Keith Mullin looks back on the era when Japanese banks surveyed the international markets from a position of apparently unassailable strength.

Take a look at any broad yardstick of international investment banking achievement today. Four of the Japanese Big Five CIBs and investment banks – Mitsubishi UFJ, Sumitomo Mitsui, Mizuho, Nomura and Daiwa – are in the top 20 of global fee earners. Yet at the same time, it is probably fair to conclude that their positions in M&A as well as debt and equity underwriting are modest relative to their size and stature. Their combined market share is just 5% of the global IB wallet and that includes their domestic market exploits.

But it was not always thus. During Japan’s modern-day financial Golden Era, whose zenith was between 1987 and 1990, the country’s Big Four securities firms (Nomura, Daiwa, Nikko and Yamaichi) came to dominate the combined Eurobond and Euroconvertible business. And they used the huge revenue streams they derived from their presence in Japan-related primary and secondary markets to build out their capital markets origination, distribution and trading platforms, and to broaden their product coverage outside of Japan after the asset-inflation bubble burst.

In the years leading up to the real estate and stock market crash of 1989–90 and before the “lost decade” of economic stagnation and decline, the Japanese had the look of unstoppable world-beaters. During that period of rapid growth, their presence in London reflected their new-found stature: the Japanese houses became patrons of the arts, sponsoring high-profile classical music events, opera and theatre productions, museums and art galleries; moving and shaking with City glitterati; and rubbing shoulders with its leaders in the corridors of City power and influence. In short, the Japanese had arrived.

But one particular arrival that was to become very significant in cementing the rise and influence of the Japanese in London in those days went largely unnoticed.

“I arrived in London on New Year’s Eve 1987. It was a very strange day; nobody was working and the only restaurants that were open were Chinese,” recalled Takumi Shibata, chairman of Nikko Asset Management since July 2013 but before that a 36-year Nomura veteran and until last year chairman and CEO of the firm’s wholesale division and COO of Nomura Holdings.

“Prior to my arrival in London, I’d been working in Tokyo as head of the American desk. That was the worst job you can imagine as Tokyo is in a completely different time zone and I didn’t really get much time to sleep. London was the perfect environment in which to operate an international business. It was like being in an amusement park. With the exception of the quality of restaurants, London was a globally diverse place so you could arrive as a foreigner and be accepted,” he said.

Shibata did two stints in London for Nomura, the market powerhouse. During his first, he stayed for six years, initially running debt and equity new issues – keeping Nomura at the top of the Eurobond league table for four years – before gaining a broader role as head of investment banking.

“My predecessor Hiroshi Toda had told me: ‘Hey, Shibata, you need to belong to the boy’s club’, which wasn’t a problem for me as I felt I was a fit from day one. But I asked myself: ‘Do I want to be a part of a club or do I want to form the club?’ I went for the latter and was one of the founders of a group originally called G7. We used to have dinner in Brown’s Hotel, where we would eat, drink lots of wine and criticise each other’s deals. We were a group of naughty boys. That’s when I realised that capital markets boys were by no means true gentlemen,” he joked.

Typical of the environment of the time was Morgan Stanley’s ski weekends. “At Friday lunchtime, I would sneak out of the trading room and catch a flight to Geneva. We had a bus waiting for us at the other end and we would all drink from a bottle of Schnapps so by the time we arrived we were drunk. Then we would all go into the sauna and hope that we would survive. But then we had two days of ski-ing together.”

Having established strong personal relationships in the London market, the Japanese securities firms kicked off their assault on the Eurobond league tables. Their rise through the ranks came in parallel with the ascent of the Japanese stock market. It was also a time of exponential growth in the Eurobond market and a period that saw Japanese financial institutions begin in earnest to grow through acquisition and asset-building outside of Japan, away from the clutches of strict regulations that had stifled the domestic banking and capital markets.

