IFR ASIA: I think the first question is really what’s behind the Asian Reg S phenomenon. Lorna, I know you’ve done a lot of work on this.

LORNA GREENE, NAB: There are a number of macro trends that are driving this. Certainly, we’ve seen a shift of wealth from the West to the East. There is the rising middle class across Asia, in particular in countries such as China and India. We are also seeing that there are quite high household savings rates as well amongst a number of countries in the region and all of these factors have led to the deep pools of liquidity that we’re seeing, and an increased amount of funds that are available to invest.

Apart from the macro trends, the dollar market in itself has presented a lot of value for many investors over the course of the last 12 months in particular. We’re seeing the impact of quantitative easing in some other Asian regions. For example, Taiwan and South Korea have been cutting rates and that’s been driving a lot of those investors to look to dollar assets for enhanced returns over those achievable in their domestic markets.

IFR ASIA: It used to be the case that a bad day in the US would mean the Asian markets were completely closed. Have we got to a point now where that doesn’t apply anymore?

MARC LEWELL, JP MORGAN: I think that’s right, Steve. Obviously, this is the Reg S bonds roundtable but I’d always be a little bit careful from distinguishing between Reg S and 144A, because what we’re really talking about is the Asia investor pool. Now we’ll come to talk about format later, but what that means is the Asia market is able to support transactions – whether they’re from Australia or the rest of Asia or even from Europe – and those deals could be in 144A format or Reg S format.

To your point, 15, 10 or even five years ago, a 144A trade might have been 40% placed in Asia and 60% placed in the US. These days many deals – Francis’s transactions, for instance – would be 90% Asia and 10% US if they were done under 144A. Lorna no doubt covered the ultimate causes, but the end result is that we don’t need the US investors on certain Asian transactions on a day-to-day basis.

BRYAN COLLINS, FIDELITY: You can see that in the investor base, either looking at primary market participation breakdowns or even just looking at our own investor base, which would be reasonably representative of the industry. Over the course of the last 10-plus years – and on all kinds of credit ratings, from high yield to investment grade – the percentage of Asian investors has incrementally gone up. It’s highly correlated with the primary market placements, as it is with our investor base. That really is the primary driver. Added to that you’ve got the emergence of a dedicated buyer base for Asian credit, and all the other dynamics that you’ve talked about in terms of growing wealth.

Interestingly, I think from the context of Australian issuers, the issues come about from pricing. We used to have – and we probably should still have from time to time a premium here in Asia – but that premium has been diminishing quite significantly on a like-for-like rating basis. An Australian issuer used to get a cost advantage by going to the 144A market. It’s now not there, or at least not as much, and they’re opening up to a much larger universe.

LORNA GREENE, NAB: Absolutely. And in fact we’re actually seeing that for many issuers, depending on the sector that they’re from, they’re actually achieving price benefits by targeting the Asian investor base more exclusively, whereas in some cases US investors are slightly more sticky on pricing. So, again, depending on the sector, you can actually get a price benefit if you’re just focusing on the regional investor base.

MARC LEWELL, JP MORGAN: We’ve seen several Australian issuers this year do 144A trades where they want to maintain the relationship with US investors, but focus the pricing on the tightest bid – which is from Asia.

We’ve also seen, for certain issuers, that the US pricing is still the most competitive, not just for Australia, but from around the region. Generally the Asia bid is the strongest for the ‘yield-ier’ transactions, or for transactions from an Asian issuer where the regional investors are most familiar with the name.

For many of the very high-rated global names, whether they’re in China or Korea or Australia, there is a bit of a floor in the spread or yield levels where Asian investors will play. For Jessica’s transactions, for instance, you see a much stronger bid in the US for the shorter end, because you can’t get to the tightest levels with Asian investors below a certain absolute spread number. For a Triple B minus credit, very clearly this year the strongest bid has been from Asia. For a Double A or Single A it is much more of a balance.

