction of covered bonds.”

The council’s own statistics more than bear this optimism out. Between 2003 and 2009, the value of European covered bonds outstanding increased overall by 59.5%, registering year-on-year increases. The number of total bonds issued within the same period climbed by nearly a third. Anecdotal evidence not only corroborates this but suggests that the market experienced further improvement in 2010, leading into 2011.

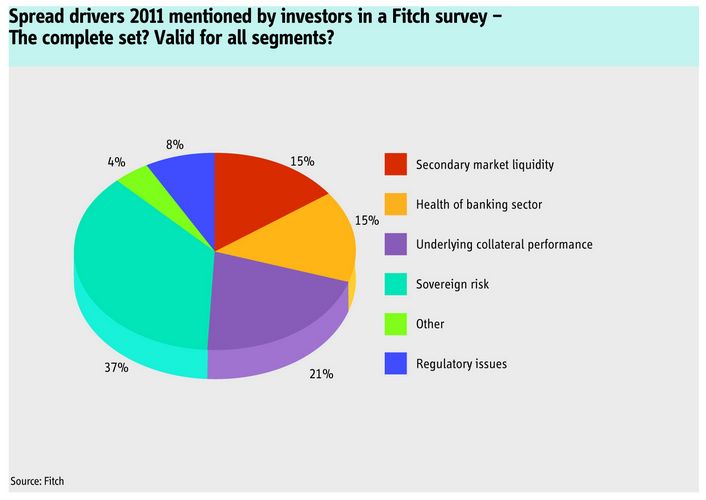

There are a number of reasons for this, said Richard Kemmish, director of fixed income at Credit Suisse. Firstly, the product has moved into the mainstream. Last year, he said, there were over a hundred issuers within Europe, a composition of the sector that he referred to as ’granular’. It was a situation never before seen, occurring, Kemmish said, because of a growing awareness among investors of the resolution regime.

“It’s the idea that bonds, in holding on to what we call ’senior unsecured debt’, are potentially going to take losses on an ongoing basis,” said Kemmish. “That’s made people question the asset class in general, and to want to put on protection against that risk. If you look at covered bond spreads, they’re not very much tighter than spreads on senior unsecured debt. You’re paying a relatively small differential to get a lot of extra protection.”

Regulatory support has also helped. Despite noises in many quarters of tightened regulation, the covered bond market appears to have escaped the authorities’ ire. “There’s an attitude amongst regulators that covered bonds are not part of the problem that caused the credit crunch but part of the solution that will take us out of it,” said Kemmish. “The market was seen to stay open for banks funding through the crisis.”

Kemmish’s third reason for the market’s growth lies in the nature of the product. “The more covered bonds that you issue, the more difficult it is to issue your own unsecured debt. So you have to keep issuing covered bonds. To some extent, that’s what we’ve started to see this year: issuers with not-so-good access to the covered bonds market beginning to shift very substantial amounts of their funding into the products. That’s why this year has been a crazy year for covered bonds.”

New World potential

Outside of its traditional European stomping ground, the market has been seeing major legislative moves within the US, Australia and New Zealand.

Stateside, the Covered Bond Act is being worked through Congress and the Senate. Tim Skeet, managing director of debt capital markets for RBS, was asked to testify before the Capital Markets Sub-Committee of the House Financial Services Committee on March 11 2011. There is, he said, still some controversy around the US covered bond law proposal because of the role of the FDIC and the ongoing questions around structural subordination.

“There’s a compelling case for introducing covered bonds into the US,” he said. “But because of the way the resolution framework operates there, there is still some question as to whether covered bonds are the product that’s best-suited and best-fitted. I think they are, but there is debate which has to be fully resolved. That’s why every time this topic raises its head, it’s not all a one-way discussion.”