“It was a very stimulating time to be in the business. Clients didn’t have access to the technology that they have today; so when you went to see clients, they relied on your information because they didn’t have access to it first-hand. The mood felt young and ambitious; we had an enormous amount of self-belief and aspiration,” said Paul Morganti, international head of capital Markets at Mitsubishi UFJ Securities International and who entered the market in 1987 at Daiwa before moving to the-then Tokyo-Mitsubishi International in 1996.

“There was a lot more camaraderie; we used to interact a lot more. It used to be a lot more fun; you felt you were part of a community. Our work had a nice buzz to it. It also used to be acceptable for borrowers to do a lot of socialising and throw parties and fund outings. The market today is so commoditised,” said Morganti.

His comments were echoed by Shibata, who said: “I’ve maintained friendships from those days to today. It was a period in which people could exist as true friends. Of course, we would pinch each other’s deals and moan about everyone else’s mispricing but it was a good life. My positive attitude to life came from my London days.”

Grabbing market share

If by 1986 only two Japanese firms – Nomura and Daiwa – had hit the big time and built a combined Euromarket underwriting share of 13%, that changed dramatically in the following five years. In 1987, the Japanese Big Four securities firms were all in the Top 10 and had garnered 30% of all Euromarket debt and equity-linked underwriting. By 1988, IBJ International had also entered the Top 10, making it five Japanese firms in the leading echelons of the Euromarket.

By 1989, the Big Four share had increased to a staggering 40%. Add in the banks and the second-line brokers (such as Cosmo, Kankaku, New Japan Securities, Nippon Kangyo Kakumaru, Okasan, Wako and Yamatane) and that share was closer to 50%. The Big Four’s share remained at above 25% in the two following years and they experienced a rebound in 1995, when the massive Japanese retail investor base unleashed its prodigious buying power in yen and non-yen straight bond product.

Nomura was the notable hold-out in terms of league-table position into the middle part of the 1990s. But by the time the world had moved towards the creation of the euro; the Japanese economy remained in its moribund rut; and many leading banks and brokers were going through a painful round of restructuring, the Japanese had faded from the upper echelons of the Eurobond market. By the end of the 1990s, Yamaichi had gone bust and Japanese banks and securities houses withdrew to maintain a lower international capital markets profile.

No overnight sensation

At the time of the Agefi International Bondletter launch in 1974, the Japanese domestic capital markets were still tightly controlled and heavily regulated, as was the banking sector. Banks were divided into city banks, long-term credit banks, trust banks, regional banks and the Bank of Tokyo, which had a unique role as the country’s specialised foreign exchange bank. Each segment had its own carefully guarded business profiles. Their narrowly defined activities were fiercely segmented and none of the banks were permitted to engage in corporate bond underwriting.

Foreign banks and brokers, too, were severely restricted in their ability to conduct business in Japan. In fact, non-Japanese securities firms were only authorised to set up subsidiaries in Japan in 1985; the same year the Tokyo Stock Exchange launched 10-year JGB futures, the country’s first financial futures contracts and a key hedging tool.

By the 1980s, Japan’s domestic markets were being gradually deregulated. Also in 1985, TDK issued the first non-collateralised senior unsecured domestic bond for more than 50 years; by 1987, hundreds more authorisations had been granted. Observers at the time suggested that domestic bond market liberalisation was prompted by the huge success of Japanese offshore issuance. A commercial paper market was introduced in Japan in 1987.

While Japanese regulators had kept the domestic market under their strict control, they had authorised Japanese companies to issue equity-linked debt in the Euromarkets since 1981 and had granted permission to the commercial banks to participate through offshore subsidiaries. The slowly unfolding process of deregulation meant that domestic banking segmentation was slowly erased but it was only in the 1990s that banks were permitted to underwrite bonds in the domestic market as the weight of client interest shifted away from bank lending.