LORNA GREENE, NAB: That’s a good point regarding tenors, and obviously this is yield-driven. Certainly, a lot of the corporates who are looking for longer-term debt tend to get a better reception and better pricing outcome by doing, say, a 10-year transaction targeted to Asian investors. That’s what we really see coming through now. The yield is there, but at the same time it’s usually issuers from the utility or infrastructure sector who are looking that for that longer-dated funding.

IFR ASIA: Let’s bring our issuers in on this. Jessica, how do you decide between different markets and formats? Is it simply pricing?

JESSICA GU, KEXIM: Certainly pricing would be the primary factor that we need to consider. It’s a mixture of the pricing and diversification, having a balanced range of investors in different regions, different asset classes. So it’s a mix of everything, I would say.

In case of Kexim, I think we can be easily recognised now as one of the big beneficiaries of the very deep liquidity in Asia. I heard from my predecessors that before the GFC we used to follow the strategy of announcing a Reg S/144A deal in US hours – back in the mid-2000s, I would say. After the GFC, I remember that’s when I first joined the foreign currency funding team, bankers were saying to us, “It’s now the new fashion that the deal has to start in Asia.” The order book has to be built strongly in Asia in order to carry the momentum into the Europe and the US line.

It’s quite obvious to me that we’ve been benefiting a lot from the larger size of the Asian order book, as that could always play a factor in compressing the spread level that we have to pay.

Although we engage in SEC-registered deals for benchmark-sized global US dollar transactions, we still depend on the Asian investor base a great deal.

For a three-year or a five-year transaction, more in the shorter to mid-part of the curve, it’s a fine mix. I would say typically 40% would be in Asia and 40% in the US and the rest in Europe. Then in the longer part of the curve, it’s definitely more about Asia. It’s more like 60%-70%. Also the spread differential from 5 to 10 years remained quite flat, almost in single digits.

IFR ASIA: It might be useful just to define all the terms we’re talking about here. Alex, let me come to you on these. So in my understanding a US investor overseas can still play in a Reg S deal, no?

ALEX LLOYD, CLIFFORD CHANCE: It’s slightly ironic. Reg S and Rule 144A are, of course, regulations under the US federal securities laws. They actually refer to when transactions are exempt from the registration requirements under the Securities Act – when you can sell in the US, or to specified US holders, without having to register with the SEC.

It’s become a short-hand for geographic description of markets. 144A is an exemption for the registration requirements. It allows you to access qualified institutional buyers in the United States. That is a significant pool. The definition of a qualified institutional buyer really covers most types of financial institutions that you would expect to buy bonds. So 144A, effectively, becomes access to the US.

Reg S, which is, again, a US securities law definition, essentially defines what is considered by the Securities Exchange Commission to be offshore. If the transaction follows those rules it’s outside the United States.

Now there is nothing in either of those regulations – Rule 144A or Regulation S – that covers documentation. The distinction is that to the extent that you access the United States under 144A you also carry with a potential liability under the US federal securities laws for disclosure. There is a perceived and actual litigation risk, and that risk drives a view as to what is the minimum documentation required.

A properly written Reg S transaction will not expose you to that disclosure liability in the United States, but obviously any issuers and their financial advisors remain potentially subject to liability for fraud and other applicable laws in any jurisdiction.

One of the key things I think that influences a lot of people’s choice of the Regulation S market is effectively speed to market. You’ll notice that most medium-term note programmes utilise Regulation S. It’s actually quite difficult to utilise the 144A on a regular basis – unless you are a very regular reporter, preparing quarterly reviewed financials and things like that, which most Asia-based issuers are not doing. They’re usually doing it on a semi-annual basis at best.

That’s one distinction that comes out of the legal framework, that issuers in the Reg S market can come to market quicker.

IFR ASIA: I’ve always assumed there’s an additional documentation cost attached with a 144A issue. But it’s really about disclosure, isn’t it?

