The central banks were once Olympian gods but have descended to be among men, and in doing so have lost many of their powers.

There was a time, not all that many years ago, when central banks seemingly controlled the world. I’m not talking the eras of Ben Bernanke or even Alan Greenspan, but of the 1980s when Paul Volcker ruled the Federal Reserve, Karl Otto Pohl was master of the Bundesbank, Fritz Leutwyler was at the Swiss National Bank and Robin Leigh-Pemberton was governor of the Bank of England.

These four men, in concert, sat on top of the world. Truth be told, it was easier then. Hedge funds were few and far between, while leverage, in much of the world at least, was still known as gearing and was a means to an end rather than an end in itself. So when the monetary authorities spoke, the banking system not only listened but quivered.

Concerted central bank action, as it was known, was a side-effect of the 1973 oil shock and the subsequent period of rampant inflation and extreme currency volatility accompanied by deep recession. It also came in the aftermath of the highly inflationary Vietnam War and the Watergate scandal.

So with belief in the ability and integrity of Washington at a low it was time for the men in grey to take over. Hence, under the guidance of Volcker, the monetary authorities pushed aside the politicians and became controlling powerhouses.

Volcker decided that inflation had to be wrestled to the ground at all costs and under him, with the help of his counterparts in Europe, the interest rate screw was ruthlessly turned. If imposing double-digit interest rates was what it took to slay the beast, double-digit interest rates it would be.

To cut a long story short, inflation was brought under control, the central bankers became the all-powerful knights in shining armour and there began the long and fruitful – for fixed-income markets at least – interest rate super-cycle, the end of which we appear to be experiencing right now.

Admired

In time, Volcker stepped down and handed the keys of the Fed to Greenspan, who played the part, with great aplomb, of the man who had all the answers. He went on to become Time magazine’s Man of the Year and rose to become the most admired and quite possibly the most powerful man in America.

The Fed was not alone. The Bundesbank, under the guidance of a variety of tight-lipped presidents who followed Pohl, picked up the fiscal mess left by Chancellor Helmut Kohl’s headlong dive into reunification with a destructive one-for-one exchange rate between the mighty Deutsche Mark and the Monopoly money-like currency of the GDR (the Ost Mark). While Kohl show-boated, the Buba set out to mop up the mess.

In summary, the impression was created – and the myth born – that central banks don’t just steer and fine-tune underlying trends in the economy but that they actually determine them. Who, for instance, can forget “Mr Yen”, the mercurial Eisuke Sakakibara, who could move the currency at the raising of an eyebrow?

Centre stage

Fast forward to September 2001 (skipping past the ERM crisis of 1992 when the Bank of England was humiliated by the foolishness of Britain’s politicians). Two passenger jets crash into the twin towers of the World Trade Center in New York, one into the Pentagon in Washington and a fourth one ploughed into the ground en route to what is subsequently assumed to be the nation’s capital.

The politicians are once again clueless but Greenspan steps out, centre stage, and takes control. The US economy had been moving into an otherwise healthy cyclical downturn when 9/11 hit. Greenspan seems to have concluded that the country could deal with a recession and it could deal with the attacks, but it could not deal with both.

He can’t make the latter go away but he can postpone the former and that he does by way of aggressively accommodative monetary policy. In doing so he unwittingly laid the foundations for the global financial crisis which overtook us all six years of rampant consumption later.

The emergence of China as a low cost-producer of anything and everything with a near insatiable desire to catch up on over half a century of ideologically imposed economic stagnation (via the boundless availability of cheap credit in the US) produced a toxic stew of imported disinflation mixed with a central bank remit constructed around the holy cow of a low inflation target. The West found itself with what Bank of England governor Mervyn King described as the “NICE” economy – non-inflationary, consistent expansion.

Too clever by half

So the self-satisfied arrogance of the post-war political class, which thought itself to have eaten with impunity of the fruit of the tree of knowledge and thus rode blindly and cluelessly into 1973, was now followed by central bankers doing very much the same in 2008.

It is hard to believe now, but Greenspan and his cohorts truly were convinced that the low inflation environment that accompanied the consumption boom of the post-9/11 era was the result of their own incredibly clever monetary policy.

When the balloon went up and the bubble began to burst in November 2007, they knew not what had hit them. They were, however, incredibly lucky. The banks had made out like bandits – actually they had made out many, many times better than bandits – during the free ride provided by the Fed and its chums between September 2001 and September 2008 when Lehman Brothers collapsed and, thus, in the eyes of the general public, the villains had been identified.

Not surprisingly, the monetary authorities never saw the need to face up to – or even admit – their role in first creating the bubble and then doing absolutely nothing to stop it getting dangerously big.

Fallible after all

And yet, for reasons that remain a mystery, markets, politicians and citizens alike continued to worship at the altar of those mighty and infallible central bankers.

So it came to pass that instead of acknowledging the flawed developments that led to the cataclysmic near-collapse of the financial system in 2008 and that should have spelled the end of the entire borrow-to-consume economic growth model, the monetary authorities assiduously looked the other way.

As we now know and are slowly beginning to acknowledge more widely, the central banking system could come up with nothing smarter than to replace the bubble created by easy and irresponsible bank lending with one of its own: “quantitative easing”, which if translated into plain speak means nothing other than pushing yield curves lower by flooding the world with a near-endless supply of officially sanctioned unsecured credit.