Expansionary aspirations and domestic deregulation notwithstanding, the story of the rise of the Japanese in the Euromarkets during this period is a story about the ascent of the Japanese stock market in the 1980s. The rise of equity prices in Japan was part of the process of raging asset-price inflation driven by rampant bank-financed speculation, most notably in real estate. The rise in Tokyo real-estate prices was so extraordinary that there were claims, arguably spurious, that the land contained within the walls of the Imperial Palace in Tokyo was worth more than all of the real estate in California combined – or even worth more than Canada!

A sign of those frothy times, corporate issuers began to use the proceeds from capital market issuance not to repay bank loans or fund capex but to engage in land speculation or create exposure to financial instruments that benefited from rising stock prices. In that environment, they felt they could make more money as hedge-funds-by-proxy than, say, as manufacturers.

January 10 1984 was a key date because the Nikkei 225 index closed above 10,000 for the first time. More notable was that it had doubled by February 1987, added another 10,000 points to close above 30,000 by the end of 1988 and gained almost 10,000 more points in 1989 alone, when it closed at its all-time high of 38,916 on December 29 of that year. In those five years, the market had gone up by 292%.

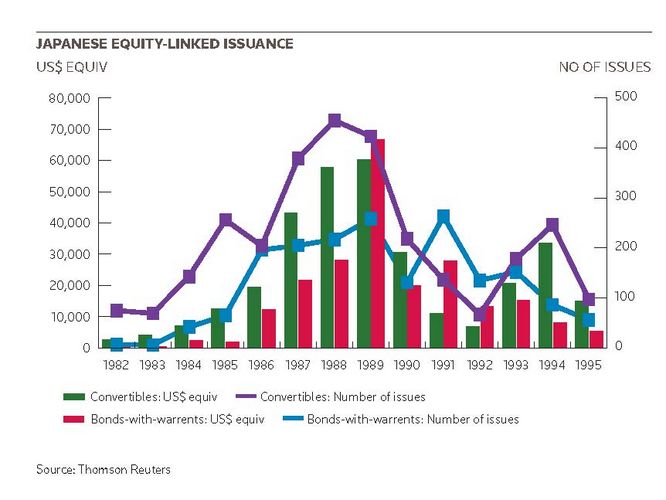

US$435bn equity-linked boom

This period offered Japan’s Big Four securities firms an incredible opportunity to make money, which they took with both hands. The rise in equity prices and a voracious appetite among Japanese companies for capital created the perfect conditions for equity-linked issuance, which enabled borrowers to pay ultra-low running yields in return for giving investors exposure to stock that was always going to move quickly beyond strike or conversion prices.

Warrants were in essence an extremely cheap way of creating leveraged exposure to the Japanese stock market. In the bubble years of 1986 through to 1990, Japanese companies issued a staggering US$435bn in Eurobonds-with-warrants and convertibles. While many blue chips tapped the market, so too did hundreds of SMEs from the TSE’s Second Section that were virtually unknown outside Japan.

An essential tool for every warrant market participant in those days was the Japan Company Handbook, split into one volume for First Section companies and another for Second Section companies. Volume two in particular was an invaluable guide, with short company descriptions and some basic financials – not that investors were remotely bothered by company fundamentals in a one-way market that had not at that point seen a single default by an offshore issuer. For issuers, the economics were too good to pass up: by adding equity optionality they could save hundreds of basis points on coupons versus Eurodollar straights.

As the bubble expanded, so did issue sizes. By 1989, a veritable Who’s Who of corporate Japan – Nissan, Toyota, Japan Airlines, Toshiba, Canon, Nippon Steel, Kobe Steel, Matsushita, Sumitomo Corp, Asahi Breweries, Mitsubishi Corp, Mitsui & Co, Mitsubishi Heavy Industries, C Itoh and others – were selling US$1bn-plus issues. Through the combination of yen cashflows from option exercise as warrants sailed through strike prices and a very favourable basis swap (yen interest rates were some five percentage points lower than US interest rates), issuers could effectively receive free or even negative-cost funding.

