Carnival levered investor faith in the resurrection of the cruise industry last week, as it landed just over US$1.26bn-equivalent of subordinated debt which will rank behind billions of dollars in debt already raised by the company since the coronavirus crisis.

The cruise business has been one of the worst hit by the crisis, after several ships, including some owned by Carnival's Princess Cruises, became coronavirus hotspots.

Like many other cruise lines, Carnival now has no income, as its ships have been languishing in ports for months after all voyages were suspended.

But the company managed to raise additional cash to weather the Covid-19 downturn on the back of optimism about what may still seem a far-fetched scenario: the promise of a workable vaccine.

Global co-ordinators JP Morgan, Goldman Sachs and Deutsche Bank sent out price talk on Wednesday for two 5.5-year non-call three offerings; 10.25%–10.5% for a €400m euro note, and 10.5%–10.75% for a US$550m US dollar bond, after starting out with initial price thoughts of 10.5% area and 11% area, respectively.

Investor demand allowed leads to upsize the deal, landing €425m euro notes at 10.125% and US$775m in US dollar bonds.

The company's US$28.1bn security package for its new second-lien secured bonds is practically the same as its first secured deal issued in April. However, these will rank behind more than US$7bn of first-lien debt – making recovery in the event of a bankruptcy a trickier proposition.

There were no complaints from unsecured bondholders, said a source familiar with the deal, despite the fact that such investors now own debt that has been primed by billions of dollars of secured debt.

"Frankly, given the circumstances what is the alternative?" asked the source.

"There is no revenue – how else is the business going to survive? This benefits unsecured bondholders as well. All of these cruise companies are trying to bolster their liquidity as much as possible so they can weather the storm. When things get back to normality, they will start operating again."

That's something that investors can foresee – even at this early stage.

"There is a growing sense of expectation that this is something we can resolve and if that's true you can imagine cruise lines returning to profitability at some point," said John Bellows, portfolio manager at Western Asset.

Increased optimism on vaccines formed a positive backdrop for the deal on Wednesday morning, said David Knutson, head of credit research at Schroders America.

"The leisure industry is the most levered on there being some kind of vaccine or treatment," he said.

"It has lost the most and it will come back the hardest. Once there's a fairly reasonable outlook regarding a vaccine or treatment of that nature these bonds and leisure stocks will react immediately."

Carnival has now raised over US$11bn in new financing since voyages were paused – enough cash to see it through to late summer 2021 without any revenue, said the source.

But after that, the company will need to have 25 out of its 104 ships operational in order to break even.

Carnival, rated Ba1/BB–, is set to burn through US$650m a month in the second half of the year, said chief executive officer Arnold Donald, speaking on the company's second-quarter earnings call on July 10.

CONFIDENCE IMPROVING

Of course, improving market conditions also helped the deal through the pipeline, as central bank intervention across the globe has kept risk premiums down.

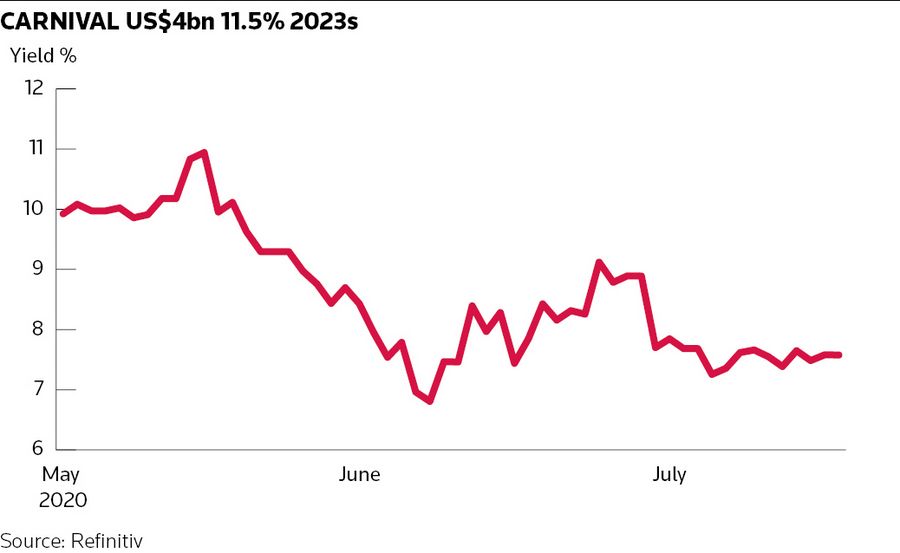

Carnival still had to pay up, although the 10.5% yield on its new US dollar bonds compares favourably with that on its first post-coronavirus bond sale – a US$4bn first-lien bond due 2023 that landed in April at 11.5% and an OID of 99.

"Investor confidence has materially improved since the deal in April," said the source.

April's debt raise saw Carnival pledge the lion's share of its assets, including the majority of its fleet of ships, as collateral.

Carnival's collateral package, valued at over US$28bn, includes 83 cruise ships, out of its current fleet of 104 ships.

In addition, the company is offering investors "material" intellectual property, stock pledges over vessel-owning subsidiaries and some inventory and casino equipment.

Carnival represents over 40% of the global market for cruises, and its LTV is the lowest among its peers, said the source.

The second-lien debt raise brings the company's LTV to around 29% – compared to over 50% for rival Norwegian Cruise Line.

"Look at Carnival's collateral, and the unique nature of its asset base," said the source. "The company is so large within its industry that yes, it has raised a lot of capital but relatively speaking to its peers, it has not raised a disproportionate amount of capital."

NCL was also in the bond market last week. Like Carnival, it was raising cash for the second time since March to help weather the Covid-19 pandemic.

It launched a US$675m 5.5 year non-call three senior secured note at 10.25% on Thursday. The notes (Ba2/BB) were sold via lead-left JP Morgan.

As security for those bonds, Norwegian offered a first priority in the Norwegian Epic cruise ship, which has an appraised value of around US$1.1bn. The notes are also guaranteed by subsidiaries that own 14 other vessels with an appraised value of US$4.79bn.

"WELL COVERED"

In addition to April's US$4bn bonds, Carnival's new second-lien notes will rank behind a US$2.8bn Term Loan B, and a US$200m European Investment Bank facility and 7.875% US$200m June 2027 first-lien notes.

"We currently own the existing first-lien notes which mature in 2023," said Mark Benbow, a fixed-income investment manager at Kames Capital. "Our view is you're well covered even in the event of bankruptcy. Even if the business halves and the leverage doubles, you're covered. But the more junior you go, the harder a decision it becomes as you start looking at potential impairments."

Carnival now has around US$1bn left in its second-lien basket that the company could raise via either loans or bonds, said the source.

"The unsecured market would be more challenging, but could also be a possibility. However, there would be a cost associated with it – and then it becomes, is it worth paying for the insurance premium if you don't have an immediate need for it?"