To view the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

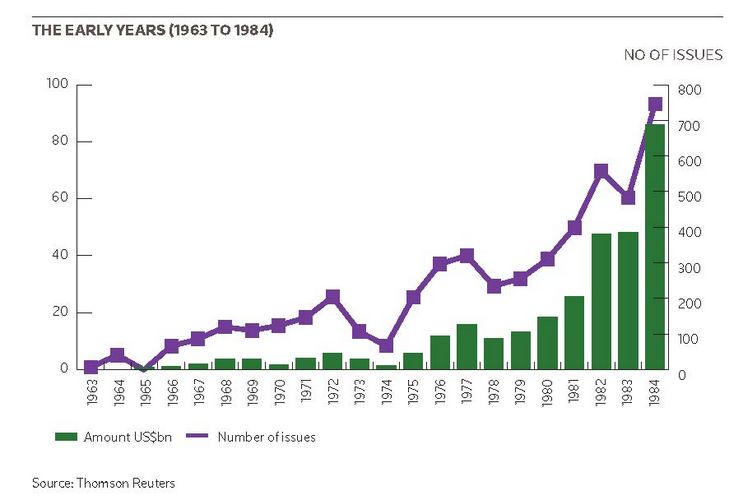

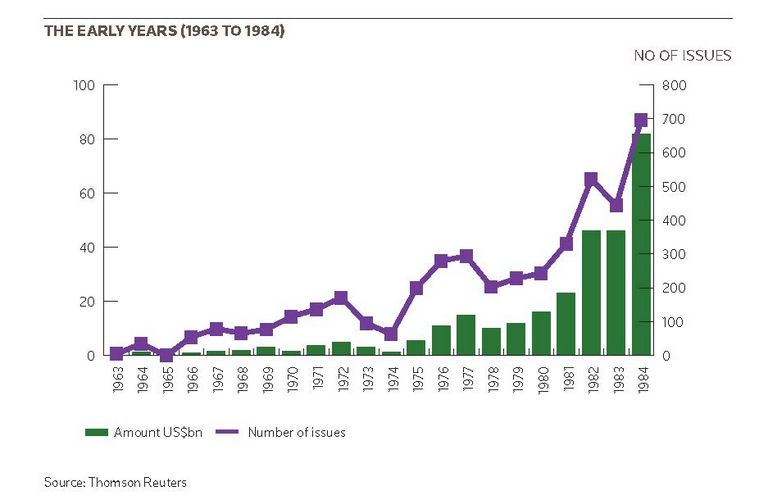

IFR: Gentlemen: thank you for attending IFR’s Eurobond market retrospective, coinciding with the publication of the 2,000th issue. IFR was launched in 1974. Looking back, it was a momentous year that saw a host of dramatic political and economic events. But what do you recall of your early careers and the environments you found yourselves in?

Rene Karsenti: In 1974, I had just started my career in Paris at Caisse des Depots in financial management and went on to join the treasury of the World Bank in 1979 when Gene Rotberg was treasurer. It was a completely different world; the financial markets were fragmented because of national barriers and borders. When I started in Paris, the French market was very much a regional market.

What was striking during my early years at the World Bank was the markets were highly regulated so we had to seek authorisation and approval every time we wanted to borrow from the regulators and central banks of the country whose currency we were borrowing in. What was also very striking was from a technology point of view was that we were in the infancy of what we have now; the time it took to put together even a standard transaction was incredible: producing and proof-reading prospectuses, drawing up documentation, getting everything checked and so on. It was a time of antiquity.

A transaction of US$50m or US$100m would take several weeks to be completed. Looking back at the progress we’ve made in technology and what we are able to do now with global issues of billions it’s an amazing achievement. But my early recollections were of fragmentation in terms of markets, currencies, investors and technology.

Gene Rotberg: The major events that I remember in the early 1970s were really non-events. That is governments were doing their best and were succeeding in blocking capital flows between countries. You weren’t allowed to take funds out of the UK for many years, for example. Similarly, the French had blocked their market to all foreign borrowers and most countries were trying to restrict savings to be used only in their own country. The US severely restricted the World Bank from borrowing dollars inside the United States.

It was a period in which finance ministries and central banks tried to block both the flow of savings from their own country to finance anything outside their own country, either private or government, and secondly to block currency speculation so that they and they alone would have control over the value of their currency. Because of that, they didn’t want to see their currencies out of their control. ie issued outside the host country. That was the environment in the late 1960s and early 1970s.

