Mariko Ishikawa, LPC/IFR: Andrew, what are the factors behind Australia being at the forefront of ESG loan financing in Asia-Pacific?

Andrew Ashman, Barclays: When you consider the Australian market, there are a unique set of factors that have helped accelerate ESG loan financings across the country. Firstly, the demand drivers for ESG capital, the borrowers or the issuers, remain high. The Australian corporate market is dominated by sectors that naturally lend themselves to ESG financing.

Sectors such as real estate, food, transport and infrastructure were early adopters of ESG financings in the global markets. It is natural that these Australian peers are taking advantage of the trend and driving the development of the product in the Australian market.

The other angle is the supply of capital. Australia benefits from a deep institutional and banking market. When you talk to investors in Australia, both in loan and bond markets, there is a sense of a real shift in sentiment over time. ESG has quickly become a key part of any investment decision, not only from a credit risk perspective, but also in terms of stakeholder engagement.

Factors such as stewardship and social responsibility are becoming more important and driving many of the investment decisions. When you combine the strong supply and demand drivers, along with this overriding environment where there is a drive to net-zero, that requires capital. So it is natural that that capital is deployed to the ESG financing market and that ESG financing has really taken off in Australia, as we have seen in many other parts of the world.

Mariko Ishikawa, LPC/IFR: Nneka, what are your thoughts on Australia’s role in ESG bond issuance activity?

