Latin American cross-border bond issuance has been reduced to a trickle after a record start during the first quarter. European debt woes have been threatening to close the markets over the summer and beyond as investors fret about the impact of a Greek exit from the eurozone. Yet deals can get executed, and at attractive costs, if borrowers can bear the brunt of higher new issue premiums.

To view the digital version of this report, please click here.

Hopes of a revival in high-yield issuances have faded somewhat with bankers focusing on blue chips and the record low coupons they can potentially achieve as US base rates hit record lows as investors flee to the relative safety of US Treasuries. Yet constantly shifting sentiment has exacerbated execution risks in a market constantly under the threat of headline risk.

Still, inflows into emerging market bond funds and dearth of supply in Europe mean cash has been accumulating on the sidelines and is ready to be put to work in high quality Latin American credits denominated in both dollar and to a lesser extent euros.

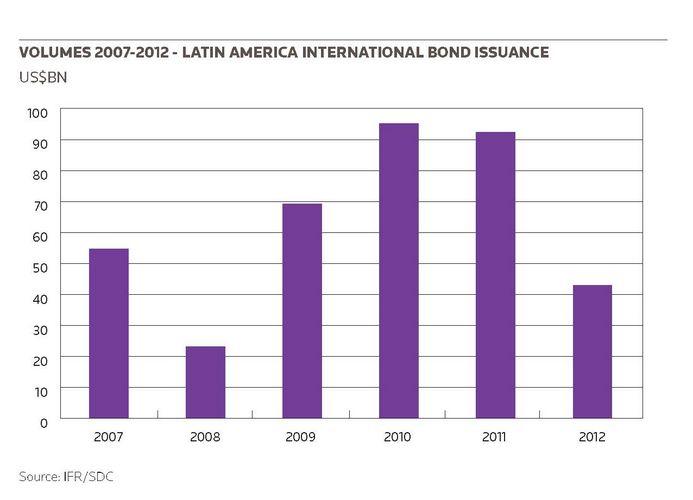

Despite the dramatic slowdown in issuance in May, so far volumes on are on pace to meet last year’s total of US$91bn. The region had already seen more than US$45bn in cross-border bond issuance this year until late May, though activity has declined after a bumper January and February. Those two months saw combined volumes hit US$32bn. In contrast, May, April and May only produced US$8.2bn, US$2bn and US$1.4bn.

The rush to print early in the year was driven partly by the numerous corporates that were sidelined last year and a sense that the environment in the international capital markets could potentially become more volatile later in 2012. Similar arguments were also applicable by the second quarter as concern about the fallout from Greece and Spain became more acute.

“Volumes to date have surpassed last year,” said Katia Bouazza, co-head of global markets, Americas, at HSBC. “We told a number of issuers to come sooner in the year as we saw some additional volatility.”

A senior syndicate official echoed similar sentiments. “Hats off for people who jumped in early. They correctly predicted that the scenario was too rosy for reality,” he added.

It’s all Greek

In May the buyside was firmly on the sidelines or sticking to safe liquid names until the second round of Greek elections on June 17 provide some clarity on the direction of European risk. “It is all Greek to me. That is what matters now,” said an investor focused on LatAm and other EM corporates.

Until the middle of May, external debt funds had been seeing net inflows, which was a positive. But the latest EPFR data show that investors are becoming increasingly risk averse, with both hard currency and local currency funds seeing net outflows in the week to May 23.

At least the build-up of cash positions should provide support to the primary markets if European policymakers can generate greater comfort levels. But some believe a more positive outcome in Europe may even result in a significant reversal of EM debt flows as investors become less risk averse.

“At some point, if things start to look better, I’m sure we’ll see big reallocation out of fixed-income into equity,” said a syndicate manager.

For now, markets remain open for investment-grade LatAm credits, which could still take advantage of low absolute yields, although new-issue premiums will be considerably higher. “New-issue premiums are 30bp or 40bp higher, but that is not a lot in the grand scheme of things,” said a syndicate official.

LatAm DCM bankers have been keeping a close eye on the US high-grade market, which has had a mixed performance. For many a US$8.9bn multi-tranche offering from United Technologies was illustrative of the enormous amounts of cash on the sidelines and of how top quality LatAm credit could lock in ultra-cheap financing.

