There has been a significant shift to trading bonds electronically rather than over the phone since the coronavirus crisis and working from home, which many bankers regard as long overdue and may herald a structural change.

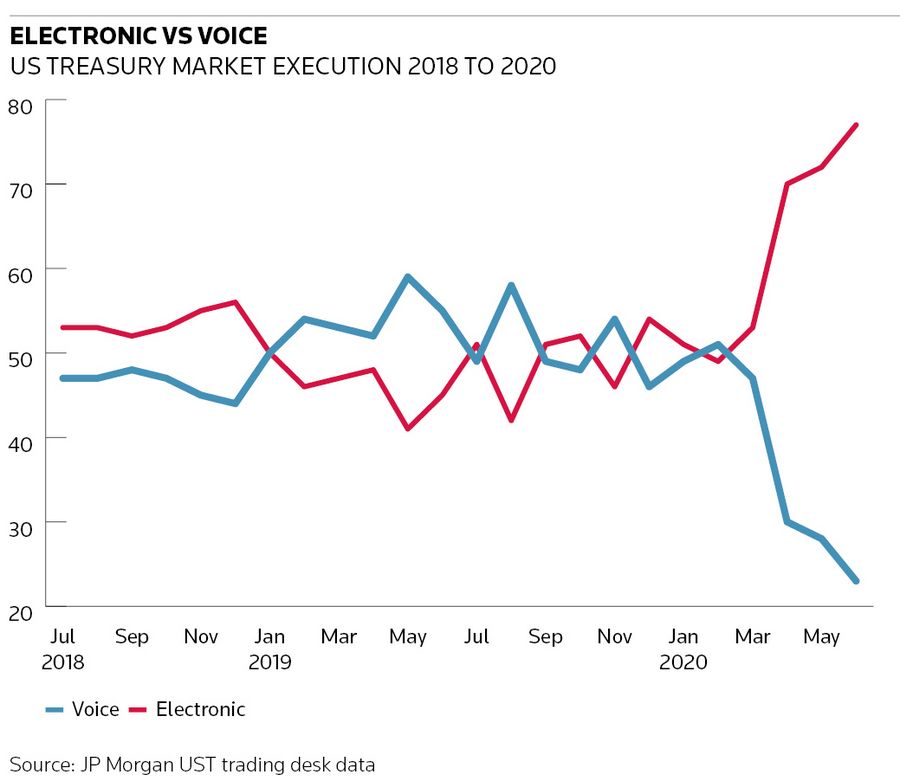

A report by JP Morgan said electronic execution in June accounted for about 77% of dealer-to-client trading in the US Treasury market, up from around 50% before the coronavirus crisis and lockdown.

That is a huge shift in the most active and liquid bond market. In the previous two years, trading was roughly evenly split between electronic and phone orders. In January and February of this year electronic trading still accounted for about half of the US Treasury market, but that jumped to 70% in April and rose further in the next two months, according to data from JP Morgan's US Treasury trading desk.

There has been a similar shift in other parts of fixed income trading, including credit, where the level of electronic trading lagged behind other areas.

"Working from home was definitely a factor, and so was the underlying volatility in the market. The fact they occurred on top of each other exacerbated the effect," said Graham Cox, co-global head of UBS Bond Port.

"It's almost a bit like a jump-start the market needed, particularly in the credit space, which has been lagging the more liquid markets like Treasuries, FX and equities," Cox told IFR.

SYSTEMATIC CHANGE

Trading in the interdealer market for benchmark government bonds had already shifted to mostly electronic trading, similar to what previously happened in FX and equities. In those markets, almost all trading is done electronically.

But large parts of fixed income have been far slower to move, due to greater heterogeneity and complexity of many securities, which can also make them illiquid.

Significantly, the shift in dealer-to-client trading seen in recent months has been apparent across all clients in the US Treasury market, the JP Morgan report said.

"The electronification trend transcends client type, with asset managers, banks and broker dealers, as well as hedge funds, all displaying growth in low-touch execution since the onset of Covid-19," said the report to clients.

"With this in mind, it may be appropriate to question whether the recent market conditions have prompted or catalysed a systematic change in how investors trade USTs."

FIRM PRICES

Part of the reason for the shift was because traders at home wanted to transact based on prices quoted on a screen.

As volatility rose and liquidity reduced, bid/offer spreads widened, quoted prices became stale, and it became inefficient to call several dealers for a price.

An increase in high-frequency trading in the past decade is likely to have added to the illiquid conditions as they can reduce activity during times of stress.

That left traders on the hunt for firm prices. "These firm prices were often found through electronic channels," the JP Morgan report said.

Historically, more heavily traded on-the-run bonds were likely to be executed on electronic platforms while voice execution dominated for less traded, or off-the-run securities.

JP Morgan said the off-the-run Treasury market had shifted to more electronic trading since the Covid-19 crisis.

The report said orders of more than US$100m and deep off-the-run tickets still showed a preference for high-touch execution, with 68% conducted via voice.

UBS Bond Port volumes hit a record in the second quarter and traded volume on the platform was up 153% from a year ago. The number of trades was up 94% and trades worth US$1m or more were up 210%.

Cox said the trend seen since mid-March had continued.

"There has definitely been a cultural shift towards the platforms. You can often see that drift off, but it has proved both on Bond Port and more broadly that there's been significant stickiness within the electronic space," he said.

Bond Port is a liquidity network in the fixed income market. It provides firm pricing in more than 40,000 securities, covering credit, government bonds and emerging markets. It has 2,500 clients, including fixed income venues, traditional dealers and alternative providers.

"There may have been some people who never had any interest in electronic trading and refused to do it, but were forced to do it and thought: 'hang on, this is actually good'," Cox said.

NOT SO FAST...

The shift to electronic trading is broadly welcomed as cutting trading costs, improving transparency and broadening market access. But regulators remain watchful for negative side-effects, and it could also be mixed news for banks.

Firms have spent heavily on platforms and whether that pays off can be a scale game, but margins are typically squeezed by electronic trading, so there is a risk banks cannibalise some of their income.

The Bank for International Settlements said in a 2016 report that regulators need to watch the impact of the electronification of fixed income markets.

"The rise of electronic trading is creating efficiencies for many market participants, improving market quality in normal times, lowering transaction costs and reducing market segmentation, while at the same time posing challenges to some participants," the BIS report said.

But the BIS said it was not appropriate for all securities, particularly for illiquid securities where there are higher risks from information leakage.