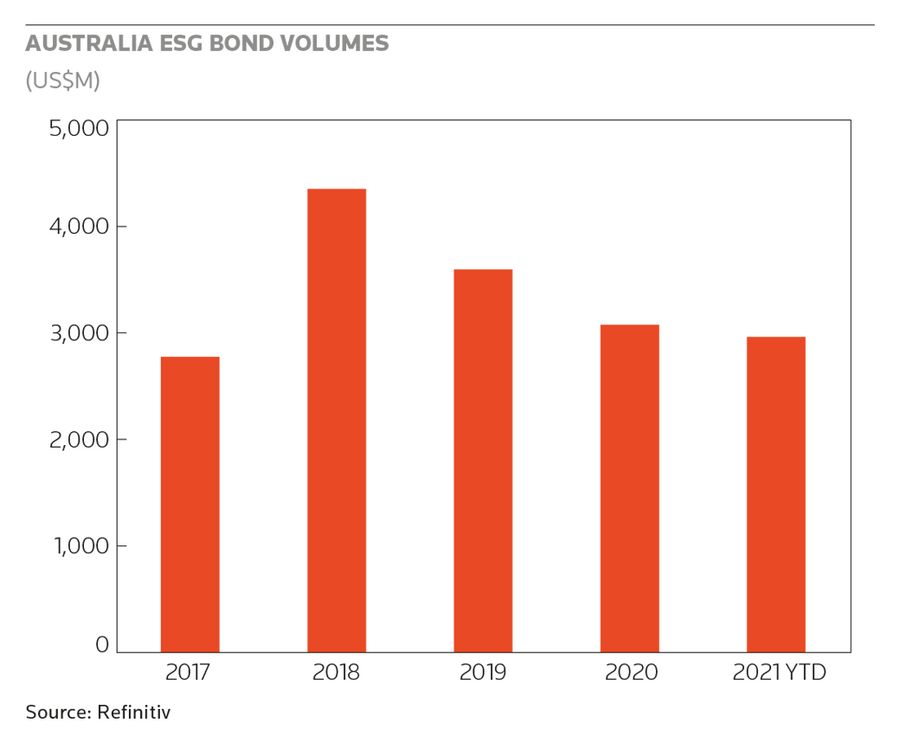

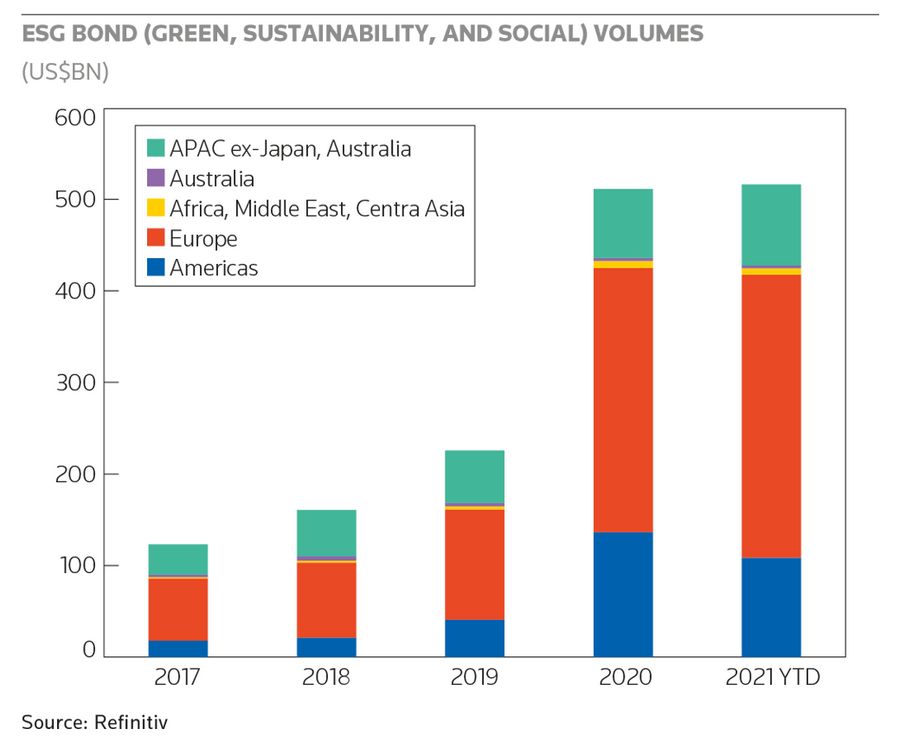

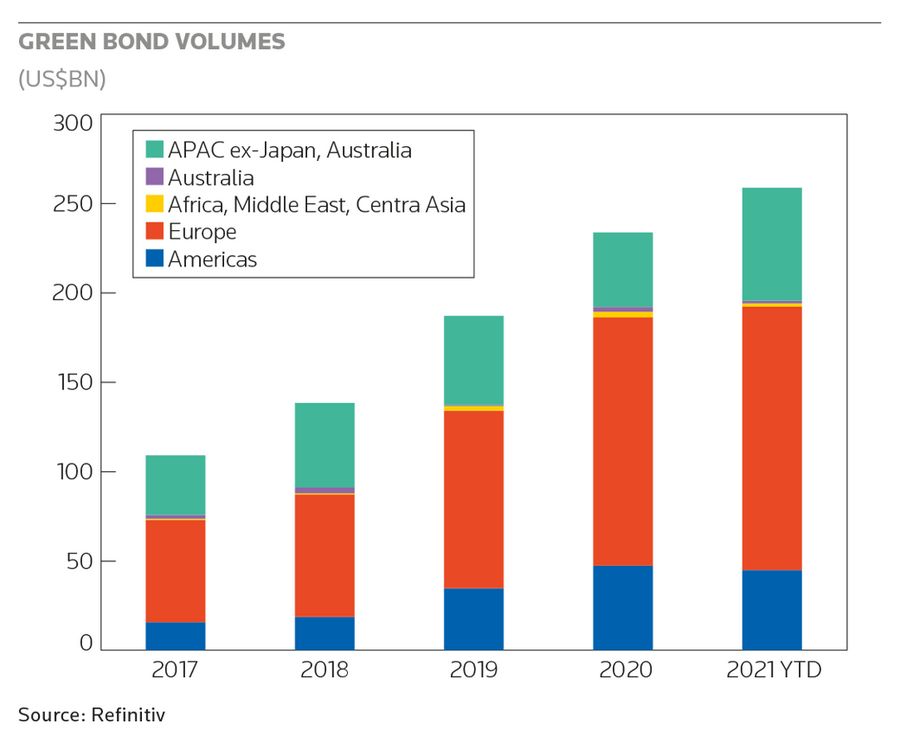

Nneka Chike-Obi, Fitch: Australia is a relatively small player in the ESG bonds market globally, with around 1% of issuance. Even within Asia-Pacific, it accounts for a very small percentage. In Asia-Pacific, China is the second-largest issuer of green bonds by value, and given the size of that country and economy, dwarfs most countries in the world in terms of ESG bond issuance. The only market that is issuing more than China is the United States.

What might be the reason for Australia being relatively small in the bond market? It is fairly easy to see when we look at Australia’s large, globally-facing companies. A lot of them are in high-emission activities related to natural resource extraction, and so they face difficulties in issuing ESG bonds.

Not only because it could require significant reshaping of the way they approach their strategy in a new world of moving towards a low-carbon economy, but also because there is the potential for questions and scrutiny from the market if a company that is involved in producing coking coal, for example, decides to issue a green bond.

So, that may be part of the reason. You can see that major companies that are potentially contributing to carbon emissions directly, like BHP, Fortescue or Woodside Petroleum. Then we have, indirectly, the banks that finance those activities. Being such a resource-dependent economy makes it tricky to really take a stance on the ESG bond market.

Even in Europe, which is a leader as far as this market goes, there is more hesitancy from companies that are in some of these mining and fossil fuels extraction businesses to enter the market and be criticised for it.

We mentioned briefly about the role of real estate and the property sector in Australia, and they are quite active in the ESG bond market. More than 40% of green bond issuance in Australia, the use of proceeds has been limited to buildings, which is actually higher than the global average, where the largest segment is energy. Around 35% of globally-issued green bonds are energy-related. In Australia, it is only 25%.

So, the Australian market is slightly different from what we see in other parts of the world and has its own unique characteristics. The property sector is also, interestingly, one of the top use of proceeds for ESG bonds in Japan, which, similar to Australia, is less active in the ESG bond market than you would expect given the size of the economy and its capital markets.

What may be happening is investing in energy efficiency in green buildings long-term probably reduces operating costs because it reduces the amount of energy that these assets require. Whereas if you look at the fossil fuels extraction industry, if you wanted to have a lower-carbon operating environment, that could essentially mean less extraction of these energy resources that are emitting. This is a dramatic strategic shift.