IFR: With all the talk of de-globalisation, we seem to be heading back in that direction, certainly in terms of public policy

announcements from certain governments.

Cyrus Ardalan: In my first four or five years, when I was at the World Bank working as an economist on the assets side, what was quite remarkable was that developing countries had zero access to the international capital markets. It didn’t exist at that time; if you were a poor country, the only way you could borrow money was through the development agencies, hence the importance of the World Bank and its significance.

Even middle-income countries had very limited access, and what access they had was through the syndicated loan market, and even that was on a very patchy basis. I remember conducting research for the board of the World Bank on Yugoslavia and its access to the international markets at that time, which was exclusively focused on syndicated loans from a group of very second-tier institutions.

On the treasury side, picking up on Rene’s comment, it was really quite interesting for me. I think the big contrast between then and today is that it was an incredibly inefficient and illiquid market at that time. You had very limited visibility and transparency in pricing; and prices tended to move very, very slowly and sporadically.

We had no computers so there was no way of making price comparisons. I remember, for example, running the swap business with the World Bank. We used to update our pricing sheets once a week, once a week as opposed to every five seconds. Swaps were not traded and the market was based on matching counterparties with opposite positions.

IFR: That sounds like bliss …

Cyrus Ardalan: Things just didn’t move; it was not an efficient transparent market. It was a completely different world, and as Rene said things were very slow. You had to go through a whole process of due diligence and it took weeks before you did a transaction and transaction sizes tended to be quite small. But it was also a period of incredible innovation and creativity. You had on one side a very traditional and simple market; on the other side the seeds of enormous change which were already beginning to emerge.

Gene Rotberg: Following up what Cyrus just said, because developing countries were blocked from accessing capital markets, they had no choice but to borrow from commercial banks. Therefore, you had a huge concentration of borrowing by Argentina, Brazil, Mexico, and much of South-East Asia from the commercial banks.

They clearly saturated their portfolios with very little attention paid to creditworthiness. That directly led to the LDC debt crisis of the 1970s, because all of the borrowings took place through the commercial syndicated loan market rather than through capital markets where the risk would have been spread across the world in thousands of institutions.

Iain Baillie: Picking up on two of the points that Cyrus made: volatility was so low back in the 1970s that we would make firm, overnight offerings to institutions in Asia. They’d be sent by telegram and the responses would return the following day by telegram or telex; telex at that point was positively high-tech.

The investing side of the Eurobond market at that point was very much dominated by Swiss institutions. But you couldn’t just pick up the phone and dial Switzerland; you had to have fixed time calls. We would have a call at 10:30am, say, with the same institution every morning, If they had some orders we’d get them, and if they didn’t we wouldn’t. It was a very different world from a technology point of view from where we’ve ended up.

Robert Gray: I would endorse comments made about the primitive state of the derivatives market in the 1970s. Although I started life as an oil and gas banker, I had joined Morgan’s International Financial Management Group in New York by the late 1970’s. This really was the laboratory at Morgan for what was happening in Europe, in the build-up to our establishing our own underwriting business in London in 1979 under Morgan Guaranty Ltd.

Part of my time was spent running the bank’s swaps book. It wasn’t a full-time job. We’re talking 1978 now: I literally ran Morgan’s swap business in New York on a part-time basis. US companies loved the opportunity to write cross-currency swaps with us, but at the start we took all the non-US dollar flows though our foreign exchange book. The treasurer of the bank told me: “It’s fine for you to do these swaps, but you must come upstairs and write the individual foreign exchange tickets yourself”. Each foreign exchange inflow and outflow had to have its own ticket, which I had to write out by hand, as part and parcel of being responsible for our swaps business.

Michael Dobbs-Higginson: Well I joined White Weld in 1973, without any experience of banking whatsoever. The only reason I was given the job was because I was the only person in the City who spoke Japanese; the Japanese were just arriving and that was an interesting niche at that time.

I was also reporting to a 23-year-old, who was completely unwashed in every other respect but he was quite smart. I was earning probably a 70th of what I was earning in Japan as an entrepreneur but I’d been chased out of Japan by the CIA, so I had very little alternative but to take this low-paying job in a different environment.

