The European Union will struggle to force a large-scale migration of euro swaps clearing onto its shores without causing serious harm to its own banks as well as EU regulators’ ability to police these markets, industry experts have warned.

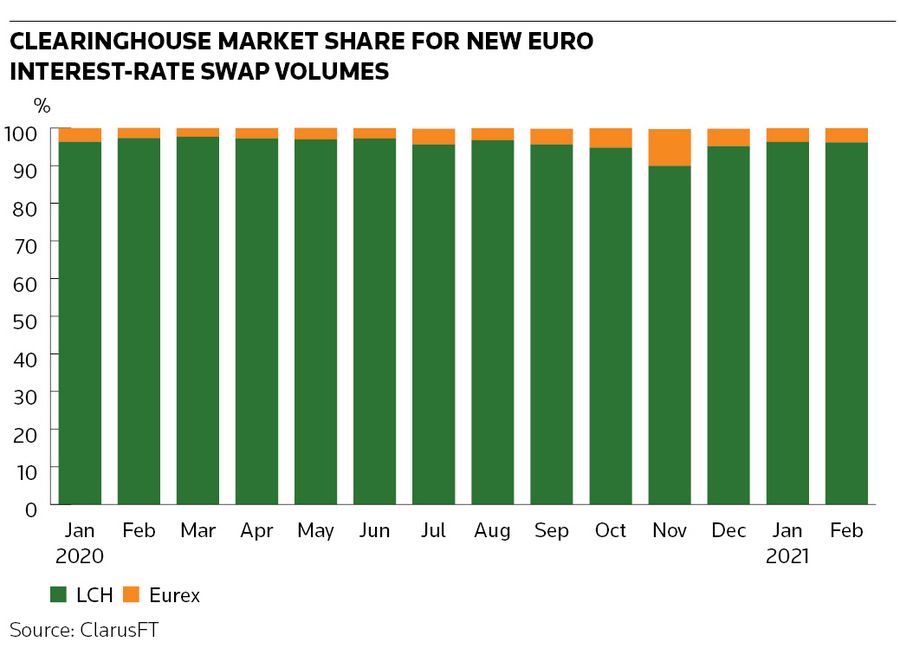

The EU has captured a large chunk of euro interest-rate swaps trading activity this year amid a post-Brexit regulatory impasse with the UK. But there has been no mass movement of euro interest-rate swap clearing out of London, with the UK’s LCH still accounting for roughly 96% of new clearing volumes in January and February, according to data from research and analytics firm ClarusFT.

The stickiness of clearing activity will frustrate EU leaders and underlines the challenges they face in attempting to wrest control of the euro swap market out of London’s grasp.

Roughly three-quarters of euro swaps clearing activity doesn’t involve EU firms, complicating Brussels’ efforts to attract this business. That dynamic also raises the possibility of EU banks and regulators being cut off from the largest global pool of euro swaps clearing if the two sides don’t reach an agreement.

The EU has so far tempered combative rhetoric with pragmatic action, warning the market it must reduce its perceived over-reliance on London while extending regulatory relief for UK clearers until mid-2022. But there is still no clarity over how much of the euro swap market the EU ultimately wants cleared within its borders – or the lengths to which it will go to make that happen.

“There is a huge amount of uncertainty,” said Ulrich Karl, head of clearing services at ISDA. “There seems to be a big political push from the EU to relocate clearing of euro-denominated contracts into the EU. The question is, how far it will go?”

Flashpoint

Central clearing is a dull, but crucial, part of market plumbing designed to minimise the risk of defaults among derivatives traders spilling into the wider financial system. It has also become a flashpoint in post-Brexit negotiations over financial services.

The vast majority of interest-rate swap clearing (about 90%) resides in London at LCH’s SwapClear – a fact that has never sat well with EU leaders keen for greater control over the euro market. (LCH is part of the London Stock Exchange Group, which also owns IFR following LSEG’s acquisition of Refinitiv this year.)

Brexit gave the EU a powerful tool to bring more financial activity within its borders by refusing to recognise the UK’s financial regulatory regime as equivalent. That has borne fruit in areas such as derivatives trading, with the EU significantly increasing its market share in euro swap volumes this year after EU firms were cut off from UK trading venues. Some think this will embolden EU policymakers to take more clearing activity by force too.

