A £3bn raft of social housing sustainability bonds and private placements this year signals a wider take-off in UK ESG debt when the first green Gilts are launched in September.

In the third inaugural housing association sustainability bond offering in as many weeks, Metropolitan Housing issued a 15-year deal on Wednesday that combines green and social use of proceeds. This follows 30 and 40-year debuts from Anchor Hanover and Flagship Housing. More are set to follow, potentially including the first HA sustainability-linked bond as well as foreign currency issues.

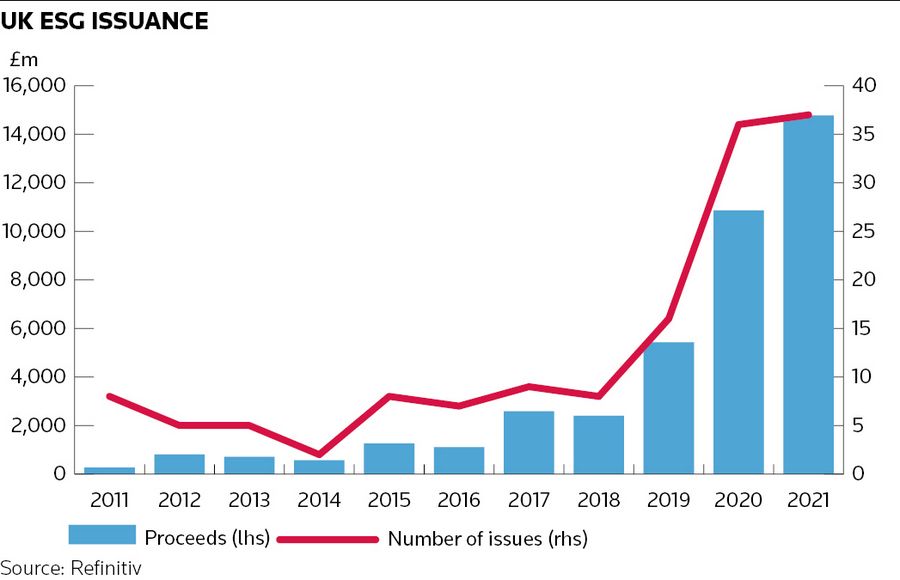

Some £2.5bn of HA ESG bonds have been issued in 2021, according to IFR data. This represents 80% of the sector’s public issuance since January, according to NatWest Markets, and a third of total UK ESG volume.

The series began in January 2020 with a pioneering 15-year from Clarion Housing. But this year Aster Group, Beyond Housing, Notting Hill Genesis, PA Housing and Paradigm Homes have all got sustainability bonds away as labelled debt has rapidly become the sector norm – expanding a previously narrow investor base and improving pricing.

The total for 2021 rises to £3bn when a further £500m of HA ESG private placements are included. These include UK and US offerings for Believe Housing and Origin Housing, respectively.

Moreover, the aggregator bLEND Funding recently converted all its nearly £1bn of bonds to social bonds. It may also establish a sustainable financing framework.

Shining light

“The social housing sector has become the shining light of ESG issuance in the UK,” said Matt Thomas, head of UK corporate DCM at Barclays. “There's a demand from investors to buy product that they can very safely put into their ESG portfolios. This sector is perfectly set up to provide them with what they want – these are quality businesses doing good things in society.”

HAs are especially ESG-friendly. They provide affordable homes and support services to lower-income residents, while the UK Regulator of Social Housing now requires them to raise the energy efficiency of all properties.

“It's a sector that fits hand in glove with both the social and environmental tendencies of sustainable finance,” said Arthur Krebbers, head of sustainable finance for corporates at NatWest Markets.

UK HAs are one of the first social housing sectors in Europe to have agreed a sector-wide sustainability reporting standard with investors. Some, including last week’s new entrant Metropolitan, have also gained "certified sustainable housing" labels.

“The ESG commitment has gone past the point of no return. That's what a housing association bond looks like now, and the exception will be those who for whatever reason don't label theirs,” said Thomas.

Building out

Besides a strong HA ESG pipeline in the run-up to the UK hosting November’s COP 26 climate conference, the country’s first sovereign green bonds should help to expand ESG debt supply from other sectors.

Although the UK has lagged G7 peers France, Germany and Italy in entering the product, HM Treasury and the Debt Management Office are set to break new ground by offering retail green savings bonds alongside September’s institutional green Gilts.

Krebbers expects a “positive ripple effect in the wider market” once the sovereign issues. “The experience we’ve had in other European countries is that the top-down effect can be quite meaningful. It improves overall liquidity and credibility of the asset class to more investors; they set up dedicated funds and mandates and push for more supply.”

The UK programme “will further encourage borrowers and investors to align their own practices along these lines", said Thomas.

Tammie Tang, fixed-income portfolio manager at Columbia Threadneedle Investments, welcomed the increasing breadth of the UK ESG market.

“Historically, supply has been focused on a few specific sectors such as banks and utilities. So it is great that now we are seeing other sectors. Greater issuance enables greater diversification in choice, particularly for those focused on building sustainable impact portfolios,” she said.

Only 3% of high-grade sterling issuance has been in green, social and sustainable formats versus 7% in Europe, according to CTI.

But corporate sales are already ratcheting up. IG sterling ESG issuance this year has now reached £7.8bn, according to IFR data. This compares with £3.4bn in all of 2020. Tesco and others have also issued SLBs in euros.

The sovereign framework’s innovative emphasis on "social co-benefits" of green expenditures could also see wider adoption in UK corporate and public finance.

“The UK could become a particularly interesting market with not just green, social and sustainability bonds, but also green bonds with a deliberate social profile as well,” said Nick Robins, professor in practice for sustainable finance at the London School of Economics.

He hopes to see a majority of UK FTSE 100 blue-chips having launched net zero-aligned capex financing strategies within a year of COP 26.

Education angle

One likely source of further supply is higher education. A public sustainability bond from University College London and a private placement from its peer King's College London have already started a new ESG debt push.

“UCL was a ground-breaking trade in the education sector, so I would expect others to at least have a very serious look at doing something similar when they look at funding,” said Alex Hardman, a vice-president at Barclays.

Bankers cite universities’ campus building improvements and their research programmes and bursaries as projects that ESG bonds could fund. One terms these “quite a differentiating proposition to sustainable investors”.

Elsewhere, the Municipal Bond Agency plans to establish a sustainable financing framework for its bonds on behalf of UK local authorities.

Some bankers also see the devolved Scottish and Welsh governments as potential ESG issuers. The Edinburgh administration is looking to demonstrate its independence by exercising its borrowing powers for the first time. The chair of the ruling Scottish National Party’s Sustainable Growth Commission recently called for £10bn to £25bn of "net zero social and economic transformation" bonds.

A deal could emerge in November to coincide with COP 26 taking place in Glasgow. “I’m not surprised this is being suggested, given Scotland are the hosts,” said one market participant.

Given the strength of investor appetite for healthcare exposure after the pandemic, National Health Service entities could even emerge, bankers suggest – though their funding flexibility is unclear. “Parts of the NHS would be very well-received,” said one banker, who cites healthcare-themed social bonds since the pandemic as well as the recent sterling sustainability bond issue from healthcare real estate investor Assura.

ESG debt sales should also pick up in higher-emissions industries such as building and property, manufacturing and transport now that power sector emissions have been driven down in the UK. For example, “we should expect more green and sustainable issuances from many parts of the real estate market”, Tang said, citing the need for the sector to be a driver of accelerated carbon reduction.