ALEX LLOYD, CLIFFORD CHANCE: There is, as I said, because you are subject to a potentially higher liability regime in the United States, there are additional procedures that you need to do. For example, there are limitations as to what financials you can use. Financials go stale after 135 days, which means that when you’re looking at accessing the 144A market, you may have to incur the cost of an interim review that you wouldn’t perhaps do in a Regulation S context.

IFR ASIA: So the lawyers don’t make any more money out of them?

ALEX LLOYD, CLIFFORD CHANCE: Unfortunately not. I would encourage you always to do your due diligence and to understand the issuer, because there is a potential liability in the US that extends not only to the issuer but also to an underwriter. Everybody is invested, as it were. You do tend to see a higher degree of documentary due diligence and management due diligence.

The need for more current audited financial statements, and requirements that auditors provide comfort letters, again increases the amount of work that the auditor has to do. Ultimately, the lawyers are required to provide 10b-5 disclosure letters, which again means that they have to go through a larger amount of diligence to assure themselves that they’re in a position to give that comfort.

IFR ASIA: All of that sounds good for investors. But if you have all that disclosure, then does that justify a different price?

MARC LEWELL, JP MORGAN: I would say – and we should hear from the issuers, too – while the additional legal or auditing fees may be there, in practice they become something of a rounding error in terms of basis points, especially if you’re any sort of frequent issuer. I think that’s demonstrated by the fact that most of the 144A or SEC registered issuers continue to issue in that form, even though the market has become more Asian in distribution at the current point in time.

The main barrier to issuing in 144A over Reg S is the hassle and the time taken to be ready to market, especially the first time you issue. I can think of only a handful of issuers that have done that work once and then later gone back to Reg S, if they’ve issued relatively soon afterwards. Actually, the cost of doing a second or third 144A transaction versus a Reg S when you’ve already done the first document is very, very similar.

BRYAN COLLINS, FIDELITY: I would expect that we will see a lot of the issuers that are only doing Reg S now eventually move to 144A as the market gets larger and potentially saturated by a particular type of country risk or sector risk.

We’ve already seen this in some of the high-yield names. They started with Reg S, built a curve and then later on life they’ve broadened their horizons and gone to 144A to try and expand their investor base and to reach new investors – in the same way that you would have US issuers eventually come to Asia to broaden their horizons.

There is a very high correlation with credit quality, and you’ll typically see the very high-rated names issuing frequently in both formats. You typically don’t see it very much down in high yield, unless it’s a particular sector or company which is deliberately trying to reach both markets. We see that here in this part of the world with some of the technology or gaming names that are deliberately reaching different investor pools, because you’ve got a large, dedicated investor base.

All things being equal – which is rarely the case, I know – if you’ve got a corporate that’s using Reg S and 144A regularly, they’re probably going to be a higher quality issuer. It also demonstrates takes its creditors seriously, to some extent, and that typically rewards them with a lower cost of funding, but I stress that it’s correlated with the underlying credit quality.

MARC LEWELL, JP MORGAN: That’s why you’ll see a lot of high-yield issuers issuing in the Reg S market but using a 144A format, partly because the investor base that’s looking at the credit would expect to be able to do full diligence on the issuer, but only a 144A-style offering document would give them the information they need.

LORNA GREENE, NAB: The other advantage of issuing in Reg S-only format is actually for those issuers who don’t have a very large funding need; the minimum benchmark size being smaller. So what we find quite often, particularly for our Australian corporate clients who don’t have a very big funding requirement, they will raise maybe US$300m–$400m and that will satisfy their funding need for most of the year, because many will also want to continue to maintain a presence in the domestic market. For issuers like that, we won’t see them go the whole way to 144A because they just don’t need to.

FRANCIS HO, CLP: From the issuer perspective, a lot of corporates are fairly flexible in looking at different funding opportunities. I believe treasurers will pay a lot of attention to a couple of things: first, management time; second, the certainty of the transaction and the prompt response from investors. In the past, we have been told by our bankers that Reg S works more for smaller size companies that are located in this region or for lower targeted fundraising amounts, so yes, we have gone for that.

