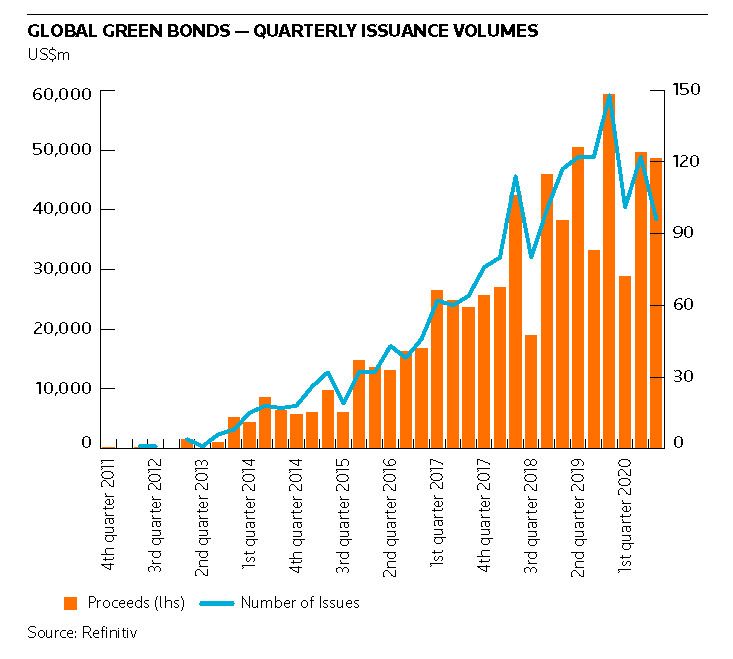

Environmental, social and corporate governance bond issuance shifted up a gear last week as several European corporates made their debuts in the format to take advantage of investors' surging demand for such assets.

Four corporates new to the ESG sector announced deals across both the euro and sterling markets, including Burberry, which is seeking to issue its first bonds of any kind.

The fashion brand is expected to make a sustainable bond issue this week with its deal highlighting the growing importance of ESG debt to corporates' funding strategies.

The three other debut ESG issuers – French telecoms group Orange and healthcare-related REITs Assura and Icade Sante – all printed their deals last week with pricing at very tight levels.

A number of issuers across the bond market have made their first splash in the ESG sector since the post-summer reopening of markets, including the German sovereign, Spain's Banco Sabadell and Daimler, which at the start of September became the first German vehicle maker to issue green bonds.

That momentum continued through to last week as a buoyant market encouraged more issuers to hit the screens.

"The stars have aligned for new sustainable debt issuances. The immediate mindset of treasurers in Q2 was one of survival – this often superseded thoughts around longer-term environmental projects. But as conditions normalise they are encouraged by the talk around 'build back better' and the green recovery," said Arthur Krebbers, head of sustainable finance, corporates at NatWest Markets.

"Also, there is growing evidence of the economic impact. If you can make a 5bp or 10bp saving and attract a broader range of investors, this helps counterweigh the additional preparation time and costs involved."

The new supply is being welcomed by investors, especially those with ESG mandates, as it expands the amount of assets available to them. This has been particularly clear in the sterling market, which both Burberry and Assura have targeted.

"Having been a more prevalent trend in the euro market in recent years, which we actively participated in, we very much welcome the growth in this segment of the sterling market," said Euan McNeil, co-manager of the Aegon Ethical Corporate Bond Fund.

"The fundamental analysis we carry out for all our credit work has always incorporated these ESG considerations, but it is certainly heartening to see issuers embrace and acknowledge these issues more regularly."

SUSTAINABILITY IN FASHION

Burberry signalled its landmark trade on Wednesday, announcing the five-year benchmark sustainable bond offering, which is scheduled to be priced on September 14.

It will also become the first luxury goods firm to issue sustainable bonds.

"There is certainly an increased uptake of the sustainability theme in the fashion industry. Last year you had Prada signing a sustainability loan and also the UN Alliance for Sustainable Fashion was launched," said Krebbers.

Use of proceeds from the Burberry deal will focus on the company's procurement of cotton and other environmental projects.

With questions around the working practices of some fashion retailers, such as Boohoo, investors are likely to take comfort from Sustainalytics' focus on Burberry's human rights record and its health and safety policies as part of its second-party opinion.

If last week's deals are anything to go by, Burberry's offering should prove a big success.

For example, Orange, which also opted for a sustainable bond issue in order to target both environmental and social projects, priced an offering that came through fair value.

The €500m of no-grow 0.125% September 2029 notes were priced at 45bp over swaps with a book of about €2.9bn. Leads BBVA, Credit Agricole, Credit Suisse, HSBC, ING and Natixis placed fair value from 53bp to 55bp.

"The investor response to green and sustainable corporate debt, especially in a post-Covid world, is getting substantially stronger," said Atul Sodhi, global head of DCM at Credit Agricole.

"This was an awesome result for Orange. We had very strong books and a very strong response from the sustainable investor base."

Under Orange's framework, it can allocate proceeds to projects that fall within the categories of digital inclusion, social inclusion, energy efficiency, renewable energy, circular economy or pollution prevention and control.

At the end of 2019 it published its five-year plan, aiming to change its operating model and make commitments to both the planet and "digital equality".

"Following this step change, Orange decided to also align its financing strategy with these commitments, and with its CSR policy," said a spokesman at the company.

"This is why we issued our inaugural sustainability bond, supporting both Orange's social and environmental commitments."

BUILDING SOCIAL

A pair of healthcare REITs also targeted ESG issuance last week, each with social bonds.

Assura brought the first sterling ESG-related deal issued since June, pricing £300m of 1.5% September 2030 bonds at 128bp over mid-Gilts, 7bp through fair value.

In euros, meanwhile, Icade Sante raised €600m with a 1.375% September 2030 note issue, similarly landing the bonds inside fair value, at 155bp over swaps.

Proceeds from both bond offerings will go towards acquiring, developing and expanding access to essential health services.

Although the point could be argued that the use of proceeds varies little from how these issuers would deploy the money raised from a conventional bond issue, bankers believe that there is value in adding a social label.

"While you can definitely argue that Assura is an 'intrinsically social' company, impact investors do tend to see added value in such firms issuing under a social debt framework," said Krebbers.

Not only does adding a social label provide greater rigour in terms of impact reporting and external scrutiny, it also allows investors to track the money raised from the bonds to specific assets and projects.

In addition, it ensures eligibility for a wider range of investment portfolios, such as those that track particular ESG indices, and it makes for a good anchor holding that investors can communicate to their stakeholders, more so than a conventional bond offering, he said.

There was debut ESG issuance in other markets too last week. In the US high-grade market, Johnson Controls, which makes fire protection, HVAC systems, and security equipment for buildings, priced its first green bond issue, US$625m of 10-year notes.

And in the emerging markets Saudi Electricity became the first issuer of green sukuk or conventional bonds from the kingdom, Brazilian pulp and paper producer Suzano sold the first sustainability-linked bonds from an emerging markets issuer, and Chinese gas distributor ENN Energy Holdings sold its first green bonds.