In the immediate aftermath of the March 11 earthquake, many outside Japan thought the country’s capital markets had been decimated. But foreign issuers were positively surprised to see investor attention quickly refocus on the superior-yielding Samurai market. Global FIGs stormed the yen market as an alternative funding ground, proving the doubters wrong. Atanas Dinov reports.

To view the digital version of this report, please click here.

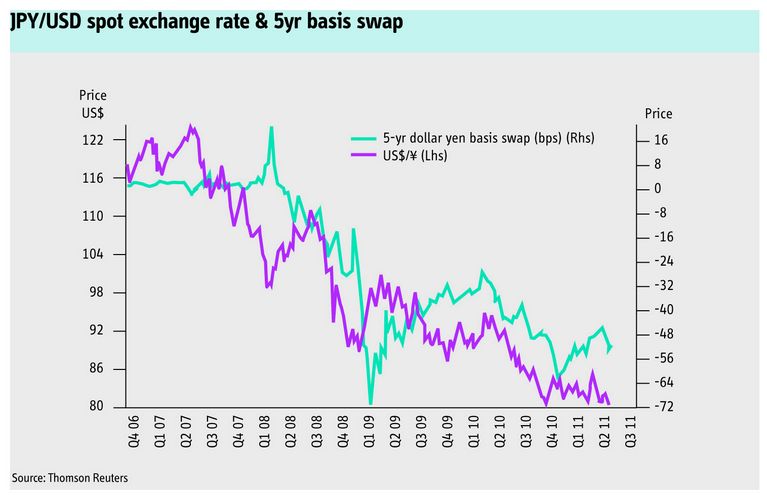

The devastating March 11 earthquake in Japan – the country’s strongest on record – shook the yen capital markets to the core. As a result, the yen credit market closed about 10 trading days earlier than the usual fiscal year-end finish in April. Corporate spreads took the biggest hit. Yen-denominated international paper generally also widened, although not so dramatically, with investors understanding underlying credit quality had not been damaged.

Now, many expect Samurai issuance volume to enjoy one of its strongest ever years. The summer has traditionally been the busiest Samurai issuance window, and this year Samurai bond issuance volume to the first week of June stood at ¥1.19trn (US$14.8bn), from 36 tranches. That included ¥281.5bn of Japan Bank for International Cooperation-guaranteed emerging market deals. In 2010 during the same period, the market saw issuance of ¥530.9bn, including ¥100bn of JBIC-backed Samurai bonds.

Most near-term issuance will come from global FIGs, especially European banks which are keen to diversify wholesale funding, the EU’s criticism of their over-reliance on the US dollar market still ringing in their ears. European banks have only recently entered the yen market, traditionally a happy hunting ground for US banks – at least until the collapse of Lehman Brothers in 2008.

A lack of domestic supply has been a positive for foreign credits, which have proved investors’ main opportunity to pick-up yield. Many have recovered the post-earthquake widening. Some of the top quality names have moved even tighter.

“A lot of people lost focus on the yen market after the earthquake but after HSBC and SBAB, the focus is back,” said one syndicate banker at foreign houses. “We are receiving a lot of questions now for updated prices.”

Sound funding alternative

The public yen market was reopened with HSBC’s ¥143.4bn five-year dual-trancher in the middle of May, the largest non-guaranteed deal since Lehman’s demise. SBAB Bank had started marketing on March 10 but had been forced to postpone. It printed a ¥75bn three-part trade the week after HSBC’s deal, pricing through the borrower’s pre-earthquake price guidance and attracting attention from a wide range of issuers.

“The Samurai market is on fire. The rolling success of the latest deal from CBA on top of the other recent deals just shows the strength of the market,” said Kazuhide Tanaka, head of long-term funding, Japan, at Rabobank.

In the first week of June, CBA demonstrated the unusual, improved circumstances in the yen market, in a rare case of arbitrage funding. The ¥101bn Samurai deal was only CBA’s third offshore benchmark deal for its fiscal year. Some estimated the saving to be at least 5bp, while others put the number in excess of 10bp. The secondary levels on CBA’s US dollar paper equated to around the mid-40s over yen offer-side swaps.

