Wakako Sato, Refinitiv LPC: Welcome to the ESG roundtable webcast. My name is Wakako Sato and I’m a correspondent at Refinitiv LPC. I’m pleased to moderate the panel discussion today. I would like to express my thanks to sponsors Mizuho Bank, MUFG and Sumitomo Mitsui Banking Corp. The theme of today’s discussion is ESG finance in Japan, a hot topic as evident from the 728 people registered for the webcast.

Within ESG finance, we will focus particularly on loans with our panellists being representatives of borrowers, banks and ratings agencies. I am thrilled that this will be a valuable opportunity to benefit from their insights. I would like to introduce the six panellists.

Yasushi Goto, Mizuho Bank: My name is Yasushi Goto from Mizuho Bank’s syndicated finance department where I have worked since 2012. Sustainable finance in the syndicated loan market is still in its early stages, but companies and investors are showing strong interest, and we would like to continue to help develop the market.

Tomoki Muto, MUFG: I am Tomoki Muto from MUFG. I am responsible for structured finance such as project, including renewable energy projects, aircraft, shipping and trade finance. Additionally, we established a team called the sustainable business office in August last year, which is engaged in green and sustainability-linked loans. At the moment, we have received a great deal of interest from our customers, and like Mr Goto said, we would like to work with you on helping grow the sustainable finance market in Japan.

Tadahiro Kaneko, SMBC: I’m Tadahiro Kaneko from SMBC. I have been managing the sustainable business promotion department since April, which was established as a part of the wholesale banking unit. One of the big pillars of the mission in this department has been to promote sustainable finance.

Other countries are ahead in the loan market expanding its size, but even from Japanese customers the number of enquiries is increasing a lot. I think this will come up in the discussions later but the variety of businesses that are coming for consultation is increasing too, so I would like to promote the business with all of you together.

Atsuko Kajiwara, JCR: I’m Atsuko Kajiwara from the Japan Credit Rating Agency. We started the sustainable finance evaluation business in October 2017 and since then, starting with green bonds and social bonds, we have green loans, positive impact financings with unspecified use of funds, and SLLs. As a ratings agency, our role is to show both financial institutions and companies easy-to-understand measures for promoting ESG finance, so we hope that you will make more use of it.

Naoki Ito, Marubeni: I’m Naoki Ito from Marubeni, a trading company. Our staff in the domestic electric power project department work on the development of renewable energy generation projects. Among the sources of renewable energy, we are focused on offshore wind power, biomass, and small hydropower. We have a company called Mibugawa Electric Power through which we offer one-stop services for small hydropower, from development and operation to maintenance. I am also the president of that company.

In Japan, renewable energy has gained momentum and more and more projects are emerging. Therefore, sustainable finance is something we are very much interested in as a borrower.

Yoshiaki Hamano, NYK Line: I am Yoshiaki Hamano and I am the deputy head of NYK Line’s finance group. I joined NYK’s Yokohama branch in 1993, then moved into sales marketing of cargo on the Latin America shipping route at the headquarters. I was then seconded to the LNG shipping operational management department. After that, I was transferred to the finance department for the first time in 2002. Since then I have moved back and forth between the finance and accounting departments. My most recent move was in April 2017 when I was transferred from the accounting department to the finance department. I have worked on some ESG finance deals in the last three years and have had many opportunities to discuss ESG finance with financial institutions in various situations.

Wakako Sato, Refinitiv LPC: Firstly, I will share some data from Refinitiv LPC to give you a brief introduction to the current status of ESG finance. Then I would like to ask the panellists about the trends and background of what the data show.

