A large chunk of interest-rate derivatives trading has migrated to US venues this year following the UK’s withdrawal from the European Union, dealing a blow to the City of London and highlighting the importance for the UK of reaching a post-Brexit agreement on financial regulation with the EU.

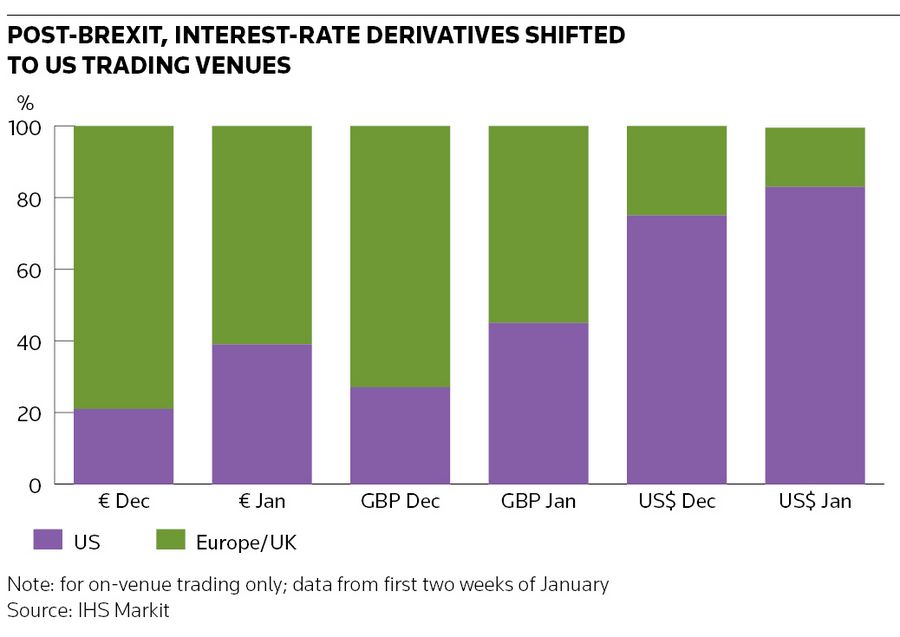

Volumes of euro interest-rate swaps transacted on US-based platforms known as swap execution facilities, or SEFs, jumped from 21% in December to 39% in the first two weeks of January, according to data provider IHS Markit, while sterling swap volumes registered a similar rise. That came amid an equivalent drop in trading volumes on UK and EU-based derivatives trading venues.

The sharp move in activity came in the wake of the UK and EU failing to reach a “mutual equivalence” agreement on cross-border regulation of derivatives trading following the UK’s departure from the trading bloc.

A permanent shift to New York would be particularly damaging for London and that prospect further raises the stakes in negotiations as the UK and EU look to iron out an agreement on financial services in the coming months. But industry experts note it could also harm EU-based companies if the cost of trading derivatives rises as a result of the impasse.

"The market was primarily based in the UK. But the market is global and quite agile – it will shift. This is what we expected to happen with the lack of equivalence," said Kirston Winters, managing director at IHS Markit's MarkitSERV.

"The key thing is liquidity pools are fragmented. The worry participants have is, what are you doing to prices and liquidity if you're fragmenting the market?"

The UK and EU have a virtually identical regulatory framework for derivatives trading, including a requirement for cleared swaps that are sufficiently liquid to be transacted on venues that are broadly similar to US SEFs. But that hasn’t stopped Brexit from throwing sand in the gears of these markets after the transition period for the UK leaving the EU expired at the end of last year.

Not recognising each other’s derivatives trading rules meant that EU-based entities could no longer transact swaps on venues based in the UK – and vice versa – come January 1. Instead, EU and UK-based entities can only trade on local venues or in countries with which equivalence agreements have been struck, such as the US.

Global hub

That is particularly problematic for London, the foremost centre for derivatives trading globally, including the US$495trn interest-rate swap market. Around US$3.7trn in these swaps changed hands daily in the UK, according to a 2019 survey from the Bank for International Settlements. That’s about half the entire market and over 30 times more than France’s share, the most prominent EU country trading these swaps.

So far, at least, the US has been the main beneficiary of the lack of an equivalence deal. Nearly half (45%) of sterling swap trades in January have been traded on US SEFs, according to IHS Markit. US dollar swap transactions also increased, with US SEFs capturing 83% of these markets, up from 75% in December.

"Market participants can easily minimise regulatory risk and access the same liquidity by trading on SEFs," said Nicholas Bean, global head of electronic trading solutions at Bloomberg, which operates derivatives trading venues in London, Continental Europe and the US.

"Whether this is a long-term trend remains to be seen. However, it is likely to persist at least until the EU and UK deem each other's venues equivalent" for the purposes of derivatives trading, he added.

One result of the current standoff over equivalence is that UK-based branches of EU banks have to comply with both sets of rules, not allowing them to trade on venues in either jurisdiction. That means US SEFs are one place where all the major dealers can trade at present.

"Since clients are always looking for the deepest liquidity pools, it’s not a surprise that there has been a migration to SEFs,” said Bhas Nalabothula, head of European interest rate derivatives at Tradeweb, which operates derivatives trading venues in London, Amsterdam and the US.

“If a future equivalence decision allows the liquidity picture on the UK [venue] to match what it had pre-Brexit, it’s very likely we will see a shift back to" the UK, he said.

Limited relief

The UK’s Financial Conduct Authority has provided some limited relief that allowed UK firms trading with EU clients that don’t have access to SEFs to trade on EU venues. But the regulator made clear in a late December statement that an over-arching agreement on mutual equivalence is needed “to avoid disruption for market participants and avoid fragmentation of liquidity”.

London and Brussels are aiming to sign a memorandum of understanding over financial regulation by March, although that does not guarantee that an agreement over mutual equivalence will be reached. In the meantime, there is concern in the City that the EU may try and lure more derivatives trading activity to its shores, as it has with stock-market trading.

"The derivatives trading rules are identical – the UK wrote them with the EU. This is entirely political,” said Winters.