When Nicolas Sarkozy and Angela Merkel met for a weekend summit at the French seaside resort of Deauville in October 2010, Europe was in deep crisis. Greece was just five months into its first bailout, and Ireland was days from becoming the second country to seek help. Fear was rife that it was the beginning of a crisis that would drag in much bigger countries and maybe even bring down the euro.

The French and German leaders realised they were unprepared for a big flare-up. In their haste to push through the Greek rescue and avoid painful treaty renegotiations, the European Financial Stability Facility – the body charged with funding any bailouts – had been set up to automatically expire after two years. Both agreed that a new, permanent rescue vehicle would be needed.

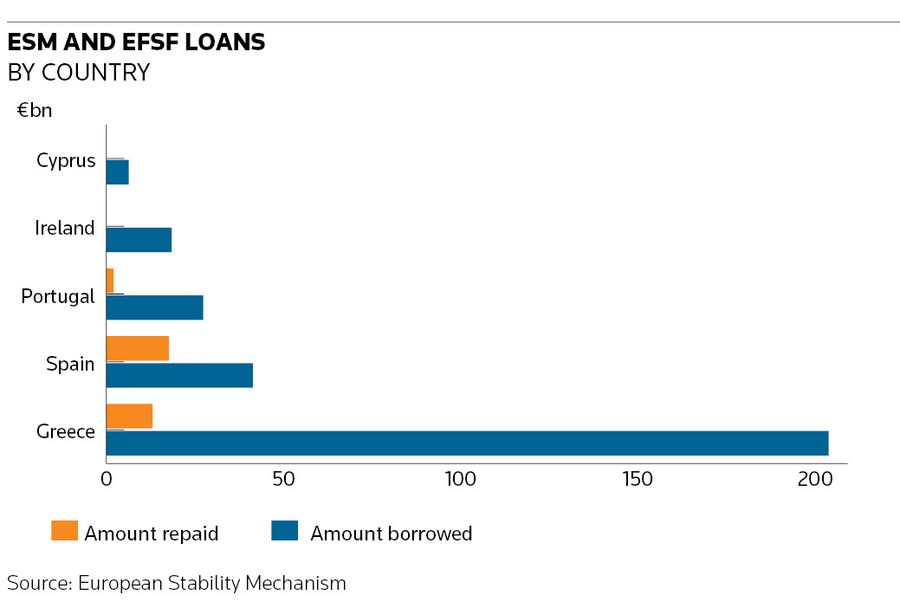

And so the European Stability Mechanism was born. A decade on, it still bears the scars of the European sovereign debt crisis. Its job is to continue financing the €260bn still owed by the five countries that were bailed out. While Spain is due to pay back the €40bn it borrowed before the end of the decade, the €200bn lent to Greece in three rescue deals isn't due to be paid off until 2070.

The 10-year anniversary of the ESM’s conception also coincides with a big change in its remit. Later this year, the Luxembourg-based institution will take on new responsibilities linked to bank resolution and economic monitoring. The transformation will leave it looking more like a European version of the International Monetary Fund with a vastly expanded mandate.

“This feels like something really significant because it’s reopening the treaty,” said one official. The new treaty was signed in January and will enter into force once ratified by the 19 parliaments of euro-member countries. “In a sense, it’s a real new chapter and you will see an upgraded ESM.”

By popular demand

The biggest change will see it become a backstop to the Single Resolution Board, the body charged with the orderly resolution of failing banks. The ESM will raise money on its behalf as and when needed. Until now, the SRB’s resources have been limited to bank contributions. Access to the debt markets through the ESM will increase its available liquidity tenfold to €68bn.

Such increased firepower will help avoid situations like the forced fire sale of Banco Popular, which was sold off overnight to Santander in June 2017 for just €1 – in part because the SRB could not muster the liquidity to allow Banco Popular to open branches the next day. Santander was the only bidder and looks set to make huge gains. Investors allege the sale was flawed and are suing the SRB for compensation.