I certainly understand that this is the more practical, easy way to issue. It caters better to certain companies that are more moderate in size. They have less frequent funding needs and their management, in terms of resources and management time, they don’t want to travel to the US. These are very important factors.

Even then, a fair number of companies in the corporate sector – like CLP – will accommodate both 144A and Reg S in their documentation. We also understand the incremental costs for the documentation are minimal, so the treasurer would be able to convince senior management to go for both when drawing up the documentation. When it comes to pulling the trigger it depends on the funding cost.

BRYAN COLLINS, FIDELITY: There are some technical and administrative dynamics around the initial Reg S and 144A format from an investor’s perspective, and, again, it’s highly correlated to the credit quality. Generally, it’s to do with the timing of the deal. If you’ve got an Asia-based issuer, trying to issue into an Asian investor base, it’s a good concept to have the final pricing, a firm view of the book and all the other terms sorted by the end of the Asia trading day.

It happens rarely these days, but it used to happen quite a lot that all those terms were finalised in the middle of the night and we were basically giving issuers a free option if we wanted to participate.

The technical dynamics are tricky to assess, but typically deals which have a foothold in both the Reg S and 144A markets are technically better. They’re not as volatile. You might have different taps of liquidity in US hours, for example, through a global trading desk or through using global banks to help trade and execute overnight. We can hold 144A or Reg S, it makes no difference, but we might participate in a primary market deal as a global book and deliberately take 144A, because we know that will be more liquid for us if we are going to be trading either here, in Asia or outside the region.

Interestingly, some mandates that we have in some jurisdictions here in Asia actually limit the amount of 144A securities that you can hold. It can be quite a generous limit, but even a 20%, 30% cap on 144A exposure within a portfolio does come up from time to time. That naturally puts a cap on how much Asian-based institutional investors will actually put into 144A.

MARC LEWELL, JP MORGAN: I think there’s a big difference between different types of credits in different jurisdictions. Even before this recent rush of Asian demand over the last two years,

Francis’s bonds will have been most at home in Asia for a long time. Hong Kong has always had a lot of dollar liquidity, and CLP is sort of Hong Kong royalty. There’s a very natural domestic and regional bid.

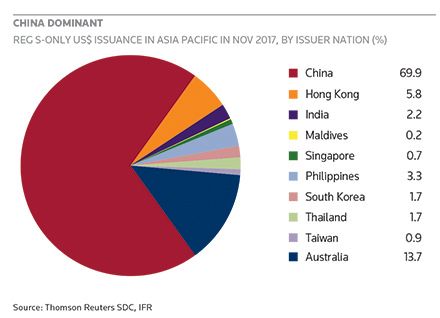

What we’ve seen over the last few years is a huge growth of offshore China money. When we talk about the growth of the Reg S market, from an intellectual perspective, we have to look at the growth of China. Except for the global tech names, the oil and gas giants and some of the quasi-sovereigns, in many ways it’s really a greater China regional market that operates somewhat differently from issuers from the rest of the region.

I think the trends are more normalised if you look at Indonesian or Korean trades. Actually, I don’t think they have become meaningfully more Reg S. We have seen a big growth in high-grade Australian or European issuers looking at Asia. But for most of Asia outside of China, there’s still quite a good balance between US distribution and Asian distribution.

IFR ASIA: The China point is excellent. Are we really talking about Asian liquidity here, or is it Chinese buyers and Chinese issuers just connecting offshore? And does that risk flowing through and distorting prices in the wider market?

MARC LEWELL, JP MORGAN: My view is that it starts off with China buying China, but once it reaches a certain level the international investor base in the region will also participate – they may take sometimes only 10% of the transaction, but other times they will take 50% or 60% of the deal versus the China share. Clearly, there are issuances where the best bid is very clearly from Chinese investors who know that issuer best.

But that has all added to the volume, and that is also helping global investors dedicate resources to their Asia-centric businesses, because you have a bigger market overall. Then you have a self-fulfilling prophecy, as more investment funds dedicate more resources to the regional credits as well as the global ones.