The debate illustrates an interesting difference between the perspectives that prevail on either side of the Atlantic. “Everyone over here in Europe believes that this is what they should be doing in the US,” said Skeet. “That’s the nature of any public debate and it’s right that they should be doing that. What’s compelling for us in Europe isn’t always as compelling for them over there.”

Kemmish is more bullish, insisting that the bill not only enjoys support in both Democratic and Republican circles, but that it should pass Congress. However, he added, he is not clear as to its immediate future within the Senate.

“Ultimately it’s seen as a potential alternative to Fannie and Freddie,” explained Kemmish. “The agencies have dominated housing finance for such a long time but, as they’ve had so many problems, you need an alternative way to finance mortgages. Most people agree that covered bonds are part of that.”

Although the political debate continues to rage, the US will be home to a massive covered bond market within a few years, Kemmish predicted.

On the other side of the world, Australia and New Zealand made moves in 2010 on entering the covered bond market. In the former, Wayne Swan, the Treasurer of Australia, said that the country would make changes to its financial regulations to allow for the introduction of covered bonds. A report in The Wall Street Journal in December 2010 stated Swan would also allow credit unions and building societies to produce covered bonds.

Swan was also reported to be bringing in legislation to allow government securities to be quoted on a securities exchange, deepening any covered bond market in Australia. All of this was followed on March 24 by draft legislation for Australia’s domestic banks to produce their own covered bonds. Under those proposals, Australian banks will be allowed to hold up to 8% of their total assets this way.

Bank of New Zealand also launched its first covered bond programme last year.

It is indicative of a general trend. “The Canadians have been the largest non-European market for a while but lot of countries are now catching up,” said Kemmish. “The first New Zealand issuers have come and the first Australians will arrive soon. The regulators in those countries have, in the past, focused on the structural subordination issue. Increasingly, they’ve come to realise that access to funding is far more important. It’s not easy to put into place a legal framework; there’s a lot of vested interest and a lot of laws need amending.”

Calm in a crisis

Within the EU, 2010’s narratives centred on the sovereign debt crisis experienced across some of the region’s member states. The completion of the European Central Bank’s Covered Bond Purchase Programme, which saw the central banks of member countries purchase €60bn worth of European covered bonds, was also a defining moment.

The debt crisis posed unprecedented challenges. It was almost impossible for bankers, regulators and politicians to stay ahead of the crisis, with the political and social effects of the crisis often driving the solution.

“We look at what went on and there’s a human dimension,” said Skeet. “It’s not just about pieces of paper and macro-economic decisions but also about human lives, which makes it very tough. So I think we have to look at it responsibly and say clearly that we need to see a quieter, more reflective and more pragmatic market.”

The ECB’s programme to purchase €60bn of covered bonds was completed on 30 June. Despite the steep price tag, the amount purchased by the ECB was a minuscule share of the overall market, said Kemmish, which he valued at closer to €2.7trn.

The ECBC’s 2010 European Covered Bond Factbook declared theprogramme a great success, calling the impact “exceptional”. However, the chapter authors – Frank Will, head of covered bond strategy, and Sophia Kwon, senior covered bond strategist, both of RBS – added a caveat regarding “domestic bias”. It concluded: “The German, French and Italian issuers benefited disproportionately whilst the Greek, Spanish and Portuguese markets, despite having arguably the highest needs, received less support due to their lower outstanding covered bond volumes.”

It was also argued that while the interference of the ECB had reinvigorated the market and accelerated its recovery, the market would have recovered by itself.

“Most of the buying was in secondary rather than primary,” said Kemmish. “Structurally, the covered bonds market had too many bonds. The street was too long, there were people who were forced sellers,” a problem by no means confined to the covered bonds market. “What the programme really did was not buy bonds that people otherwise would not have bought but sucked some of that excess inventory out of the market.”

Where the market comes from now seems obvious: the actions of the ECB and the optimism of the ECBC point to a golden future. As markets begin to loosen on the macro-scale and households budget begin to loosen on the micro, it may be that the market has room yet still to grow.