“We like the diversification of the Samurai market for wholesale funding,” said Simon Maidment, head of group funding and execution at CBA. “Out of our home market, we have only done one US dollar and euro benchmark this fiscal year, ending in June. The Samurai deal is our third offshore benchmark.”

CBA was, he said, very happy with the result of the trade. “While the pricing is more expensive for us than our most recent US dollar transaction we wanted to return to the Samurai market and are satisfied that the Samurai market has remained relatively stable in light of the offshore market’s volatility during marketing week [in the first week of June].”

However, while the US dollar paper was cheaper, the US$3bn CBA trade done in March – which contained a US$700m five-year fixed-rate tranche with a coupon of 3.25% yielding 188bp over US Treasuries – priced in a more stable market environment. The turn of the markets and Moody’s downgrade subsequently translated in widening of the dollar spreads by around 7bp-10bp for Aussie banks. Yen funding, by contrast, stayed relatively stable.

“We look at secondary levels in other markets, of course, but a big part of the Samurai marketing strategy is built on relative pricing versus similar Samurai credits in yen,” said Shun Nakamura, syndicate manager at Daiwa Capital Markets. “While we have our reference points from US dollar and other core markets’ trading levels, a big extent of the price formation comes from the relative pricing in yen compared to other recent foreign borrowers.”

“What we paid is justifiable when you consider the overall decline in yields since earlier this year,” added Rabo’s Tanaka. “In the space of four months Rabobank was able to return and we have done over ¥150bn of long-term funding. That we can come back after just four months and essentially get a bigger deal done shows the excellent shape for international yen deals, due to a very receptive investor base and lack of competition from domestic supply.”

In the immediate aftermath of the devastating earthquake, Japanese investors were – and still are – uncertain about the future of Tokyo Electric Power Company. That is a significant concern for a company that has more than US$61bn of bonds, roughly 8.5% of all outstanding domestic credits.

The wildfire started from Tepco, with total liability at around ¥9trn, and quickly spread across to the other electric power utilities and corporates, the latter’s spreads taking the biggest hit. As the Tepco saga unfolded, the ¥13trn utilities bond market froze. Local accounts therefore realigned their investment strategies in March and early April in favour of the quasi-sovereign municipalities and the Zaito agencies. However, the supply from the high-grade sector was insufficient to absorb the mountain of cash left over from the corporate space. April saw only about half of its usual primary issuance volume.

The primary market reopened for the new financial year in the second week of April. The absence of the utilities meant a rush to buy whatever high-quality names were out there, be they highly rated Samurais or top-quality domestic corporates.

“The definition of a high-grade corporate in Japan used to be the electric power utilities, JR and NTT,” said one syndicate head involved in NTT’s deal printed at the end of May. “The utilities are not accessing the market now, while JR-East is obviously affected by the earthquake, so what was left was NTT. So it was pretty much the right deal size at ¥100bn, but it’s still not enough. Investors are hungry, very hungry and they are moving to Samurais.”

Pipeline dream

FIGs had already drummed up ¥751bn of funding by early June, about 59% of all the FIG Samurai volume for 2010, according to Thomson Reuters.

And the pipeline is strong. Inaugural transactions are being envisaged by French banks. Societe Generale and Banque Federative du Credit Mutuel are eyeing the market while there are also rumours of a debut deal from Credit Agricole.

From the UK, Lloyds TSB is preparing a mid-June pricing while Barclays has been heard to have soft-sounded on a few occasions, adding some weight to speculations for at least one deal within 2011. RBS, on the other hand, has opted for a September wholesale benchmark issuance, meanwhile focusing on a mid-June cheaper plain vanilla funding through a retail Euroyen (Uridashi).

UBS is another potential candidate, having also been heard more than once to have softly approached investors. National Australia Bank and Westpac, which postponed deals due to the earthquake, are expected to return, on the heels of CBA’s success. Some Korean issuance should also transpire, especially from quasi-sovereigns such as Export-Import Bank of Korea and Korea Gas.

US FIGs are also expected to return to their old stomping ground once their quarterly results are translated towards late June or early July. JP Morgan reopened the market for US FIGs in February, printing a ¥111.1bn five-year deal, which could pave the way for others to follow. Rumours abound that Citigroup will return with ¥186.5bn Samurai redemptions in fiscal year 2011, while Bank of America (¥123bn redemption) is gearing for late June funding across three- and five-year maturities.