LORNA GREENE, NAB: I would say if you look at the issuance from Chinese borrowers, the actual allocation to offshore China funds has been decreasing. We’ve seen increased proportion from other parts of Asia but also increased demand out of Europe, in particular. I think that’s been a positive development.

BRYAN COLLINS, FIDELITY: Keep in mind that the investor base will have a natural home bias. So a Philippines-based financial institution will have a natural bias for the Philippine US dollar paper, and we all understand the structural dynamics there.

Indonesia is not at that same level yet, but it will be at one stage, and India is obviously heading in that direction, too. Hong Kong and Singapore have been much more global, but still have a very strong domestic buyer base. It’s actually very much the same for Korea and even Japan, with the domestic bid at times swapping it back.

You will always have that natural bias. For a Chinese institutional investor, in whatever form that might take, to have a bias towards a name they know is natural. Same for the US, same for Europe.

FRANCIS HO, CLP: I believe it’s more than China opening up. Since the Asian financial crisis 1997-98, the regional governments in APAC have started to rethink how they manage their financial sectors. When we look back at 10 years ago, when the global financial crisis kicked in, this region was in good shape in terms of financial stability, liquidity, asset management and so on.

First we saw Japan building up its wealth, and that liquidity coming to investors outside of the country. Over the past two decades or so, we started to see Taiwan, China, Korea, they all have developed this capability. It’s because of the macro-economic situation, the international financial market development, and the government even encouraging the private sector insurance companies or the banks to start looking at investment opportunities overseas.

BRYAN COLLINS, FIDELITY: One of the benefits for Asia looking at both hard currency and local currency funding is that it presents alternative sources of funding. China is an immensely powerful illustration of what a domestic capital market can do. We’ve seen just in the last couple of years the dynamics around Chinese corporates borrowing in dollars to pay down onshore and onshore to pay down dollars. Obviously the capital controls have created some complexities, but these two markets now operate almost in parallel to each other. That gives companies immense flexibility, and also helps mitigate systemic risks.

IFR ASIA: Jessica, from your experience dealing with different investors in Taiwan and other Asian markets, do you find they respond better if you go into their home market?

JESSICA GU, KEXIM: Very much so. I guess Kexim has been quite lucky in being able to tap the US dollar Formosa market three times already. Our first Formosa deal was in the US dollar currency back in 2010, even before Formosa market became popular. Then we did our second transaction in 2016, and one more this year as well.

The size of the deals was a lot bigger than we expected, actually. We first had this expectation that the deal would be about US$100m–$150m, but it ended up being more like US$350m–$400m. The technical dynamics as well as the spread level were all very affirmative for us. We found investor communication simple and straightforward hence easier to get clarity from that dedicated investor base in Taiwan.

I had the experience of meeting with a lot of investors after the 2016 deal, and the response we got was very, very straightforward. We would talk about the levels where both investor and issuer would agree, and it was very clear that a deal could be made. In terms of size, each individual investor had very big pockets of money to deploy. We benefited a lot from those deals.

IFR ASIA: Are these investors that you already knew from your global US dollar deals?

JESSICA GU, KEXIM: Some of them, yes. We were also there to tap into investors that were not very familiar with us, in that they did not really participate in our trades before. I guess the export-driven economy of not only China, but also Taiwan and Korea, has distributed a lot of the wealth gained in those countries quite evenly, so there were newly discovered pockets of investors that we were able to meet for the first time.

MARC LEWELL, JP MORGAN: We’ve seen quite a lot of cases where there’s been this cross-fertilisation around Asia and I think that is very healthy for the Asian market overall.

We’ve seen investors coming into credits for the first time through the Formosa side, whether it’s for Kexim or a US or European issuer, and then those same investors participating more actively in the next 30-year US dollar benchmark.