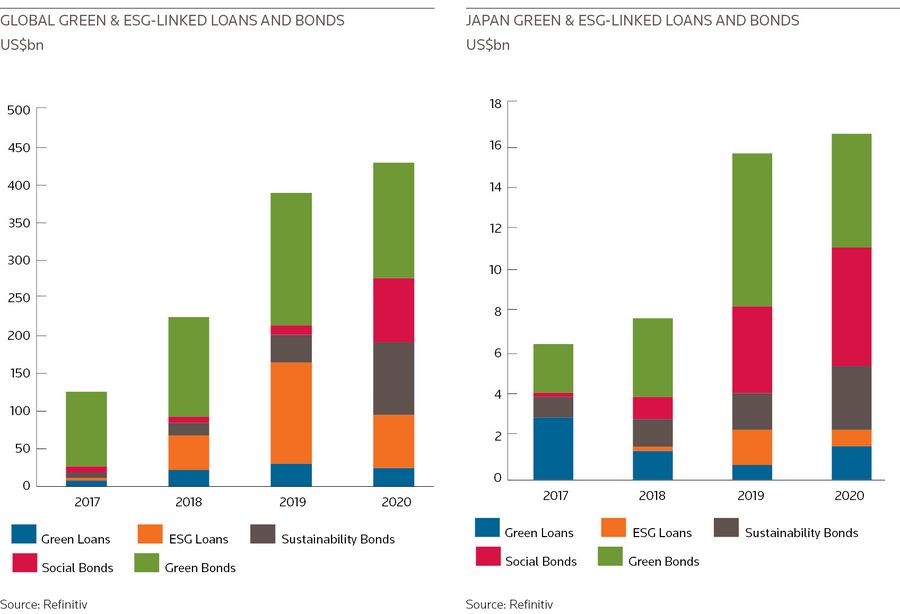

The first slide shows the trends in global ESG-related bonds and loans, which have recorded rapid growth since 2017. the us$431.4bn raised from January to September this year is already around 3.4 times the us$126.7bn transacted in 2017. Bonds are leading the ESG issuance and this year, in addition to green bonds being more prolific, social bonds and sustainability bonds are also expanding rapidly. Even in Japan, although the scale is still small, ESG loans have picked up in recent years in addition to the green loans that were initially leading the market. Domestic issuance in Japan shows the same trend. The market was worth US$6.5bn in 2017 and has expanded 2.5 times to US$16.6bn this year. ESG-related loans account for around US$2.4bn. This is still very small compared to the bond market. Compared to around US$200bn for all domestic syndicated loans, including non-ESG-related projects, ESG still makes up only about 1%, a very small slice.

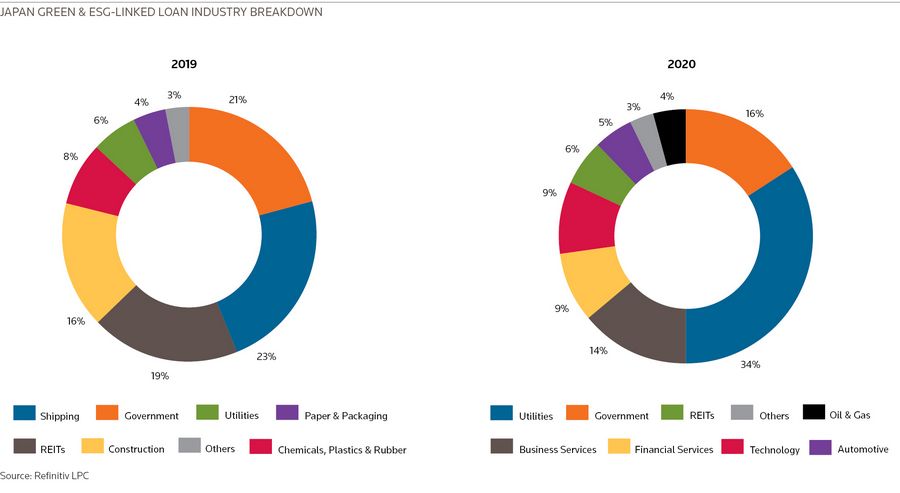

Next, let’s look at the breakdown by industries for Japanese ESG-related loans. Because the market is still very small, individual deals influence the numbers heavily. The utility sector has dominated the dealflow because it includes renewable energy project finance loans such as solar, biomass and wind power. This year we have seen large-scale biomass projects.

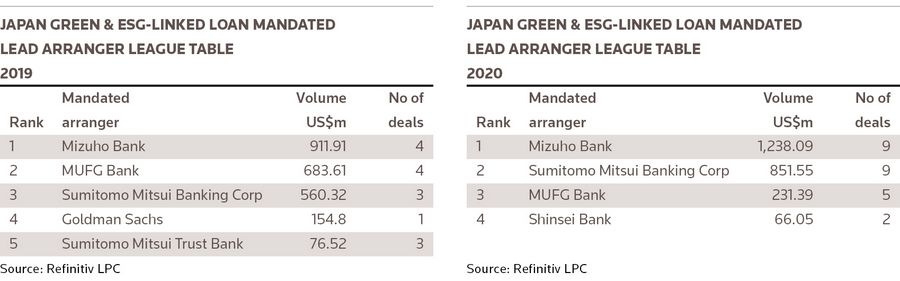

The next slide for mandated lead arranger league tables of Japanese ESG-related loans shows that the Japanese megabanks dominate activity and opportunities for other arrangers are still limited.