“United Technologies’ blended average cost of funds across the six tranches was 2.90%,” said Clayton Pope, who heads Credit Suisse’s EM syndicate desk in New York. “A US$40bn book for an intraday execution is evidence that there continues to be a substantial amount of high-grade cash to be deployed, which is definitely there for storied LatAm issuers looking to fund at record low absolute yields.”

But for now investor reaction to Europe’s debt crisis will probably be the principal driver of EM and LatAm credit performance and ultimately new issuance activity over the coming months.

The market’s constant switching between risk-on and risk-off sentiment towards Europe has affected the “performance mechanics” of EM credit and has become a “new systemic risk factor” that has taken away from fundamental analysis, said David Masse, an analyst at Prudential Asset Management, at recent EMTA panel.

Liquidity is king

Against this backdrop, smaller debut names, high-yield issuance and local currency trades are likely to be put on the backburner unless there is a dramatic turnround in sentiment, said bankers. Investors are putting a premium on liquidity and this will naturally work against these two market segments.

“I don’t doubt you can get a deal done,” said Bouazza. “The question mark is for the smaller deals and high-yield names. It is not because there is no appetite, but because they are smaller, and in a volatile environment investors tend to go to more liquid names.”

Last year, local currency was a big theme, with several borrowers tapping Global Real bonds and Mexico’s Pemex coming with the region’s first corporate global depositary notes, but the mixed performance of recent corporate global Real issuance as Brazilian authorities imposed further capital controls to contain the appreciation of the currency has left investors wary of this asset class.

With the Central Bank seemingly content with letting the Real trade around 2 against the dollar, some are wondering whether this could be a good entry point for investors. But a volatile market backdrop and investors’ need for liquidity may in the end hold back a revival in this asset class, at least in the short-term.

“When it comes to offshore local currency deals, keep in mind the market is only receptive when it is a frequent borrower and it comes with a large liquid format,” said HSBC’s Bouazza.

This combined with increasingly lower cost of funding in the local markets may mean that fewer Brazilian corporates, at least those with local currency revenues, will try the international capital markets.

“The debenture market is very strong,” said a senior syndicate official in New York. “Local rates are not dramatically different from what you paid a few years ago.”

If more Brazilian companies decide to fund closer to home, this could have an impact on volumes by year-end, considering that the vast majority of international LatAm bonds come from Brazil. Of the US$43bn issued year to May, about US$23bn came from Brazilian corporates, US$1.9bn from Chile, US$1.6bn from Colombia, and US$7.1bn from Mexico.

Euro hopes

This comes as opportunities may be opening for high-quality Latin American names in the euro market as European investors watch cash levels rise amid a dearth of supply from local issuers. Mexican state-owned oil company Pemex was meeting European investors in May, while Latin American telecoms America Movil was also considering such an option in the wake of its bid for Dutch phone company Royal KPN.

“We are seeing an increasing interest from European investors to bring EM credits,” said a DCM banker. “They are looking to diversify.” With risks in Europe increasing, investors from the region would welcome an investment-grade company from Latin America that generated a pick-up over similar European credits, he added.

However, only a handful of LatAm corporates could move quickly enough to take advantage of such demand, mostly those that have already tapped this market. Aside from America Movil the list includes Petrobras, Vale, Pemex and Banco do Brasil.

The question is whether or not it makes sense for borrowers from a pricing perspective versus their dollar curves. Some bankers believe that the relative strength of the secondary market in euros versus dollars could make pricing attractive.

“Some bonds in euros have rallied more than dollars and, even if the swap conditions are not good, [pricing] could be balanced by the rally in the secondary,” said a banker at a European institution.

However, the five-year basis swap cost from euros to dollars had climbed from around 35bp in April to 60bp in late May as concerns over Europe’s debt crisis intensified, said one banker.

In this environment, companies such as Pemex would still have to pay some 50bp over its dollar curve and, although Pemex does not have a standard rule of thumb, it is thought that this was still too high a cost to diversify its funding base. Other issuers may feel the same.