I would say that the first 10 years of my life as an investment banker we were rather like World War I aces, putting on one’s goggles, white scarf around the neck, getting in one’s little Tiger Moth and hand-dropping bombs (aka proposals) on prospective clients. In my case, they were principally in Asia and most of them had never even heard of the Eurobond market, let alone knew whether they wanted to play in it or not.

I had to spend sometimes four or five years persuading the Indian, Taiwanese or Korean governments but my colleague Andrew Korner [now Chief Executive of Asian Capital Partners Group] and I eventually ended up opening seven or eight of the ASEAN countries, plus Korea, to do their first ever Eurobond issues.

Indira Gandhi thought I was crazy. She said: “This is a foreign plot to take over our economy”. I said: “No, madam, it’s not that at all”. Again, those were the days which had a different aspect to today, where it is super high-speed fighter jets that have huge support services behind them with instant reactions. It was a totally different world. It was a fascinating time, and coming from living on a farm in the bush in Africa, I was used to pioneering, so those were the great days.

IFR: We hear a lot today about culture, ethos and ethics. How did those discussions play out back in the day? Historically, for example, people’s backgrounds were academically and socially diverse; the market today is a bit more monolithic. To your point, Michael, the only reason you got the job was because you spoke Japanese, not because of any banking expertise.

But we were making history at the time, and so there was nothing to go on. You couldn’t say: “what do you want to be when you grow up”? “I want to be an investment banker,” because it didn’t exist. Do you think there’s a danger today that we’re creating clones? I think a lot of people that are in quite senior positions in banks nowadays probably wouldn’t ever get employed in the first place now.

Michael Dobbs-Higginson: I certainly wouldn’t have been, that’s for sure …

Robert Gray: I think one of the extraordinary strengths of JP Morgan at that time was the conviction we had that each of us could occupy somebody else’s position within the firm and vice versa. There was an inherent conviction about mobility; whatever your background you could be moved from one desk to another and there was a completely open attitude towards internal movement. I think that contributed to a great degree of mutual respect between employees, the feeling you could be in somebody else’s position tomorrow and they could be in yours.

I think it was a true strength.

Bear in mind that our chairman - Dennis Weatherstone - had started life in London as a clerk and he became chairman of the entire organisation. Those types of positive signals, I think, contributed a great deal to the culture of the firm.

IFR: Iain, you were at Salomon Brothers for quite a long time and of course the firm had its own infamous culture. Could you speak to this whole notion?

Iain Baillie: I think Salomon had a very specific culture. We used to joke that we were rather like Millwall Football Club, no one liked us but we didn’t care. I think the interesting point is it was a very small community in those days and liquidity was provided by traders dealing with each other. In fact, you were expected to make markets to the other dealers, so everybody knew who everybody was.

That meant people found you out very quickly, so there was quite a culture of honour amongst thieves. It’s an interesting point about the evolution of liquidity in the market, because it was the American investment banks that really encouraged the introduction of inter-dealer brokers they were not enthusiastic about the amount of time that dealers all spent dealing with each other - and out drinking with each other, it has to be added.

Michael Dobbs-Higginson: I’d like to second that, because in my days at CSWW/CSFB, looking after the client was actually very important. I think that changed, certainly in my 20 years in investment banking, where the quantum of bonuses grew exponentially, people became much more personally bonus-driven, and this phenomenon got egregiously worse in the 2000s.

I saw that trend and I must say it was a very unattractive trend, because people, especially on the trading and syndicate side, would say, despite having made a commitment to a client: “find a way not to do this deal because we’re going to lose money”, or, “do this deal but do it at a price which will give us a huge profit”. Over time, this resulted in the client’s interests being less and less important.

Robert Gray: I can give a practical example to support what Michael says, which was when I was syndicate manager in the mid-1980s one of the many ill-fated innovations was the perpetual floating-rate note …

Michael Dobbs-Higginson: Which we started …

Robert Gray: …which became the preferred instrument for second-tier subordinated capital for banks. I was instructed in no uncertain terms that I was not to underwrite that instrument because it was not an instrument that was in the long-term interest of our investing clients. It was one of those cases you mentioned, Michael, where a syndicate manager had to take a deep breath.

Michael Dobbs-Higginson: We certainly did them and I must say it’s not something I am particularly proud of on behalf of the firm.

[Note: The US$20bn-plus perpetual FRN market, which started in early 1985, spectacularly crashed in December 1986/January 1987 when the Fed and Bank of England changed the capital value of these instruments - which counted towards bank capital adequacy - and imposed issuance restrictions. The major issuers had been UK, Canadian and Australian banks and the principal buyers were Japanese banks, which had to recognise billions in mark-to-market losses.]