The bond with warrants phenomenon created a huge and ultra-profitable market for underwriters, traders and market-makers that developed a culture all its own. The Japanese Big Four controlled 85%–90% of all Eurobond-with-warrants and Euroconvertible underwriting, led by Nomura (at the time easily the biggest investment bank in the world by market cap). The fact that most warrant buyers were Japanese investors and that issuers swapped the predominantly US dollar-denominated stubs (the ex-bonds) into floating-rate yen gave the Japanese firms a stranglehold on the market.

Beyond the leading underwriters, the market attracted a huge entourage of non-Japanese market-makers and proprietary traders made up of most of the leading US, UK and European investment banks and brokers as well as specialist warrant-trading firms such as the legendary Cresvale (whose founders Steve Burnham and Malcolm Stevenson made huge personal fortunes as the market went inexorably higher).

Masaaki Goto, chairman of Daiwa Capital Markets Europe, arrived for his first tour of duty in London in 1987, five years after joining the firm in Tokyo, to work on bonds-with-warrants and convertible new issues.

“Eurobonds with warrants became a cheaper alternative to domestic funding; by 1985, everyone had rushed into the market and there were three to four deals a week, sometimes more,” he recalled. “Everyone thought the Nikkei would carry on going up.” Indeed, while the Nikkei did suffer during the global stock market crash of 1987, its decline was muted and prices had regained previous levels within five months.

“Warrant trading was very profitable,” Goto continued. “But warrants became purely speculative tools and they were unsophisticated insofar as few people used models to correctly price option value. In that respect, pricing was inefficient and issues were almost all under-priced, so would invariably pop on launch; the offered side very quickly became the bid side and participants were effectively guaranteed a profit. The Big Four Japanese securities houses were big underwriters and market-makers but the huge liquidity in the market attracted a large number of players.”

The market also attracted some colourful characters and acquired a racy, somewhat spivvy character. Prop traders and speculators would engage in any number of option strategies using cheap warrants: synthetic convertibles (warrant baskets plus government bonds); cash extraction (short stock, long warrant baskets); volatility trading (long warrant baskets, short Nikkei futures) and a host of others.

The infamous Terry Ramsden made his fortune trading Japanese warrants. A brash, cocky trader from the mid-1970s, Ramsden amassed a huge fortune during the 1980s, estimated at above £100m, through Japanese warrant trading. He ostentatiously flaunted his wealth, lived a playboy lifestyle, had his own plane, houses and supercars around the world, as well as a string of racehorses. He would bet fortunes on horses, including a fabled £1m on a single race.

He used his huge stockpile of warrants to command big stakes in specific companies, causing huge upset in the conservative Japanese financial community in 1985 by launching (unsuccessfully) a hostile takeover of ball-bearing and electronics parts manufacturer Minebea Co, a regular issuer of bonds with warrants, through his warrant stockpile.

In the end, he went bankrupt and was then jailed for attempting to conceal funds from the court.

The stock market and real estate bubbles ultimately proved unsustainable and the inevitable happened: from its 1989 high the Nikkei entered a 10-year decline to a low of just over 7,000 in March 2009, equivalent to a fall of 82%. Even by late August 2013, the index was trading below 13,500.

Opportunity through adversity

It is worth remembering that the country’s current megabanks are partly the result of multiple government-engineered distressed bank mergers. But the story of the Japanese banks in the post-bubble period is not just one of struggle and retrenchment. While the stock market and real estate crash brought in Japan’s long-run period of economic decay and deflation that has lasted to this day, the huge profits from equity-linked activities had also given the Japanese firms the confidence and the financial wherewithal to build out their activities in the straight bond market.

One hugely important dynamic around this was the rise of the yen as a funding currency for global issuers, predominantly sovereigns and supranationals.

“SSA issuance in yen was around 2% of the total in 1980. By 1995, that had risen to 29%. The yen market became a very deep source of funding,” said Vince Purton, head of debt capital markets at Daiwa Capital Markets Europe and a 30-year veteran of the firm he joined after leaving university.