Similarly, we’ve seen a lot of Korean, Japanese, Taiwanese participation in Australian dollar transactions, either for Australian issuers or for global issuers issuing into the Aussie market. Again, that can then lead to a greater participation in future dollar deals for those issuers – in Reg S or 144A form.

LORNA GREENE, NAB: Of course if you come to their home market then they will be more inclined to do the credit work as they have everything in place to able to participate.

BRYAN COLLINS, FIDELITY: There’s a key trade-off there from an investor’s perspective. If you’re away from home, and you’re investing in a domestic currency market that’s not the issuer’s natural base, you will have liquidity problems in times of stress. There will be less bids out there, the pricing won’t be as great in the secondary market. You do need to be sensitive to that.

Go back and look at the global financial crisis and how the European names performed in the Aussie dollar market. How did the European and other issuers perform in the Japanese yen domestic market? Even the Hong Kong dollar market, there were quite a lot of European issuers, and some US banks. They were all impacted. So that’s definitely something we consider.

However, the flip side of that is when you see those dislocations we can take advantage of it. From an Australian investor’s perspective, you’ll probably make more money buying a US dollar bond and swapping it back. There are lots of other examples we can do that, when you look at the Korean Won market, or the renminbi. Those dislocations will come and go, but it’s our job to exploit that.

MARC LEWELL, JP MORGAN: Bryan raised an interesting point, which we haven’t touched on here. Clearly, some of the growth of the Asian market comes from the macro story: there is more money in Asia than there used to be. That is a secular trend. But some of it is also to do with the fact that Asia has been more bullish than the rest of the globe, partly driven by that wave of abundant liquidity, and therefore pricing has been more aggressive.

The next real sell-off will be an interesting test for the market. If there is another crisis or another correction at some point, what will happen to the Reg S market?

From a historical perspective, in a real crisis the market that recovers first is almost always the US. It may not be at a price that everyone likes, but there is almost always a price in the US market before other markets adjust. It’s the most liquid and most mature market, because it’s been around the longest. It’ll be interesting whether the Asian bond market can weather a real patch of volatility, and whether that growth is as permanent as we think it is at the moment.

ALEX LLOYD, CLIFFORD CHANCE: I think you’ve also got to be a bit concerned about storing trouble for the future. The bonds that tend to recover the best are those with real transparency and credit discipline behind them.

When I started looking at China issuance into the Reg S market 10 years ago, if you had an investment-grade rating you could issue in the Reg S market. If you were sub-investment grade or unrated, or you were using some funky credit support structure, you needed the 144A market to give you the access to sufficient liquidity. That also imposed upon the issuer a degree of discipline in order to meet the requirements of the 144A market.

As the Reg S bond market has grown and this wall of money you’re referring to has come in, it’s become easier and easier for issuers to access the international market without necessarily – I don’t want to sound too prejudicial – but without necessarily doing the work to justify it. We now have a lot of transactions with implied credit support, particularly out of China, be it from ‘keepwell’ agreements or equity purchase undertakings or whatever. These are largely untested forms of credit support, and in a Reg S issuance they are coupled with a slightly more relaxed or lower level of disclosure for the issuer itself.

While the market is buoyant, that’s fine. When the market turns the investor is going to say: “Well, actually I don’t know as much about this issuer as I thought I did. I haven’t seen regular financials and I’m not necessarily sure about the strength of either government support, if it’s an SOE, or the enforceability of these credit support mechanisms.” There is a danger that people tend to see the Reg S format as shorthand for doing less work to get into the market.

BRYAN COLLINS, FIDELITY: The diligence on the credit, the engagement with creditors and disclosure and transparency are all critical. Add to that, you don’t necessarily have that same bid from a domestic investor or a US-based institutional investor who might see value emerge at some point. That’s potentially limiting some support. Would an investor naturally come to that market for the kinds of names you were describing? Debatable. The other dynamic is if you throw in a little bit of leverage, that can obviously make the situation even more interesting.

It is something that we are actually debating quite a lot. In a period of dislocation, what would perform better? There’s a very strong case for lots of issuance coming from China. They have a bigger pool of domestic investors who have got much deeper pockets than many other investors around the world.