Gene Rotberg: On the issue of competition, a matter that was very prevalent was competition between firms as they approached each issuer. Spreads got extremely tight, and it was clear that underwriters just wanted to grab league table credit because few of these issues could be sold at two, three, or five basis points over Treasuries. Indeed, that was one of the reasons why an institution like the World Bank was rather late in entering the Euromarket because we realised that the bonds would often be held within the underwriting syndicate for a long period of time because they were so tightly priced.

As a result, we were concerned that when they finally opened up and sold those bonds because they had no other choice - they couldn’t hold them because of capital constraints - it would affect our domestic borrowings in Germany, Holland, or in Belgium because of the hidden overhang in those currencies. The expression that I sometimes used was the underwriting firms were delighted to be buried under their own tombstone ads.

IFR: Gene, how would a typical conversation go with a Euromarket underwriter, then? Bearing in mind you had a sense that pricing wasn’t necessary market pricing, would you have rows with your underwriters, would you just agree to differ? How did it work?

Gene Rotberg: What happened is we said: “Look, you’re pricing this too tightly”, which is very strange for an issuer to say, and: “Basically, you’re not going to place these bonds.” The likes of Deutsche Bank would say: “don’t worry about it, we won’t place them in Europe; we’ll place them in our branches throughout Germany.” But sooner or later they were going to leak out.

When underwriters began to come up with more realistic pricing, I felt more comfortable. On the other hand you might say: “Weren’t you worried the bonds would go to a premium, because they would be basically too loosely priced?” We basically told all of our underwriters - and I’m sure other issuers tried to do it, but the World Bank was uniquely situated - “If you come up with a bond issue and a few moments after it’s issued it’s trading at a premium, that means that you priced it badly.

What we will do the next morning, since we had to report to our board of directors which represents 180 countries, we will tell the board of directors, which reports back to their finance ministries, that such and such a firm either was incompetent in their pricing or took advantage of us. That will go through the finance ministries of every country in the world within an hour. You don’t want that to happen.

IFR: So you used blackmail …

Gene Rotberg: Perhaps. But basically at the other end, we tried to make sure that they did not price too aggressively. I think that over time the pricing worked out so that they made some profit and the World Bank got a decent price.

RENE Karsenti: Just to emphasise what Gene said and his attitude towards the underwriters, I think he forced them to adopt a sense of responsibility particularly for the World Bank, as a regular issuer. I recall doing the very first Bulldog issue [ie Sterling foreign bond] for the World Bank; Gene had put me in charge of the transaction.

But I had serious concerns about the pricing; I thought the pricing that was proposed was too generous. Gene’s attitude during the pricing meeting was: “You are responsible for it, but remember the World Bank will continue to issue. If you price it generously, keep in mind that our shareholders as well as our financial partners will know that. You have to be responsible for it.” I wouldn’t say it was blackmail; it more a question of creating some form of partnership, in developing a market between an issuer and an underwriter.

I also wanted to comment on the culture of that time. Going back to earlier days in the 1960s, the Eurobond market had been created by a number of different dealers and they were highly competitive. But they also had a keen sense of the importance of preserving a resilient capital market. Shortly after the Eurobond market was created, there were major difficulties in clearing and settlement. All the market players, who were fierce competitors, came together and put together a self-regulatory organisation to organise that aspect of the cross-border Eurobond market.

That gives you a sense of the culture; someone used the word ‘camaraderie’. I would say it was a culture of responsible people wanting to preserve and to build a resilient market. That was an important aspect of the culture at that time.

Robert Gray: I think it’s worth dwelling on the manifest inadequacies of syndicate practices in this area in the early 1980s. For example, the use of the stabilisation account - you may recall this - there was not much science as to which bonds the lead manager had bought back should be deemed to be stabilisation bonds, and for which the syndicate would be charged accordingly.

Also the whole practice of under-allotting; syndicate members did not know until very late in the day sometimes as to what their allotment was. This created an extraordinary game of bluff between the lead manager, with the implicit threat of a squeeze by under-allotting the syndicate if the thing went extremely badly, which it did on several occasions.

The allotment process was extremely flawed. Then we also had the praecipuum in those days - do you remember? - where we took an eighth off the top for the lead manager. These were all practices that had to be addressed and they were by the IPMA in due course.

