Trading volumes have risen sharply in derivatives tied to the secured overnight financing rate following the start of a regulatory push in late July to accelerate the move away from US dollar Libor.

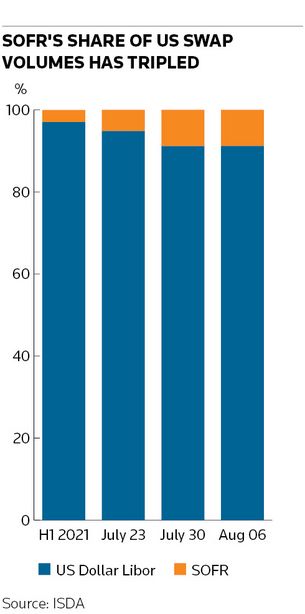

Interest rate derivatives referencing SOFR accounted for 9% of total US swap volumes in the week ended August 6, according to ISDA, three times higher than in the first half of the year.

That surge comes after the Commodity Futures Trading Commission’s “SOFR First” initiative took effect on July 26, recommending that SOFR replace Libor in interdealer US dollar swap trading conventions.

Still, despite the progress, more than 90% of last week's US$1.5trn in US swap volumes still referenced Libor, according to ISDA, underlining the scale of the challenge facing the market to meet a regulatory deadline to stop citing Libor in new contracts from the end of this year.

“The transition away from Libor in derivatives is accelerating,” strategists at Barclays wrote in a report published shortly after the SOFR First roll-out. “Data show early but clear signs that 'SOFR First' has played an important role in boosting the SOFR derivatives market, thus making a meaningful contribution to the transition away from Libor.”

US regulators have been ramping up efforts to move away from US dollar Libor following a sluggish start to the transition compared with countries such as the UK, where the campaign to drop the controversial bank lending rate is far more advanced.

Derivatives markets are central to those plans given they account for the vast majority of the roughly US$220trn in financial instruments that have historically been linked to US dollar Libor.

The CFTC’s SOFR First initiative aims to shift the centre of gravity in swaps markets by recommending interdealer trading conventions for standard US interest rate swaps move from Libor to SOFR. Interdealer broker volumes are estimated to be somewhat under half of the overall market, according to Barclays.

SOFR First doesn't apply to client trades, although regulators have said they expect no new contracts to reference US dollar Libor from the end of 2021 across the entire market.

Liquidity drive

Bankers say increased trading and liquidity in SOFR should lower transaction costs in these contracts, a current point of contention for clients, while providing more data for the wider market. More activity should also ease the transition for more complex derivatives such as swaptions.

“The next big challenge for the transition for derivatives will be ensuring that there is improved liquidity in SOFR futures and swaps prior to the end of 2021,” strategists at Citigroup wrote in a recent report. SOFR First “is attempting to solve this problem", they said.

The SOFR First initiative comes during the summer months when trading volumes tend to be lower, but analysts point to encouraging early signs. For instance, SOFR’s share of the market has grown even more when judged by trade count – to nearly 12% versus 3% in the first half of the year, according to ISDA.

On July 27, the day after the new conventions took hold, SOFR volumes were nearly a third of Libor volumes in 10-year swaps, Barclays said, compared with well under 10% in previous weeks.

But despite the progress, analysts also said SOFR First would present challenges for banks and could even increase trading costs – at least in the short term. Citigroup strategists noted regulators effectively wanted banks to hedge their Libor trades in the intedealer market using a SOFR interest rate swap and a Libor/SOFR basis swap.

“The first side effect of this will be artificially increased volumes in SOFR fixed/float swaps. However, there are clearly downsides to this. Dealers will have more variables to risk manage,” the strategists said.

Meanwhile, difficulties associated with compressing old Libor trades and new SOFR trades could cause the size of banks’ derivatives books to swell. That would be "concerning", the Citigroup strategists said, given G-SIB surcharges – the additional capital buffers global systemically important banks must hold – "are already at stressed levels".