Major US and European banks set aside more than US$70bn for loan losses last quarter, up from less than US$16bn a year earlier and far higher than the first quarter as they took an increasingly gloomy view on the impact of the Covid-19 pandemic on the global economy.

The expected credit loss, or impairment charge, across 27 major US and European banks in the second quarter was US$71.2bn, compared with US$15.6bn in the second quarter of 2019, according to IFR calculations.

The same banks' credit charge in the first quarter was US$58.2bn, up from US$16.1bn a year earlier. That meant the aggregate charge for expected credit losses in the first half of this year is US$129.4bn – a whopping US$97.7bn more than was booked in the first six months of 2019.

Several bank executives and analysts said there is a lot of guesswork in the numbers, however.

"We're very clear, we cannot forecast the future. We don't know ... It's unprecedented what's going on around the world," JP Morgan chief Jamie Dimon told analysts as he announced second-quarter results. He said the true situation may not become clear for a while.

"It's just going to be murky, which is why if you look at the base case, an adverse case, an extreme adverse case – they're all possible – and we're just guessing at the probabilities of those things," Dimon said.

The challenge for banks is two-fold: their risk models have not gone through the type of recession and lockdown seen this year; and there is little consensus on the path of economic recovery.

"KITCHEN SINKING?"

That is resulting in a wide divergence in the prospective losses booked by banks. Even if they agreed on the path of recovery, credit charges would then vary by types of business, geographic footprint, the impact of government support measures, accounting rules and other factors.

But broadly, banks have baked more gloomy economic prospects into their credit costs.

Some banks appear to be more prudent than others, and may even be "kitchen sinking" bad news. US banks, in particular, have had a good year for trading revenues and could be more willing to front-load reserves now and write-back provisions later if the economy recovers better than expected.

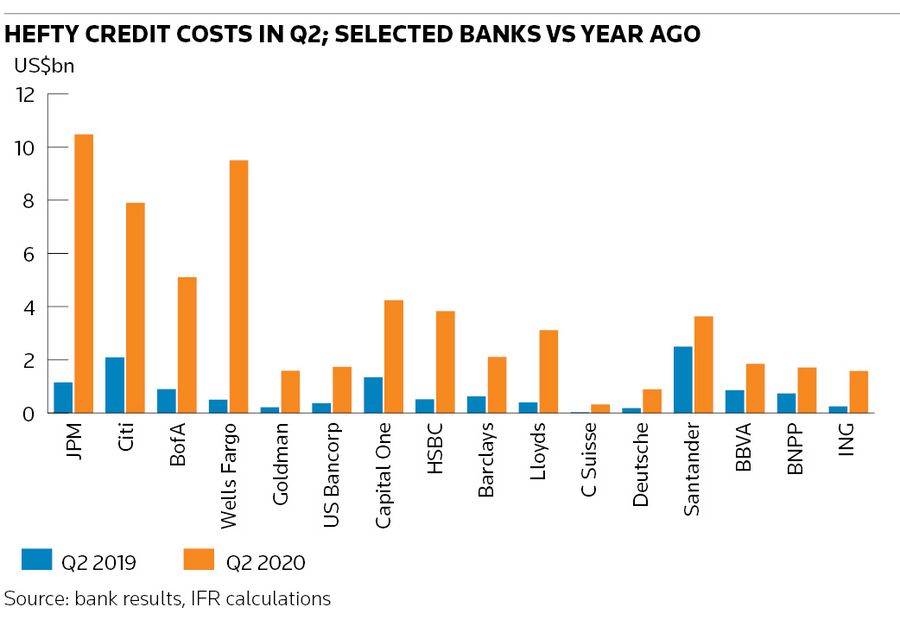

JP Morgan set aside US$10.5bn for loan losses in the second quarter, nine times more than a year earlier and taking its charge for the first-half to US$18.8bn – from US$2.6bn a year earlier.

Bank of America's second-quarter provision was more than five times last year's level and Wells Fargo's credit cost soared to US$9.5bn in the second quarter, compared with US$500m a year earlier and US$4bn in the first quarter. Regional US banks are also braced for losses – Pittsburgh-based PNC set aside US$2.5bn in the quarter, compared with US$180m a year ago.

The credit cost for 12 of the biggest US banks was US$44.6bn in the second quarter, or 6.3 times the US$7.1bn in charges they took a year earlier. That lifted their credit cost for the first half to US$79.3bn, or US$63.7bn more than a year earlier, according to IFR estimates.

British banks also took big hits. HSBC's credit cost was US$3.8bn, seven times its level a year earlier, and Lloyds and NatWest Group made similarly steep increases.

"The UK banks are facing a more significant economic drop than most Europeans as the UK has faced a bigger shock from the Covid-19 pandemic, and that has fed through into provision levels,” said Patrick Hunt, a partner at consultancy Oliver Wyman.

Fifteen of the biggest European banks took credit charges of US$26.7bn in the second quarter, or 3.1 times the US$8.5bn they set aside a year earlier. That took their first-half credit loss charge to US$50.1bn, or US$34bn more than a year ago.

BEST ESTIMATES

Given the uncertainties, few banks provided guidance for the full-year. HSBC said its credit costs this year should be anywhere between US$8bn and US$13bn, wider than the US$7bn–$12bn range it estimated three months ago. It has already taken US$6.9bn of those costs in the first half - meaning it has taken somewhere between 86% of its expected credit loss and barely half.

Banks said they were working off a number of scenarios, including many far worse than their base cases. JP Morgan said it used five scenarios, and had weighted more to the gloomy ones in its second-quarter numbers.

As well as economic prospects by country, banks need to assess the quality of their loan book – far higher provisions are needed for unsecured loans, including credit cards, than for mortgages, for example. For corporate loans, bigger provisions are needed for trouble spots like airlines, retail, energy and hospitality.

Accounting rules also differ, and US banks began using CECL rules at the start of the year, forcing them to provision for losses that are expected during the lifetimes of loans.

Government support programmes, such as payment holidays, may reduce defaults but are also delaying visibility on the ultimate problem for banks – and also vary widely by country.

"SAFER" LOAN BOOK?

And while there is criticism that some eurozone banks have not provisioned enough and could need higher top-ups in the future, some bankers said it reflects "safer" balance sheets. Those assets produce lower returns in the good times, but less trouble in downturns. The eurozone banks broadly have less credit card and other unsecured loan exposure, less exposure to energy and oil sectors, and more to residential mortgages.

"So when a crisis comes it is logical US banks take more provisions,” one European bank chief said.

Santander's credit cost of €3.1bn (US$3.7bn) for the second quarter was up 46% from a year earlier – but not the multiples seen at most rivals. BNP Paribas' cost of risk was €1.4bn in the second quarter, up from €621m a year ago.

Deutsche Bank has been criticised for not taking big enough provisions after setting aside €761m in the second quarter, although that is more than four times its €161m provision a year earlier and up from €506m the previous quarter. It said that reflects its more conservative lending book.

"While the current environment is unprecedented, our historical performance has consistently demonstrated a low loss rate and conservative reserving assumptions," Deutsche CEO Christian Sewing told analysts.

Additional reporting by Christopher Spink