The yen market was split into a variety of segments: as well as Euroyen and later yen Globals in the offshore market, the domestic market had Samurais (yen foreign bonds), Shoguns and Geishas (non-yen foreign bonds) as well as the Daimyos (yen bonds with European settlement). Uridashis came later.

For sovereigns, the Japanese buyer base was perfect. For a start, they were extremely risk-averse. When they bought international credits, they really only focused on sovereigns. They would move down the sovereign credit curve but would not veer into corporates or FIG. The arbitrage from yen to dollars was very competitive and the basis cost was negligible. And a lot of sovereigns had a natural desire to hold yen in their reserves so a lot of supply wasn’t even swapped. It was a match made in heaven.

In 1987, Daiwa had 400 people in London. “That doubled in the 1990s,” Purton recalled. “And from 1993, we developed global ambitions and wanted to become a serious player in other currencies,” he said. Japanese firms expanded their global footprint, while taking full advantage of the ongoing Japanese bid, to develop multi-currency capabilities and penetrate a much broader network of issuing clients.

The Japanese firms built out sales capabilities and established localised trading platforms in EMEA and the US. “In 1983, 90% of our staff in London was Japanese and 10% non-Japanese; by the 1990s, it was the other way around,” Purton said. The change exemplified the shift in aspiration at that time.

MUSI’s Morganti takes up the story. “At that time, business was profitable and the Japanese brokerages used that revenue to invest in good people, and we were able to push very aggressively to develop positions in sovereign markets. Before the euro was introduced, every sovereign in Europe was basically funding in a multitude of currencies so we developed a good public-sector business. It worked because at the time we were operating across all the legacy European currencies in addition to the US dollar and yen and we had good distribution platforms in Europe. We grew a very substantial presence in yen and non-yen sovereign markets in the early to mid-1990s,” he said.

One stand-out deal was the huge ¥550bn three-tranche transaction that Nomura, Daiwa and Nikko underwrote for Italy in June 1995 – at the time the largest Eurobond ever – and after Italy had already taken out ¥750bn in two issues in 1994.

“I remember being at the IMF meetings. The DCM guys from the global bulge-bracket came up to me moaning: ‘You’re doing a US$2bn deal to pump into your retail network; you’ve just killed the global mandate we were expecting to get this year from Italy’. It was hilarious,” Morganti said.

Fast-forward to today and the market finds the Japanese Big Five at an interesting point. Broadly speaking, they had an OK financial crisis. The megabanks have been net buyers during the deleveraging wave that started in 2009 and are now attempting to monetise their massive balance sheets and pushing cross-sell into their capital markets capabilities more aggressively. Nomura and Daiwa, the stand-alone investment banks without balance-sheet might, are finding the environment more challenging. Do they have aspirations to relive former glories? Probably not. But glories they were.

To see the digital version of this report, please <a href="http://edition.pagesuite-professional.co.uk/Launch.aspx?EID=b2eb69c3-7774-4d35-a0ff-c70b03f7288f" onclick="window.open(this.href);return false;" onkeypress="window.open(this.href);return false;">click here</a>.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