So you’ve got this trade-off of some credit concerns on one hand, backed up by some very deep pockets on the other. It’s quite a complex one, but it is going to be very interesting one to manage, but at the end of the day fundamentals will help you in those situations.

IFR ASIA: This comes to this next big picture question. Does this mean then that Asia is becoming more exposed to rising US interest rates or does it go the other way? Does this local pool of money give Asian issuers some protection from global shocks?

LORNA GREENE, NAB: Yes, absolutely agree. With rising dollar rates, of course, there’s going to be more appetite because of the additional yield that that provides. Then from an issuer’s perspective, being able to tap into those funds in US dollars may be simpler than looking at issuance in some of the local currencies in the region.

I think from that perspective it’s probably going to present an opportunity and we’ll see more issuance, from debut issuers as well as frequent borrowers. It’s obviously easier just to go and issue in US dollars than try to tap into some of the local markets by issuing in those domestic currencies.

BRYAN COLLINS, FIDELITY: I’d still be inclined to think that if rates are rising in the US, it’s because the conditions are genuinely improving, and that’s probably going to be quite good for global growth, not just regional growth. Also, let’s be really frank, we’ve had extraordinary monetary policy for many years now. Funding is not expensive for good quality corporates.

MARC LEWELL, JP MORGAN: More fundamentally, no one expects US rates to go from where they are now to 5%. In practice, the risk on Treasuries is likely a maximum move of around 100 basis points. If we look at highly rated investment-grade or high-yield names, rates risk isn’t a real problem. A company that’s raising money at 5% today will generally have plenty of room in terms of interest coverage.

Historically, what hurt companies in the Asian financial crisis wasn’t rates going up; it was funding in dollars while revenues were in local currency. I think that’s much less of a concern today, simply because issuers and investors are much more focused on making sure that there is the right sort of hedge in place.

The bigger issue is if you see a serious back-up in high yield, and companies which are now funding at 6% become unable to fund or go back to having to consider paying a much higher yield. Did they have a business model that allowed them to pay the debt off over the course of the bond, or were they only relying on the market being there ad infinitum? That’s when you get the real challenge.

FRANCIS HO, CLP: This relates to how companies manage their financial discipline. I would say that interest rates are going to normalise, and that’s a good thing. Rates have stayed so low for so long, it’s better for everyone to see them normalise.

For corporates, if they only rely on the low interest rate environment to grow or to operate, then I believe there is a really high risk. It will be much more meaningful for a company to diversify not only its funding sources, but also the currency, market and investors. As long as the swap market is reasonably liquid, I believe a reasonable credit can now source funding from a lot more investors and at more reasonable cost.

From my perspective, I think treasurers should be more alert on getting ahead of the headwinds including, if they can, meeting investors more often, rather than only when they do a deal. Our objective is very straightforward. We like to see investors who are engaged with the company soon after any results announcement, so that they can raise their questions. They can see the management and they can do their due diligence. When we go to the market then we can focus more on the commercial aspects.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com

| Kexim case study | |||

|---|---|---|---|

| US$2bn three-part global notes | |||

| Pricing date | 24-Oct-17 | ||

| Format | SEC-registered | ||

| Rating | Aa2/AA/AA– | ||

| Total orders | US$4.4bn; 200 accounts | ||

| Tranche 1 | Tranche 2 | Tranche 3 | |

| Principal | US$400m | US$1bn | US$600m |

| Maturity | 01-Nov-20 | 01-Nov-22 | 01-Nov-22 |

| Coupon | 2.50% | 3.00% | – |

| Reoffer | 99.65 | 99.853 | 100 |

| Spread | T+90bp | T+100bp | 3m$L+92.5bp |

| Distribution | US 35% | US 41% | US 17% |

| EMEA 25% | EMEA 20% | EMEA 20% | |

| Asia 40% | Asia 39% | Asia 63% | |

| Source: IFR | |||