Gold standard

For skillfully navigating a difficult market, successfully weighing up risk-reward and making bold decisions when advising borrowers, and for consistently supporting sponsors and investors by underwriting and distributing large and small deals, Goldman Sachs is IFR’s EMEA Loan House of the Year.

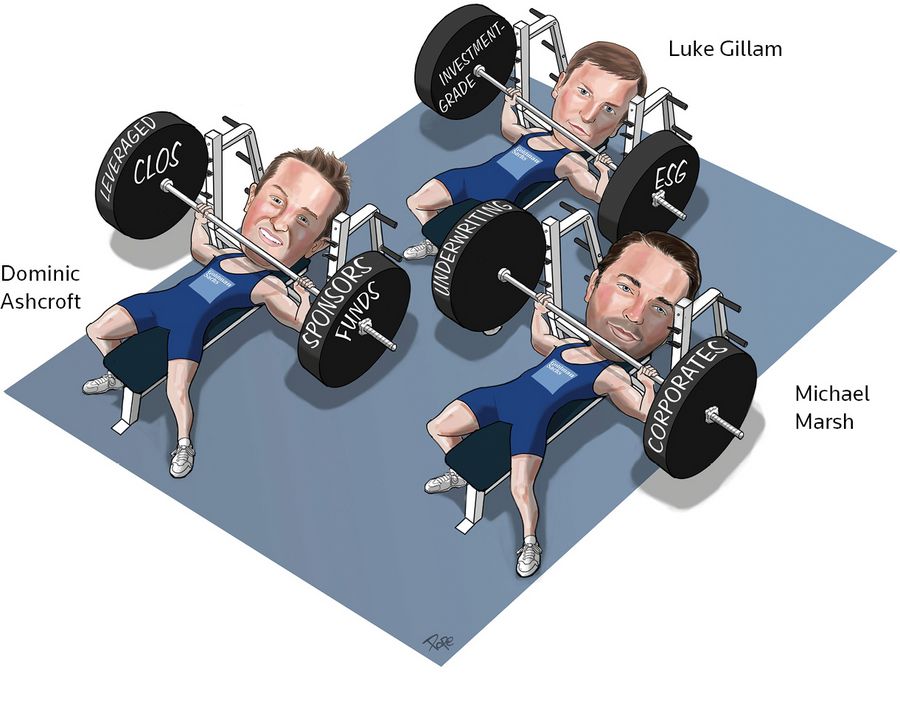

Goldman Sachs was a formidable force in the European loan market in 2019, a heavyweight in leveraged and investment-grade deals, as well as providing innovations in fund financing and ESG. In a year that saw most loan teams coming in 40%–50% under budget, Goldman performed strongly.

“Despite a tough year, in terms of deal count and P&L we were up. It was about market read, and being upfront and engaging with clients,” said Michael Marsh, head of EMEA credit finance at Goldman.

In a year dominated by public-to-private transactions, Goldman underwrote and distributed a €375m-equivalent second-lien loan for Swedish tool supplier Ahlsell, the largest second-lien since the financial crisis. It also handled a €1.56m first-lien loan for Ahlsell, one of the largest LBO-related TLBs of 2019. Goldman is one of the lead banks on a £2.517bn financing for UK defence group Cobham, one of the biggest loan underwrites of the year.

Goldman had a leading role on several other headline financings including a US$7.5bn debt package backing US-based Berry Global’s £3.34bn acquisition of UK packaging company RPC.

It also led a US$750m loan for UAE-based private educator GEMS Education, the largest ever TLB in the region; and raised the first ESG-compliant leveraged loan, for Spanish telecom company Masmovil.

Goldman led the dialogue with sponsors to successfully master the delicate balance of pushing aggressive terms while achieving successful outcomes. It had a good read of the market and took on deals that were not straightforward.

“It was a difficult year and a lot of clients came to us asking for advice on how to approach situations. We were not just a term-sheet ticker. One sponsor said we were the only bank making comments, not just agreeing to the terms sheets with a view to changing them after,” Marsh said.

Goldman led a US$1.1bn-equivalent refinancing loan for Swedish chemicals firm Perstorp. The loan reduced the borrower’s weighted average cost of debt by 300bp and closed oversubscribed with the majority of demand from new investors.

“Perstorp was a risk decision and we took leadership by helping them put a syndicate together. It was not the easiest to work through and that is where we added value to the market by taking a view,” said Dominic Ashcroft, Goldman’s co-head of leveraged finance capital markets in EMEA.

Goldman also led a €940m financing to back a buyout of French budget hotel chain B&B Hotels, which included a second-lien loan on the recommendation of the bank.

“We were the only bank that asked for a second-lien flex on B&B. If we had not it would have failed syndication or been outside the flex. Instead, the deal was a success,” Ashcroft said.

Goldman was not just there for the big LBOs – it served clients across the board, including an inaugural institutional financing for German traffic safety firm AVS with a €300m TLB.

Goldman also supported clients by putting its balance sheet to work, investing in leveraged loan transactions across first and second-lien and mezzanine debt.

“Goldman put around US$4.3bn to work in 2019, one of the largest deployments of capital in Europe,” Marsh said.

For example, it provided a unitranche facility of £325m and an acquisition facility of £75m to back the acquisition of listed media company Tarsus.

Goldman increased its presence in investment-grade, as one of three underwriters on the US$13.2bn-equivalent bridge loan backing London Stock Exchange Group’s acquisition of data company Refinitiv (owner of IFR), and one of the lead banks on French software company Dassault Systemes' €4.45bn loans for its acquisition of life sciences company Medidata.

“Clients recognise our ability to move quickly and to provide large capital commitments in big M&A financings,” said Luke Gillam, the bank’s co-head of leveraged finance capital markets in EMEA.

In terms of overall market presence, Goldman was viewed by its competitors and sponsors as best in class.

“GS has been over everything; it’s a Goldman year,” a capital markets head at a rival bank said.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@refinitiv.com