| Eurobond market (straights and equity-linked) 1986 | ||||

|---|---|---|---|---|

| Bookrunner | No of issues | Total (US$m) | Share % | |

| 1 | Credit Suisse | 100 | 19,705 | 11 |

| 2 | Deutsche Bank | 117 | 16,853 | 9.4 |

| 3 | Nomura Securities | 129 | 14,848 | 8.3 |

| 4 | JP Morgan | 92 | 12,470 | 6.9 |

| 5 | UBS | 102 | 10,758 | 6 |

| 6 | Citigroup | 67 | 9,633 | 5.4 |

| 7 | Morgan Stanley | 72 | 8,954 | 5 |

| 8 | Daiwa Securities | 83 | 8,865 | 4.9 |

| 9 | BNP Paribas | 86 | 8,493 | 4.7 |

| 10 | BofA Merrill Lynch | 47 | 6,120 | 3.4 |

| Market total | 1,406 | 179,565 | ||

| Source: Thomson Reuters | ||||

| Eurobond market (straights and equity-linked) 1989 | ||||

|---|---|---|---|---|

| Bookrunner | No of issues | Total (US$m) | Share % | |

| 1 | Nomura Securities | 153 | 32,951 | 15.7 |

| 2 | Nikko Securities | 78 | 17,471 | 8.3 |

| 3 | Daiwa Securities | 95 | 16,898 | 8.1 |

| 4 | Yamaichi Securities | 73 | 15,788 | 7.5 |

| 5 | Deutsche Bank | 124 | 15,372 | 7.3 |

| 6 | UBS | 65 | 8,869 | 4.2 |

| 7 | Credit Suisse | 47 | 8,481 | 4 |

| 8 | JP Morgan | 46 | 8,233 | 3.9 |

| 9 | BNP Paribas | 55 | 7,951 | 3.8 |

| 10 | BofA Merrill Lynch | 49 | 7,561 | 3.6 |

| Market total | 1,488 | 210,014 | ||

| Source: Thomson Reuters | ||||

| Eurobond market (straights and equity-linked) 1990 | ||||

|---|---|---|---|---|

| Bookrunner | No of issues | Total (US$m) | Share % | |

| 1 | Nomura Securities | 94 | 16,219 | 9.9 |

| 2 | UBS | 54 | 12,408 | 7.6 |

| 3 | Deutsche Bank | 83 | 11,540 | 7.1 |

| 4 | Nikko Securities | 63 | 9,769 | 6 |

| 5 | Credit Suisse | 47 | 9,332 | 5.7 |

| 6 | Daiwa Securities | 71 | 9,158 | 5.6 |

| 7 | BNP Paribas | 41 | 8,324 | 5.1 |

| 8 | JP Morgan | 33 | 7,103 | 4.4 |

| 9 | Mizuho (IBJ Intl) | 79 | 7,054 | 4.3 |

| 10 | HSBC Holdings | 40 | 7,029 | 4.3 |

| Market total | 1,092 | 163,347 | ||

| Source: Thomson Reuters | ||||

| Eurobond market (straights and equity-linked) 1987 | ||||

|---|---|---|---|---|

| Bookrunner | No of issues | Total (US$m) | Share % | |

| 1 | Nomura Securities | 123 | 18,065 | 13.1 |

| 2 | Credit Suisse | 81 | 10,545 | 7.6 |

| 3 | Deutsche Bank | 89 | 9,641 | 7 |

| 4 | UBS | 92 | 9,604 | 6.9 |

| 5 | Nikko Securities | 77 | 9,045 | 6.5 |

| 6 | Yamaichi Securities | 70 | 7,266 | 5.3 |

| 7 | Daiwa Securities | 70 | 6,940 | 5 |

| 8 | Citigroup | 57 | 6,167 | 4.5 |

| 9 | JP Morgan | 54 | 5,816 | 4.2 |

| 10 | Commerzbank | 53 | 5,815 | 4.2 |

| Market total | 1,316 | 138,358 | ||

| Source: Thomson Reuters | ||||

| Eurobond market (straights and equity-linked) 1991 | ||||

|---|---|---|---|---|

| Bookrunner | No of issues | Total (US$m) | Share % | |

| 1 | UBS | 94 | 21,703 | 9.4 |

| 2 | Nomura Securities | 115 | 21,030 | 9.1 |

