Trading volumes in Greek credit-default swaps, the derivatives contracts politicians once accused of fuelling the eurozone crisis, have surged to levels not seen since the country's historic debt restructuring.

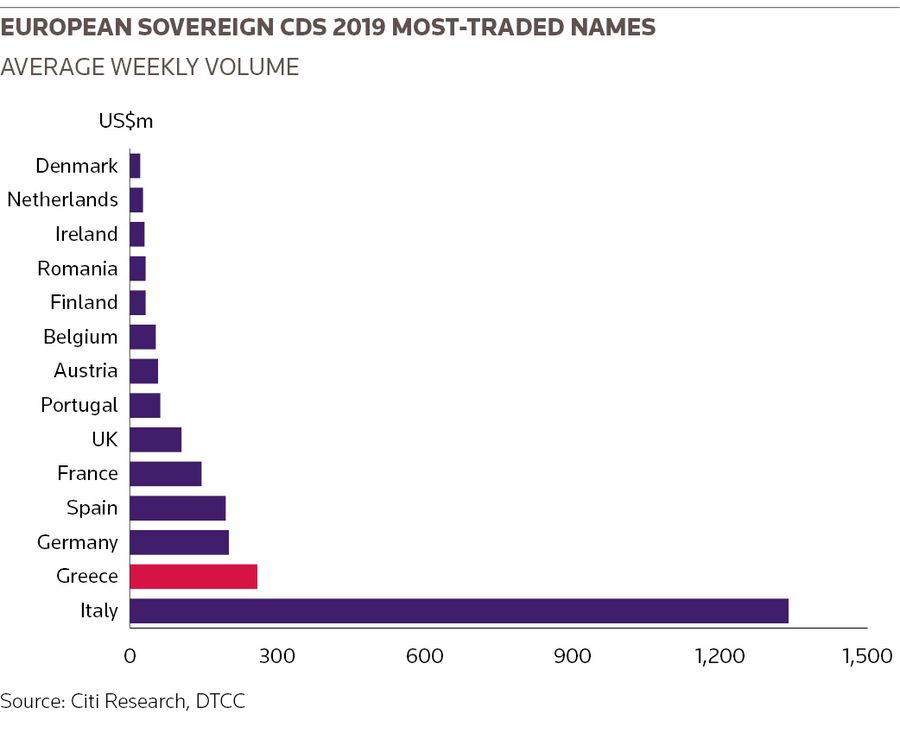

Greece has become the second most traded European sovereign CDS this year behind Italy, according to Citigroup analysis of DTCC data, with US$259m changing hands on average each week in 2019.

This time, though, analysts say the sharp uptick does not reflect concerns over the local economy. Instead, it is most likely linked to bank trading desks using CDS to hedge their exposure to Greece stemming from derivatives contracts used by the country’s debt office to manage the sensitivity of Greece's debt to interest-rate moves.

This year's plunge in market interest rates, with euro swaps plumbing record lows, may have left Greece sitting on paper losses on some of those interest-rate swaps. That, in turn, could have encouraged banks on the other side of those swaps to use CDS to hedge their increased exposure to the country.

"It is likely that hedging needs have picked up across the year – allowing CDS trading volumes to boom," Citigroup credit strategists wrote in a report last week.

Buying of CDS protection "anecdotally ... seems to have largely been driven by bank CVA desks," they added, referring to the desks that manage banks' counterparty risk from derivatives trades.

BOOMING VOLUMES

Default protection costs on Greek debt have tumbled this year thanks to improving fundamentals and loose monetary policy in the eurozone. Five-year Greek CDS have narrowed from 468bp at the end of last year to 155bp on Thursday, according to IHS Markit.

That has coincided with a sharp increase in CDS trading volumes. Greece can account for as much as 10% of the volumes in the European sovereign CDS market at times, Citigroup said, with up to US$700m trading in some weeks.

Even during the sovereign crisis, Greece never consistently accounted for much more than 5% of total trading, although overall market volumes were far higher back then.

The only European country with higher CDS volumes is Italy, with a whopping US$1.3bn trading on average each week. Italy not only has the largest amount of government debt in Europe, it also has used derivatives to hedge risks such as interest-rate moves. That activity encourages banks on the other side of those trades to use CDS to manage their exposures to the country.

BLAST FROM THE PAST

Greece controversially used derivatives in the early part of this century to help reduce its debt load - a move that came back to haunt the country years later when concerns over its colossal debt pile sparked the eurozone crisis.

There is nothing to suggest Greece has put on similar trades this time.

But Greece's Public Debt Management Agency has said in public presentations that it has used a number of measures, including derivatives, to significantly reduce the amount of its debt linked to floating interest rates.

The vast majority of Greek debt is held by official institutions like the IMF and the EU, which often lend at floating rates of interest.

In 2016, 70% of Greece's debt was linked to floating interest rates, according to a PDMA presentation. That portion had shrunk to just 9% in the first quarter of this year.

It is very difficult to know the terms of any derivatives deals Greece struck with investment banks given such trades occur in private markets. But PDMA presentations suggest a decent chunk of those swaps were executed over the course of 2018, when market interest rates were higher.

For instance, the five-year euro swap rate fluctuated between about 0.4% and 0.1% in 2018. It then fell steeply this year to a record low of less than -0.6% in August, before rebounding slightly.

That decline means the PDMA could be facing paper losses on any derivatives trades struck in 2018 that swapped floating interest rates for fixed rates.

The PDMA did not respond to repeated requests for comment.

Greek CDS volumes have picked up as 2019 has worn on and swap rates have decreased, with a spike over the summer period when rates bottomed out.

The Citigroup strategists also noted that Greece has issued several new bonds this year. Again, it is difficult to know whether there were swaps accompanying the bonds, but there has tended to be a pick-up in CDS trading after the new debt sales, they said.

"Since the start of 2018 it is quite possible that bank exposure to Greece has actually risen, in turn requiring increased aggregate need to hedge with CDS,” the Citigroup strategists wrote.