A fistful of dollars: US dollar bonds were the best (and sometimes only) funding solution for many issuers in 2012. And whether it was in the US, Europe or Asia, one bank stood out in making dollar deals happen. With unmatched execution across products and regions, JP Morgan is IFR’s US Dollar Bond House of the Year.

Issuers from all over the globe turned to US dollar bonds. Dollar-denominated issuance totalled a whopping US$900bn in the IFR Awards year.

In the midst of such a red-hot market, JP Morgan eclipsed its competitors in the league tables. Over that period, JP Morgan captured an 11.8% share of the overall high-grade and high-yield market for dollar bonds, leading 510 deals totalling US$106.3bn. That was well ahead of closest rival Citigroup, which had a market share of 9.3% after leading 432 deals for US$83.8bn.

But the raw numbers alone do not tell the whole story of the impressive performance of JP Morgan, which is IFR’s High-Yield Bond House of the Year as well as its Global US Dollar Bond House.

Quality of execution, and superb distribution across products and regions, made the bank the clear standout this year.

In a market that saw low-coupon records broken regularly, underwriters were under more pressure than usual to deliver clients the most cost-effective funding solution. And JP Morgan managed to meet those expectations consistently.

“We blazed the trail in capital markets in 2012,” said Huw Richards, JP Morgan’s co-head of investment-grade finance. “We helped our clients set low-coupon records, navigate volatile markets, re-optimise debt portfolios, achieve mission-critical financings across products, and access different markets.”

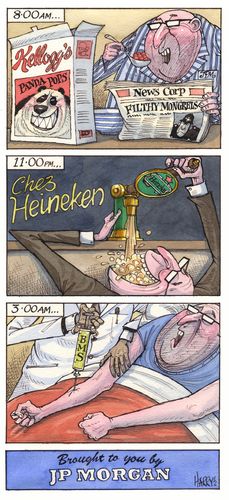

In the US, JP Morgan was one of six bookrunners on the late July deal from Bristol-Myers Squibb, which sold a US$2bn three-parter with the lowest ever corporate bond coupon in the five and 30-year tenors. It was the first time a five-year printed inside of 1%, eventually winding up at 0.875%.

The bank was also underwriter on transactions for Texas Instruments, Unilever, Sysco, Colgate, Heineken, Walgreens and Kellogg’s – all of which set low-coupon records.

It also succeeded in getting some particularly tricky deals done. Smiths Group pulled its US$400m trade after it was led by other bookrunners – but JP Morgan got it priced in October.

When News Corp was getting deluged with negative headlines (and litigation), JP Morgan priced a US$1bn 10-year transaction while serving as sole active bookrunner – itself an achievement.

The bank’s distribution capabilities ensured the issuer got an attractive pricing with the lowest 10-year Triple B media coupon at the time, and one of the lowest Triple B prints ever.

Making a big deal

When it came to jumbo trades, JP Morgan was the only bank to be an active bookrunner on every one of the 10 largest trades of the year, and the only one on the three biggest liability management deals as well. It was also a bookrunner on market-defining spin-off deals such as those for Phillips 66 and Kraft Foods.

“The key strategic development in the US market in the past year has been spin financings and JP Morgan is the only bank to have been on all of those transactions,” said Richards. “We were a market leader underwriting strategic, complex and debut transactions for US financial institutions.”

The Phillips 66 and Kraft trades were complicated and needed strong execution given the volatile state of the markets.

Phillips 66 was a wholly-owned subsidiary of ConocoPhillips and it raised US$5.8bn through a debut bond on March 7. Proceeds were to be held in escrow until the spin-off was completed. Educating investors about the transaction was critical in ensuring its success, as the company was largely unknown to investors.

The bookrunners got management to conduct calls with 45 investors and even hosted a global investor call on the day of execution, which ensured participation from more than 100 accounts. The book comprised over US$22bn in orders, guidance was tighter than initial price talk, and the deal finally priced at the tight end of guidance in all tranches.

It was not a major acquisition financing year, but most of those deals that were announced this year or funded through the US bond markets were mandated to JP Morgan. Among them, the bank was on Heineken’s four-part financing that funded a US$2.5bn bridge facility to finance the acquisition of Asia Pacific Breweries.

JP Morgan also excelled in executing US dollar bond transactions for clients in the high-yield markets.

For the 2012 awards period, JP Morgan stood out on top as it spearheaded US$70.5bn in issuance from 110 high-yield deals for a market share of 20.1%.

In the US, the bank also topped the lead-left league tables for the awards period, pricing US$64.45bn from 102 issues for a market share of 21.7%. Total US issuance for that period amounted to US$291.16bn.

JP Morgan also dominated the market when it came to first-time issuers, handling deals for Air Lease, Neuberger Berman, Inmet, Ladder Capital, NCR, EP Energy and others.

“These are all mission-critical deals,” said Jim Casey, JP Morgan’s co-head of global debt capital markets. “You don’t want to fail on your first foray in the market.”

Looking east

In Asia, JP Morgan did a superb job of delivering the US bid for Asian issuers.

The bank’s dollar deal roster includes transactions from some of the region’s most sophisticated borrowers – for rated and unrated names, corporates and sovereign issuers, and in jurisdictions as diverse as Australia and Mongolia.

The quality of the issuers that mandated JP Morgan for their dollar deals speaks volumes. From BHP Billiton in Australia and Hutchison Whampoa in Hong Kong, to Samsung in Korea and CapitaLand in Singapore, Asia’s best issuers consistently mandated the bank this year.

Australia has long been a market where JP Morgan is strong, and this was the case again, with the bank arranging multiple deals for the country’s corporate aristocracy. In the period under review, the bank did multiple trades for BHP Billiton, National Australia Bank and Commonwealth Bank of Australia. In Korea, the bank’s performance was equally strong, with the bank arranging dollar deals for likes of Hyundai, Samsung and Kexim Bank.

However, it was not just Asia’s corporate aristocracy that turned to JP Morgan. So too did many unrated issuers. Sinopec, China Resources Gas, Mongolian Mining Corp and MMI International were but a few of them.

Even more impressive than the breadth of the bank’s deals was the number of landmark and innovative trades.

Doosan Infracorp’s US$500m 30-year non-call five hybrid, for example, was the first corporate hybrid issue done out of Korea and demonstrated JP Morgan’s structuring skills.

The deal’s bespoke structure gave investors a put option after the fifth year, subject to certain events, which JP Morgan and fellow arrangers Citigroup and Korea Development Bank funded. This feature anchored the deal’s pricing and enabled the deal to get done at 20bp inside of initial guidance at 265bp over Treasuries.

Chinese state-owned Sinopec’s US$3bn debut global benchmark offer was equally impressive. It was the largest ever corporate bond from China and the biggest deal from an oil and gas sector issuer in Asia since 2009. The deal’s order book, with more than 300 accounts committing US$19bn, was the largest since 2009 and again underscored JP Morgan’s distribution prowess.

In the sovereign space, the bank was on the Republic of Indonesia’s US$2.5bn issue, which comprised a new US$500m 10-year issue and a US$2bn tap of its existing 2042 bonds. The deal was many times oversubscribed, and Indonesia will have been especially pleased with the cheapest money it had ever achieved for either 10-year or 30-year paper at 3.85% and 4.95%, respectively.

The bank also arranged a rare issue from Korean electronics giant Samsung. The US$1bn five-year issue priced at 1.829%, inside the Korean sovereign and the lowest ever five-year coupon from an Asian issuer. The order book stood at US$4.4bn from 160 accounts, impressive demand given the deal’s tight pricing.