| 3 | Daiwa Securities | 106 | 17,002 | 7.3 |

| 4 | Deutsche Bank | 99 | 16,776 | 7.2 |

| 5 | Credit Suisse | 58 | 14,376 | 6.2 |

| 6 | BNP Paribas | 44 | 14,219 | 6.1 |

| 7 | Nikko Securities | 91 | 11,957 | 5.2 |

| 8 | Goldman Sachs | 54 | 11,935 | 5.2 |

| 9 | Yamaichi Securities | 77 | 10,369 | 4.5 |

| 10 | Morgan Stanley | 15 | 9,022 | 3.9 |

| Market total | 1,316 | 231,708 | ||

| Source: Thomson Reuters | ||||

| Eurobond market (straights and equity-linked) 1992 | ||||

|---|---|---|---|---|

| Bookrunner | No of issues | Total (US$m) | Share % | |

| 1 | UBS | 122 | 25,463 | 10.3 |

| 2 | Deutsche Bank | 89 | 22,480 | 9.1 |

| 3 | BNP Paribas | 70 | 16,743 | 6.8 |

| 4 | Nomura Securities | 80 | 16,338 | 6.6 |

| 5 | Credit Suisse | 68 | 16,173 | 6.6 |

| 6 | JP Morgan | 57 | 12,476 | 5.1 |

| 7 | Goldman Sachs | 48 | 10,932 | 4.4 |

| 8 | Commerzbank | 40 | 9,917 | 4 |

| 9 | Daiwa Securities | 68 | 9,916 | 4 |

| 10 | Nikko Securities | 63 | 9,025 | 3.7 |

| Market total | 1,319 | 246,428 | ||

| Source: Thomson Reuters | ||||

| Eurobond market (straights and equity-linked) 1988 | ||||

|---|---|---|---|---|

| Bookrunner | No of issues | Total (US$m) | Share % | |

| 1 | Nomura Securities | 131 | 18,186 | 10.6 |

| 2 | Deutsche Bank | 130 | 16,651 | 9.7 |

| 3 | Credit Suisse | 81 | 14,130 | 8.3 |

| 4 | UBS | 93 | 12,942 | 7.6 |

| 5 | Daiwa Securities | 73 | 9,675 | 5.7 |

| 6 | JP Morgan | 43 | 8,687 | 5.1 |

| 7 | Commerzbank | 62 | 7,900 | 4.6 |

| 8 | Nikko Securities | 67 | 7,747 | 4.5 |

| 9 | Mizuho (IBJ Intl) | 80 | 7,565 | 4.4 |

| 10 | Yamaichi Securities | 63 | 6,965 | 4.1 |

| Market total | 1,451 | 171,151 | ||

| Source: Thomson Reuters | ||||

| Bonds with warrants – the US$1bn club | |||

|---|---|---|---|

| Date | Amount (US$m) | Issuer | Bookrunner |

| 01/03/90 | 1,000 | Matsushita Electric Industrial | Nomura |

| 28/11/89 | 1,000 | Sumitomo Realty & Development | Daiwa |

| 26/10/89 | 1,200 | Toshiba Corp | Nomura |

| 02/10/89 | 1,500 | Nissan Motor | Yamaichi |

| 11/08/89 | 1,000 | Asahi Breweries | Nomura |

| 12/06/89 | 1,500 | Sumitomo Corp | Daiwa |

| 30/05/89 | 1,000 | C Itoh | Yamaichi |

| 30/05/89 | 1,000 | C Itoh | Nikko |

| 25/05/89 | 1,500 | Mitsubishi Heavy Industries | Nikko |

| 22/05/89 | 1,500 | Toyota Motor Corp | Nomura |

| 18/05/89 | 1,000 | Nippondenso | Nomura |

| 24/04/89 | 1,500 | Mitsubishi Corp | Nikko |

| 30/03/89 | 1,000 | Japan Airlines | Nomura |

| 26/01/89 | 1,200 | Nippon Steel Corp | Nikko |

| 26/01/89 | 1,000 | Kobe Steel | Nomura |

| 26/01/89 | 1,000 | Kobe Steel | Yamaichi |

| 23/01/89 | 1,000 | Canon | Nomura |

| 23/01/89 | 1,000 | Canon | Yamaichi |

| 18/01/89 | 1,000 | Mitsui & Co | Nomura |

| Source: Thomson Reuters | |||