If ever there has been a textbook case of taking a course of action that has treated the symptoms and not the causes, QE has been it. So far, it has neither created sustainable growth nor has it helped to fire up inflation.

Instead of acknowledging the flawed developments that led to the cataclysmic near-collapse of the financial system in 2008 and that should have spelled the end of the entire borrow-to-consume economic growth model, the monetary authorities assiduously looked the other way

False underpinnings?

Much of the economic theory that underpins modern monetary policy was developed during the second half of the 20th century and in the aftermath of Bretton Woods, from where it has been carried forward into the 21st century with, to-date, no significant fundamental adjustments or upgrades.

The fact that apparent axioms from Chicago School monetarism to the Black-Scholes model formed the foundations upon which the global crisis was built has as yet not been questioned. Why should it if all evils can be palmed off on bankers?

Since September 2001, our leaders, both political and financial, have set new records in taking the paths of least resistance. If growth doesn’t happen, slash rates, then sit back and wait for the people to consume the economy out its torpor on money they don’t have and, in the absence of inflation to erode their debt away again, no way of ever paying it back.

The hubris of unquestioned power also led to the invention, if that is what you want to call it, of one of the greatest nonsenses of modern times: forward guidance.

Forward guidance, so much beloved by the current governor of the Bank of England, Mark Carney, assumes that policymakers are smarter than the rest of the world’s economists and bankers and that they know something nobody else does, or at least that they have interpretational insight that is superior to that of others.

In fact, forward guidance has proved to be not only meaningless but has gone a long way to destroying the mystique that central banks once had.

Shilly-shallying

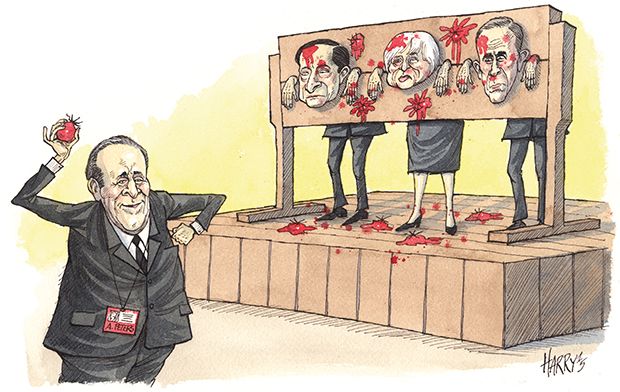

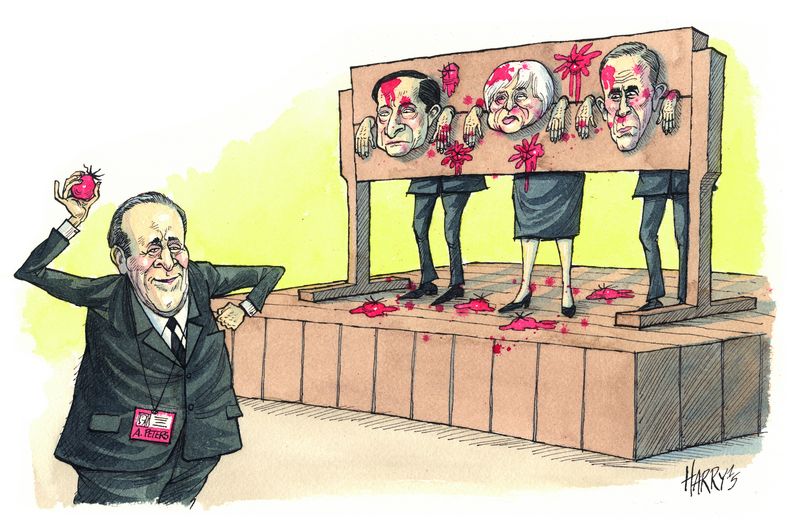

Meanwhile, the position of the monetary authorities has not been improved by the near endless shilly-shallying by the Federal Reserve Board under the leadership of Janet Yellen.

Not only did she fail to map a clear and understandable “decision tree” when it came to rate rises but she also failed to rein in her fellow FOMC members as they have spent the year competing for column inches by contradicting each other at every turn.

Yellen’s insistence on making monetary policy data-dependent has, by definition, placed the Fed behind the curve and thus, also by definition, it has all-but destroyed the institution’s most valuable asset, namely its credibility. The Fed now finds itself being tossed around on the stormy seas – in the same way as the rest of the financial system – rather than acting as the towering lighthouse that it once did.

The ECB has its own issues as it has gradually discarded its “Son of Bundesbank” disguise and now also looks like a house full of solutions in search of matching problems. Having been undermined by the politicians over Greece, it seems to have given up being the tough guy and, like the Fed, has begun playing to the gallery.

As for the Bank of Japan, it has proven to be, despite Abenomics and its broken arrows, a one-trick pony, while the People’s Bank of China has to be seen as the PRC government’s glove-puppet.

Gods no longer

The central banks, in other words, were once Olympian gods but have descended to be among men, and in doing so have lost many of their powers.

Above all, it was misguided monetary policy at the beginning of the last decade that led to the unfettered inflation of the credit bubble. And having dodged the bullet of contributory negligence, the central banks took it upon themselves to provide the solution. Now, they find themselves standing without Warren Buffett’s famous shorts.

The rule that it takes years to build a reputation and days to lose it applies to them as much as it does to the rest of us.

To see the digital version of the IFR Review of the Year, please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com .