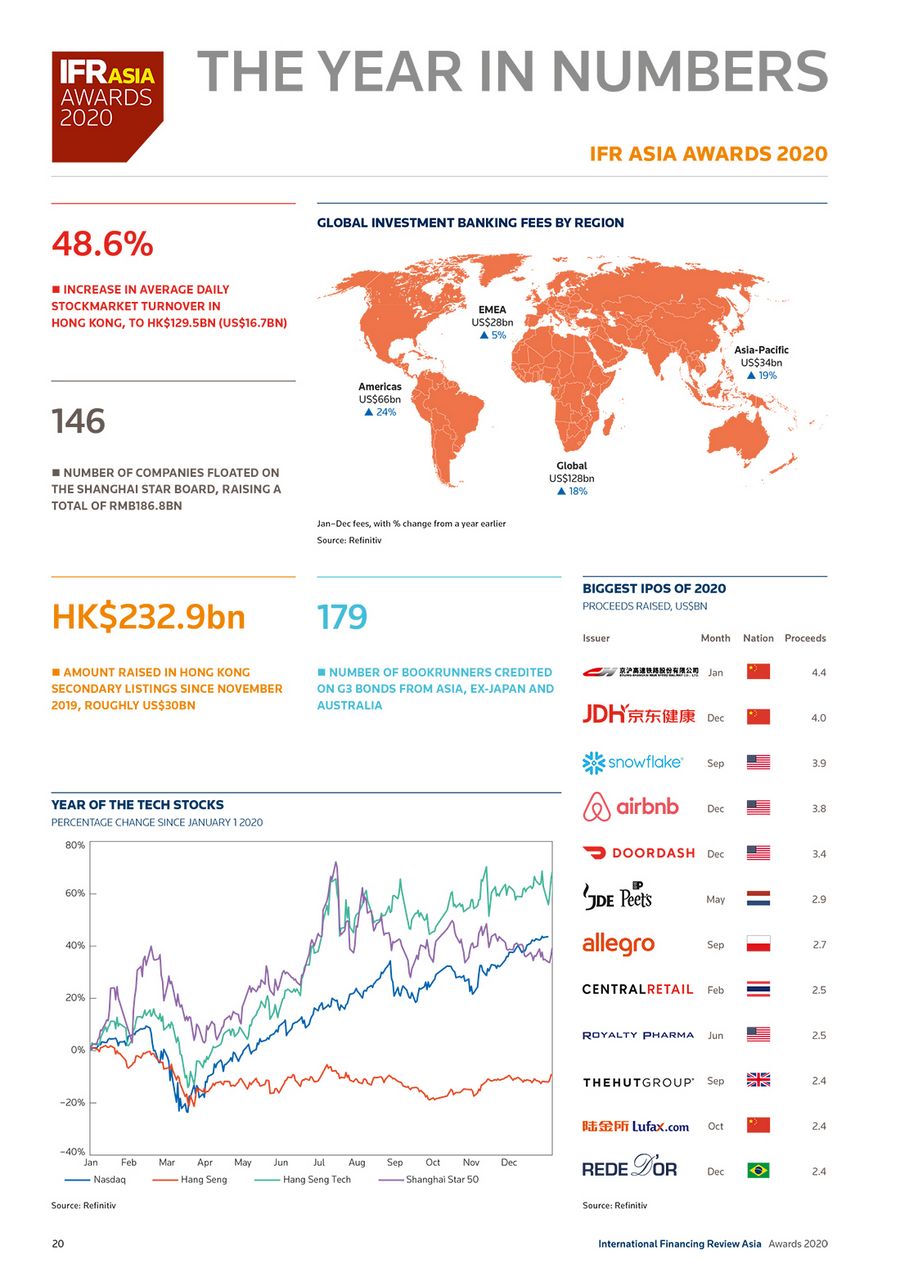

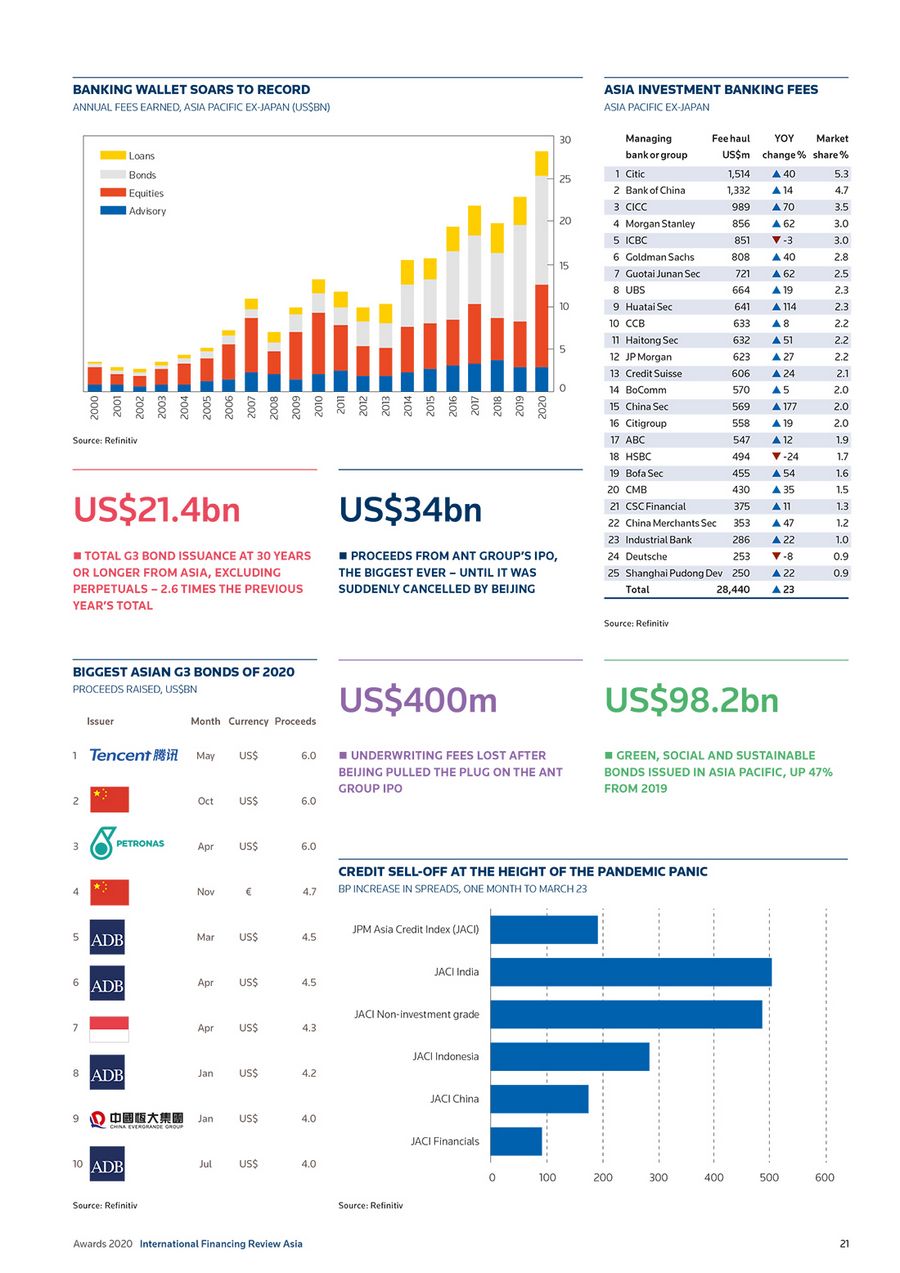

A selection of numbers and charts that illustrate the events of 2020

To see the digital version of this report, please click here

To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

To see the digital version of this report, please click here

To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

Early last year, shortly after banks in Asia first began telling staff to work from home, the regional CEO of a global bank received an unusual request from a junior banker. Would the firm start paying his rent, the young staffer asked, since it now qualified as his main place of work under the Hong Kong securities regulator’s rules. The request was politely declined, but the coronavirus pandemic threw up many more tricky questions as executives swapped boardrooms for kitchen tables and business class flights for Zoom calls. It also triggered a...

Shanghai’s Nasdaq-style board for new-economy listings beat all expectations in 2020, its first full year of operation, and is poised for further growth in 2021. The Shanghai Stock Exchange Science and Technology Innovation Board, better known as the Shanghai Star board, finished 2020 with more than 200 listed companies commanding over Rmb3trn (US$463bn) in market capitalisation. Expectations for the market were high, to be sure. “The Star Market forms part of a broader strategy in the PRC to develop its equities market into one that is fitting...

The grand buildings of the Bank of Japan and Tokyo Station stand as testament to Japan’s embrace of modern ideas at the end of the 19th century. The mastermind behind both structures, Japanese architect Kingo Tatsuno, spent four years studying architectural design at the Royal Academy of Arts in London and is credited as being the first to introduce European-style brick masonry to Japan. The change in architectural style was mirrored in the wider society. The turn of the 20th century marked a period of rapid development for Japan, when the...

To see the digital version of this report, please click here To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

To see the digital version of this report, please click here To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

Ant 1. Tiny insect that can support many times its own weight; 2. Behemoth that folds under pressure from above Barrenjoey The Australian investment bank formerly known as UBS Bitcoin Something to bet on when you’re bored of making electric cars or launching rockets Block leave Holiday spent in your own apartment complex Blue bond A whale-y big deal in sustainable finance Bookbuilding Process of taking orders when a deal is already covered, especially in Chinese US dollar bonds Bookrunner In Hong Kong, anyone who promises an order for a debt or...