Conversely, the league table for all lenders of Japanese ESG-related loans shows a large number of market participants, but only the top 20 are listed. I think that investors make up the majority in the audience today. The number of investors has expanded considerably and it shows the high level of interest.

Finally, several renewable energy projects are ranked in the top 10 Japanese ESG-related loan deals from 2017 to September this year. Shipping line NYK, where one of the panellists is from, is ranked third in the table.

I would like panellists to talk about development of ESG-related loans in Japan in the last few years and about the current status. Mr Goto of Mizuho Bank, could you introduce the types of ESG loans that are available such as green loans and SLLs, etc. and tell us about their characteristics and trends please?

Yasushi Goto, Mizuho Bank: The ESG-related market is developing rapidly overseas, mainly in Europe, and in Japan corporate bonds including green bonds are developing first as you can see from the data. Regarding ESG-related loans, companies with their core businesses or assets, which are green and social, are leading the way in the market. On the other hand, there are restrictions on the use of funds and external certification. Since there are some inconveniences such as cost burden, the focus these days is on sustainability-linked, which is a method to tackle corporate environmental and social issues without limiting the use of funds. It is a loan and has a high level of interest in the market, and syndication has just begun.

In addition, as is the case with our bank, companies are also actively procuring their own unique products as well as deals related to sustainability finance developed by banks. Mizuho also offers unique products called “Mizuho Eco Finance”, which scores the status of corporate efforts in terms of information disclosure regarding environmental considerations based on the evaluation model developed by Mizuho Information Research Institute, to companies that have obtained a certain level of evaluation. This has been well received and the loan amount has increased. The ESG-related loan market is still in its infancy, but we believe that it will develop in the same way as the European market.

Wakako Sato, Refinitiv LPC: Mr Muto, please let me know your opinion on the respective features and development of japan’s ESG-related bond and loan markets. What do you think is the reason the loan market still lags the bond market and is still small?

Tomoki Muto, MUFG: To make a comparison between markets, I think we need to first review the differences in product characteristics of bonds and loans.

For bonds, to some extent, I think the purpose of the funds is restricted in many cases. For loans, depending on the scheme or form of the certification body, it is possible to have multiple uses of funds. With regards to flexibility of the scheme, publicly offered bonds have some restrictions in finance structures, generally with fixed interest rates or bullet maturities. In terms of payment, disbursement is determined to some extent with bonds, but loans can be structured with floating interest rate or margin step-ups or step-downs, amortisation and odd tenors. Loans come with a lot of these kinds of flexibilities.

When it comes to growth in amounts, investor demand probably has the biggest impact. The bond market is still ahead of the curve in ESG investment as demand from investors who invest based on the Principles for Responsible Investment (PRI) has grown explosively. The loan market has not quite matured at this stage and we believe that there is room for expansion. Also, from the perspective of the issuer or the borrower, I think the consequences and merits of investor relations are important. IR merits are high for bonds where terms are publicly disclosed. The number of ESG-related bonds has increased considerably, so from the perspective of the impact and attention of individual deals, I feel that it has settled down a little. But the loan market is still relatively new, so we believe that each deal has a strong effect when disclosed. As you all know, the reason why the expansion of loans is delayed compared to bonds is probably due to the institutional and the principle aspects. For bonds, the Green Bond Principles were established around 2014, the Social Bond Principles in 2016, and the Guidelines for Sustainability Bonds in 2018 – well ahead of loans. The difference in starting points cannot be ignored. Various principles were established in 2018 for loans, which is when the loan market started to grow.

When comparing SLLs and sustainability-linked bonds, it is worth noting that the principles for loans were formulated in March 2019, and that for bonds in June this year. We are also paying attention to how the difference in starting point will affect the growth of SLLs/ SLBs in the future.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@refinitiv.com