Billions of euros could be needed at very short notice in such situations. But the ESM has already proven itself adept in crisis management. In 2012, as part of the Spanish bailout, it issued bonds directly to banks, which then used them as collateral to generate liquidity. The ESM-SRB alliance has been brought forward due to the pandemic, amid concern that the economic fallout could destabilise some banks.

The ESM will also take on new monitoring powers. While the old bailout programmes will not be affected by the changes, any new rescue packages will be designed, negotiated and monitored by the ESM in collaboration with the European Commission. It will also monitor economic developments in all 19 euro-member countries on an ongoing basis.

Pandemic response

Having been born out of crisis, the ESM clearly saw the pandemic as an opportunity to re-establish itself as a vital tool – but results have been mixed. Just weeks into the pandemic, it launched €240bn of pandemic crisis support loans for countries in need. Not a single euro has been drawn, although officials point out that the existence of the backstop may have helped prevent a flare-up in the debt crisis.

Klaus Regling, the managing director of the ESM, also waded into the debate around the EU’s response to the coronavirus crisis, particularly around the question of how the bloc would fund its massive pandemic response programme. With a decade of experience of selling mutualised bonds – the ESM is a standalone body backed by €80bn of capital provided by eurozone member countries – it perhaps saw itself as the natural body to issue such debt.

“We know how long it takes from the moment a new institution is created until it's possible to issue debt,” he said in a newspaper interview at the time. “In the short run, one should use existing institutions that have experience in doing all this, with the existing instruments and they can be adapted to some extent. In the longer run other possibilities exist.”

The idea of the ESM overseeing the financing of the EU pandemic response was met with opposition by some countries – not least Italy, which was concerned that ESM involvement would make any funds look like a bailout. But in truth, the ESM was never a good fit: it represents only the 19 eurozone countries, while the pandemic response will go to all 27 members of the wider EU.

“I think if you look at this crisis, it is very different,” said one banker. “This is about the EU acting as a whole, which means you can't effectively use the ESM to the same extent. So with that in mind, I think politicians clearly opted for the EU as the preferred institution to proceed with the response given the nature of the crisis, and we've seen that it works extremely well.”

The financing of the €750bn Next Generation EU and €100bn SURE pandemic response programmes will instead fall to what was once a small team in the European Commission. Several ESM employees have been seconded to the unit, including its head of funding Siegfried Ruhl, prompting some to worry whether the EC funding programme might become a brain drain for the ESM.

Big issuer

Regardless, the ESM is set to remain a big debt issuer. Last year, it sold around €30bn of bonds – two-thirds linked to old EFSF loans and a third to ESM loans – and looks set to be a central part of the capital markets for some time yet. While Cyprus, Ireland and Portugal are set to pay off their loans by 2040, the Greek loans will need financing for decades to come.

The two funding European agencies have already begun working together. The ESM, European Commission and European Investment Bank did a joint presentation to investors last October just before the EU's first bond deal. The trio is informally known as the One Trillion Club. Ideas are exchanged between all three, and they communicate on deal timing to avoid conflicts.

Officials believe that, far from being rival agencies, the ESM and the EU could actually be mutually beneficial. While the bonds have slight differences – ESM and EFSF bonds are backed by paid-in capital and the fixed calendar of issuance makes fair-value calculations easier – they are generally viewed on an equal par by investors and benefit from that status.

Traders often step in to arbitrage price differentials, which has helped bring yields down generally. Bankers believe the €850bn of supply from the EU will solidify the EU’s status as a safe asset, which will in turn benefit the ESM.

“I think it will entice investors to dramatically increase their exposure to the European Union and the ESM, simply because it is going to become the main supplier of paper in the supranational sector,” said a second banker. “The levels of supply are going to be similar to the amounts that we see from the largest sovereigns such as France and Germany.”