The derivatives trading shift "might be perceived at first sight as a ‘home run’ kind of success" for the EU, a senior European banker said.

But EU banks don't share that sense of euphoria. That's because the EU’s land grab in derivatives trading has come at a serious cost to the likes of BNP Paribas, Deutsche Bank and Societe Generale, which haven’t been able to engage in the considerable amount of euro swaps activity still happening on UK venues due to the absence of an equivalence ruling.

Industry experts are concerned a similarly blunt approach to clearing through withdrawing equivalence would inflict even greater damage on these banks by depriving them of access to the largest global pool of derivatives clearing.

A narrower policy preventing EU firms from clearing just euro swaps at UK central counterparties would be similarly self-harming, experts say. That’s because 75% of LCH’s euro swap clearing volumes do not involve an EU-based counterparty and so would probably stay in London out of the reach of EU banks. Such a move could even force EU banks out of the euro swaps business altogether, some bankers say.

It would also harm EU regulators’ ability to monitor these markets as they would no longer have oversight of London-based CCPs.

“Fundamentally we think the de-recognition tool is inappropriate,” said a second senior European banker. “It doesn’t work for dealers, it doesn’t work for our clients. We also don’t think it works for regulators [as] the EU would be voluntarily blinding itself to all the activity going on in global markets outside the EU.”

EU migration

The driving force behind LCH’s continued dominance in swaps clearing is that pooling trades in one venue tends to make clearing much cheaper. Clients can offset positions, lowering the amount of margin they have to post, while banks don’t have to set aside as much capital against their exposures if they’re mainly sitting in one place.

Breaking up the euro swap clearing market would increase margin requirements for banks by 16% to 24% on average and bank's capital requirements by 65%, ISDA said in a 2017 letter to the European Commission.

Eurex Clearing, the EU’s main euro swap clearer, has picked up business in recent years despite these head winds. It has created incentive schemes to encourage activity to migrate that have helped spur some notable switches from LCH, including Germany’s DekaBank in 2019 and French public investment bank Bpifrance late last year.

A Eurex spokesperson said its market share of new euro swap clearing volumes rose above 9% in March, while public data show its share in terms of outstanding positions was 16% (rising to just over 20% when including all euro interest-rate derivatives).

Bankers say Eurex is most popular with clients holding predominantly euro exposures, with the exchange’s leading position in Bund futures allowing cross-margining to lower collateral requirements for clients.

“Our objective has been to build up a sizable euro-clearing offering within the EU via a market-driven, voluntary approach,” said Matthias Graulich, member of the executive board at Eurex Clearing.

Excessive exposures

For many, though, Eurex remains the back-up option for euro swap clearing. Even as it has grown its client accounts to 420 (a little under half the number at LCH’s SwapClear), around three-quarters of these are inactive, sources say.

Bankers say non-EU clients have little interest in switching positions, particularly if they trade swaps across multiple currencies given their ability to cross-margin at LCH. Nearly 99% of Eurex's outstanding clearing volume is in euros.

“The challenge for the EU is how are they going to force an asset manager in the US clearing with a non-EU [bank] to clear in Eurex,” said a senior US banker.

The EU, for its part, is far from satisfied that enough euro clearing is happening within its borders. European Commissioner Mairead McGuinness told a Futures Industry Association conference recently that the bloc’s temporary relief for UK CCPs “is not a free pass”.

“Rather, it should be used by market participants to reduce their excessive derivative exposures to UK-based CCPs,” she said.

Controversial proposal

The French Banking Federation published a paper that provided one answer: the EU passing legislation forcing euro swap clearing activity into the EU. That brought a sharp rebuke from Bank of England Governor Andrew Bailey, who called such measures "highly controversial" and of "dubious legality".

The paper suggested less aggressive measures too, such as getting EU public entities to clear through Eurex to help build momentum. Bankers say the EU must also engage with clients to find ways to ease any transition.

Many are hopeful a damaging battle over clearing can be avoided if a decent chunk of euro activity gradually moves to the EU, combined with reinforced regulatory oversight of the majority remaining in London. But if Brexit has shown anything, it's that politics – in particular notions of sovereignty – can often trump economics.

“The question for the Commission is do you gain more through people bringing swaps clearing into Europe than you lose by stopping EU banks accessing CCPs in London?" said Kirston Winters, managing director at post-trade firm MarkitSERV.