The shift by the interdealer market for US dollar interest-rate swaps to SOFR from late July should mark a crucial step in global efforts to eradicate Libor, bankers say, as regulators look to give fresh impetus to what has so far been a sluggish transition away from the controversial lending rate.

The Commodity Futures Trading Commission has recommended the secured overnight financing rate, regulators’ preferred replacement for US dollar Libor, should replace Libor in interdealer US dollar linear interest-rate swap trades from July 26 onwards. That comes ahead of a regulatory deadline for banks to stop using US dollar Libor in new contracts from the end of this year.

Bankers say the “SOFR First” guidelines, which seek to emulate a similar initiative in the UK, should increase volumes in SOFR and reduce trading costs, helping to draw in a wider range of participants.

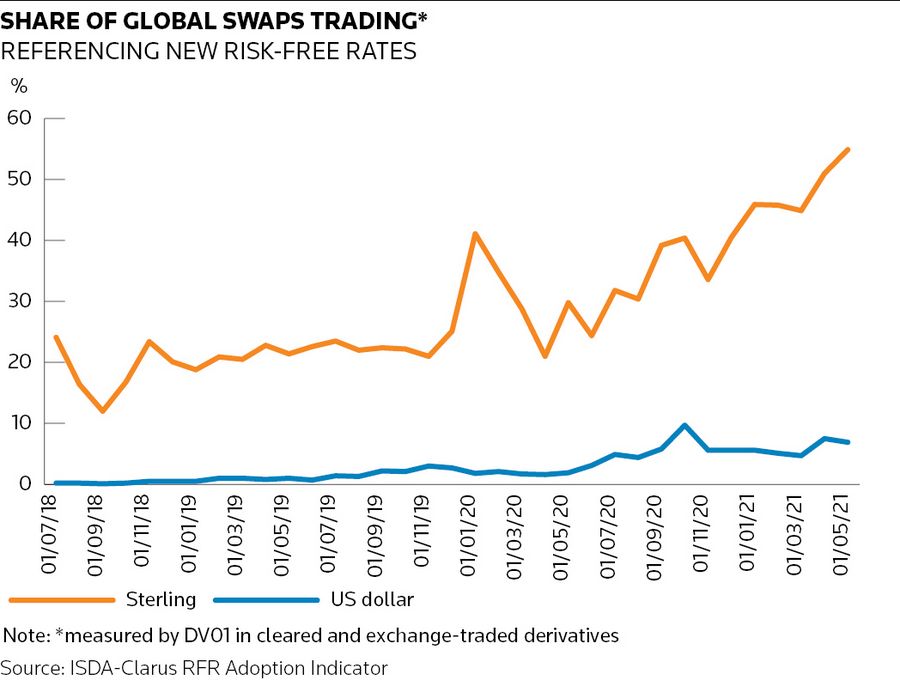

That would represent a much-needed shot in the arm for the US dollar Libor transition given that interest-rate swaps tied to SOFR made up less than 2% of US trading volumes in the first few months of the year, according to data from IHS Markit, compared with over half of sterling swap trading volumes being linked to the UK's sterling overnight index average, or Sonia.

“SOFR First should be hugely important in helping drive the transition away from Libor between now and year-end,” said Tyler Wellensiek, global head of rates market structure and business strategy at Barclays. “We don’t want everyone turning on a dime. This is a sequential, gradual thing where liquidity and activity in SOFR will build in a smooth, orderly fashion.”

Eliminating Libor from financial markets is an enormous undertaking. The amount of contracts tied to US dollar Libor has actually increased by 12% since 2016 to US$223trn, according to a recent industry report. Interest-rate swaps represented the largest portion of that Libor-linked exposure, with US$81trn outstanding.

The centre of gravity in US swap markets is expected to begin to shift gradually when interdealer brokers replace Libor with SOFR in late July, given that dealers trading on these platforms account for a “substantially large share" of activity in these markets, according to the CFTC.

The initiative should provide enhanced data around SOFR-linked contracts for the wider market too, helping to get “people to think in SOFR", said Wellensiek. It should also allow the Alternative Reference Rates Committee, a group of private-sector firms working with the US Federal Reserve, to approve the use of term SOFR rates – a potentially critical development in encouraging more widespread adoption of SOFR.

That would remove “the last obstacle to using SOFR as a replacement reference rate”, Randal Quarles, vice-chair for supervision at the Federal Reserve Board and chair of the Financial Stability Board, said in a statement.

Friction costs

Bankers say increased trading and liquidity in SOFR should lower transaction costs in these contracts, a current point of contention for clients. Banks still hedge SOFR trades back to Libor in the interdealer market at present, increasing friction costs.

“When the hedging instrument is now SOFR, our hope is that we can compress and eventually eliminate those costs,” said Wellensiek.

Bart Sokol, managing director in US interest rate swap trading at Barclays, said there had been a pick-up in SOFR quotes in the broker market since the CFTC’s announcement, in a sign the transition is starting.

“The dealer community is ready for this next step. There has already been some trading in SOFR and bid-offer has come down. Everyone knows the deadline for no new Libor from next year. The market just needed to get a little nudge,” he said.

Traders say most regular swaps users should be happy to shift to SOFR as liquidity builds in this market over the coming months. But there is still a good deal of uncertainty over the path forward for less frequent participants in these markets, such as many corporate treasurers.

These users have had to contend with a loan market that has proved even more hesitant to drop Libor, raising concerns over a potential mismatch between their borrowings and the swaps that hedge them.

SOFR's lack of credit sensitivity has been a particular sticking point for some participants. That has caused a number of alternative rates to spring up, even though SOFR is ultimately expected to become the dominant benchmark in US markets.

“The market’s adoption of SOFR has been much slower than anticipated for two main reasons: there is no forward-looking term rate in SOFR, and it lacks a bank credit component,” said Pradeep Bhatia, chief executive of financial technology firm Derivative Path.

SOFR “will undoubtedly have a dominant role in the derivatives market. But other indices such as Prime, [Bloomberg’s] BSBY and Ameribor are all vying for some role in lending and hedging markets in the future as well”, he added.