Michael Dobbs-Higginson: In contrast to that, if you did a Japanese issue back in the 1970s, you had to get the executive director of the Japanese Ministry of Finance to sign off on the pricing, and he had absolutely no clue as to what the market was. You might get him out of his bathtub at midnight and he would say, “10%” and you’d have to go with that. Those were the days; unlike the World Bank which took a much more sophisticated approach, the Japanese said: “This is Japan, we’ll do it our way”.

IFR: I wanted to pick up on the general theme of regulation. Along with culture, this is a major topic for discussion today. Looking back over the period we’re talking about, I’m curious to explore the extent to which regulation impinged on what you all did for a living back in the 1970s and 1980s, and whether it was as intrusive then as it is now. Or to put it another way, how easy was it for you to run rings around regulators, which is a subsidiary element of the innovative spirit?

Michael Dobbs-Higginson: Regulators, as far as we were concerned, were seen but not heard. We really had very little interaction with them, because we were creating a market that they hadn’t come across before, so they didn’t really know quite how to respond. It’s only later on in the 1990s and 2000s when things started to go awry regulators felt they had to step in. In the old days of the 1970s and 1980s, it was a reasonably gentlemanly thing; people would play games but there wasn’t the egregious abuse that there was later, particularly since the arrival of the derivative products and their respective “black boxes”.

Before derivatives you didn’t really have the flexibility to abuse. You priced an issue wrongly or rightly, you were long or short but that was basically it. With derivatives and swaps that opened a whole new game and that’s when the regulators started to get seriously involved, although, like the senior management of many banks, they didn’t really understand what was going on.

Robert Gray: Of course, until the early 1990s you had the offshore market and then you had a series of domestic European markets, which had their own specific rules. For example, in the UK we had a queuing system; you had to submit the name of your proposed issuer to the Bank of England and wait your turn.

Then in Spain the Matador Market was gradually liberalised to allow supranationals and then sovereigns. In France you had the Euro-French franc market and the domestic French franc market; the latter limited to domestic issuers while the Euro-French franc market was for foreign issuers. French investors couldn’t invest in the Euro French franc market.

Germany had its rules, too. In fact, it didn’t allow foreign issuers until 1992, and it had an extraordinary impost for underwriting risks. The fee structure in Germany had a special underwriters fee, which was designed to protect the underwriter against legal liability from bondholders.

Cyrus Ardalan: It was a frontier world at that time. We were making things up as we went along in a sense; things were being created all the time. There was no precedent and there were no rules and regulations, simply because the markets just simply didn’t exist. All you have to do is look back at the number of compliance people and risk management people that we had in the mid-80s; you could probably count them on one hand. Big banks today have literally thousands of people involved in compliance and risk management.

Michael Dobbs-Higginson: We didn’t have any at White Weld or CSFB …

Cyrus Ardalan: At Paribas, we had very, very few. When I was in New York for the first time, we hired a risk management person and put in a compliance person, so two compliance people and their main job was actually doing KYC [Know your Customer] for clients. I recall a very humorous situation when one of them came to me one day and said, “I think we have a problem”. I said: “Why”? He said: “This company called something African something Fund has given me their financials. I just compared then to Security Pacific and they’re identical”. That was compliance in those days; it wasn’t compliance in the sense that we know it today.

Robert Gray: Yet investors didn’t suffer losses and there was very little litigation. The only case I can remember in fact being sued as an underwriter was on a Salomon Brothers led commercial mortgage backed security in the mid-80s. As I recall the issue was the adequacy of disclosure in the prospectus of the presence of asbestos in the building. That was the only case I can remember where we were sued on a prospectus.

Michael Dobbs-Higginson: I pulled a billion-dollar deal for Robert Holmes a Court [the corporate raider who owned diversified conglomerate Bell Resources], in Australian dollars in 1987 at the time of the crash. He came to me and said: “this is impossible; you have to do it”. Thank God we didn’t do it because we would have lost several hundred million dollars but he tried to sue us; as did Alan Bond [another Australia-based entrepreneur] who subsequently bought Bell Resources. They didn’t succeed, because we had a force majeure clause. That was the only time in my 20 years where we actually had somebody trying to sue us.

To continue reading this roundtable, click the relevant section. Introduction - Participants - Part 1 - Part 2 - Part 3