US residential mortgage-backed issuers are making a year-end push, bringing supply to a primary market where investors remain hungry for this type of debt amid an upbeat outlook for the housing sector heading into 2021.

Five issuers - Freddie Mac, loanDepot, New Residential Investment, Bellemeade, Chimera Investment - have already raised US$2.9bn in the RMBS sector this week, putting it on track for the asset class's busiest week since October, IFR data show.

And on Friday, Angel Oak is adding to that supply as it prepares to price a US$249m seasoned non-QM offering, AOMT 2020-R1, which is being led by Nomura and Morgan Stanley.

It comes on the heel of blockbuster demand for a $359m MFA Financial's non-QM issue priced on December 4, which was 10-11 times oversubscribed across the capital stack.

"It shows how much confidence investors have in the housing market," said Caroline Chen, senior research analyst at Income Research and Management.

The Angel Oak deal commanded strong demand but it fell short of the robust level seen on the MFA offering, likely because it was one of the last deals of the year, a source familiar with the deal said.

Even so, its pricing on its US$197.53m Triple A two-year note cleared at a spread of 75bp over swaps, matching the MFA deal.

Investor optimism has manifested in this week's supply in other parts of RMBS market besides non-QM.

For example, New Residential on Thursday sold a US$300m servicer advance securitization, NRART 202-APT1. It fetched nearly US$1bn in final orders for the senior note, while the rest of the smaller, lower-rated tranches were as much as five times oversubscribed, a source familiar with the deal.

Strong demand helped price progression on the five-part offering, which was jointly led by Barclays and Credit Suisse. The senior US$263.9m Triple A rated "A-T1" note with a 1.98-year WAL cleared at EDSF plus 83bp, which was well inside its IPTs of 95bp-100bp, the source said.

The mortgage fund also priced a US$663m mortgage servicing rights deal, NZES 2020-PLS1, this week.

MAKING A COMEBACK

Investors have steadily returned to RMBS after shunning the sector at the early stage of the pandemic amid fears of a surge in delinquencies and defaults as the labor market soured.

The level of missed mortgage payments and defaults has indeed risen, but with the help of government aid and various forbearance programs, they have shown some signs of leveling off.

Even so, worries persist that they may head up again if the jobs market deteriorates once more and the government fails to approve more assistance.

Against that backdrop, Citigroup is projecting that private-label RMBS supply will jump to US$140bn in 2021. That is close to the US$147bn seen in 2019, and well above US$118bn expected for this year.

Also stoking appetite for RMBS is their relative spread pickup versus other credit sectors and the expectations of further home appreciation due to strong demand for single-family homes, Chen said.

Rising home prices will likely offer assurance to investors that they will recover the balance on a mortgage in the event of a default.

Citigroup forecasts US home values will on average climb by 4.7% next year. And S&P CoreLogic Case-Shiller's 20-metro-area house price index jumped 6.6% from a year ago in September after rising 5.2% in August.

Strong home demand, together with historical low mortgage rates, will likely result in a flood of loans for lenders to securitize in the coming months, bankers and analysts said.

"There is a ton of supply coming given the massive refinancing wave coming," a senior banker said.

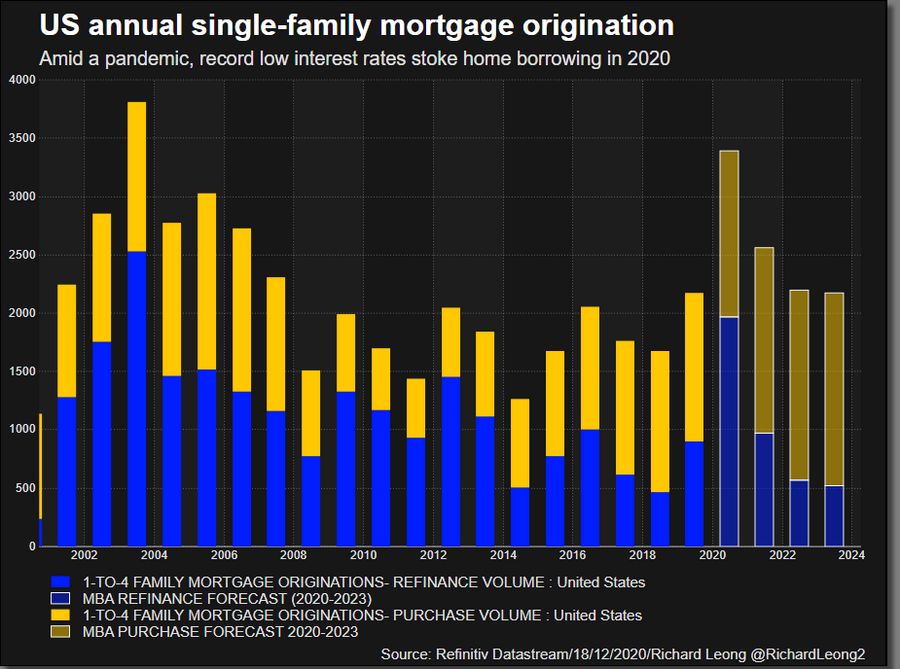

Single-family mortgage refinancing volume is expected to surge to US$1.969trn this year, which would mark its highest level since 2003 when it totaled US$2.53trn and would nearly double the US$1.028trn seen the year before, according to the Mortgage Bankers Association.

Updated story: Updates with Angel Oak deal pricing, adds graphic