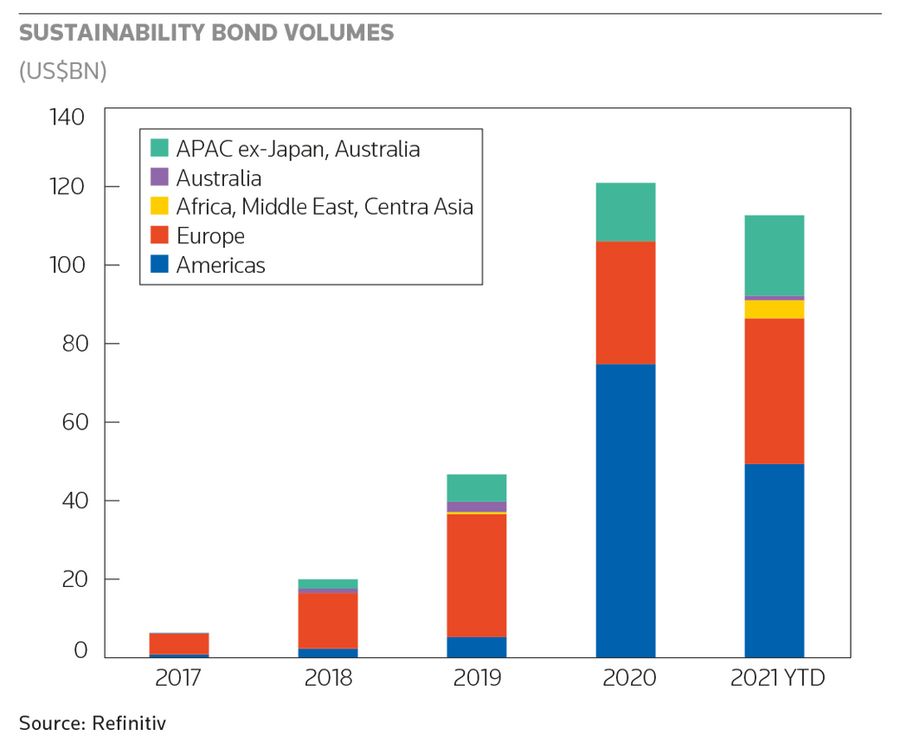

Having said that, local governments of Queensland, New South Wales and Victoria in Australia have been quite important in the ESG bond market. Low-carbon transportation has been a very popular use of proceeds among public finance issuers, urban transportation, anything that reduces the amount of carbon on the roads. The education sector has also been active in sustainability bonds, with a couple of universities issuing them.

There is a lot of opportunity, but I think some of the unique factors around the major players in the Australian economy are, potentially, why the activity in the bond market has been subdued compared with the loan market because loans are more private and more flexible for the borrower.

Prakash Chakravarti, LPC/IFR: Tania, what are your thoughts about Nneka’s comments on certain sectors lending themselves more easily to ESG financings?

Tania Smith, ANZ: I think Nneka covered off a number of the ones that we have seen at ANZ. She talked about the building and property sector. Green buildings, I think have been very big in Australia because we had a green building council that was really light years ahead of some of those overseas. The energy and utilities sector also lends itself really well with AGL Energy in Australia, Contact Energy and Mercury NZ in New Zealand raising ESG financings.

The infrastructure sector has also produced a number of transactions recently with both transport infrastructure as well as social infrastructure. The new Royal Adelaide Hospital just closed a sustainability-linked loan. Projects such as Canberra Metro and Sydney Light Rail have also closed green loans. Retailers have also raised ESG financings, including SLLs for Kathmandu Holdings and Coles, and a sustainability-linked bond for Wesfarmers.

General retailers are also getting involved, along with all of the financial institutions, semi-government and SSAs [sovereigns, supranationals and agencies]. All of those sectors lend themselves really well to ESG financings, but since the development of some of the new products that are more general corporate purpose in nature, I think most large organisations are now able to tap into the sustainable finance market, and they are really excited by that, and many are exploring those options now.

Mariko Ishikawa, LPC/IFR: Rob, what are your thoughts on which industries lend themselves easily into ESG financings?

Rob Ward, MUFG: The infrastructure sector has certainly seen an increase in ESG financings. We would expect that to continue. Social projects and social housing also have potential, but there are challenges in finding projects of scale, and getting scale to build momentum in the market.

Mariko Ishikawa, LPC/IFR: Craig, what do you think?

Craig Morabito, First Sentier: Sectors that can directly either ring-fence or show that they are able to change. There has been a large focus on green financings. Social is, a lot harder to do, although we have seen some of those.

In addition, I think entities that can source ESG data. Obviously, data uplift is required at this point in time for a large number of companies. For example, it is difficult for many companies to source the data on the carbon footprint of their supply chains.

Another aspect that would influence the outcome is companies undergoing a significant amount of change, they may find it more difficult to achieve ESG financing. Compared to stable companies that don’t have a planned material change in business profile, that don’t need to rely on a large amount of strategic assumptions to define where they are going in terms of their sustainable, green or social footprints.

Prakash Chakravarti, LPC/IFR: Frasers Property is a pioneer in many ways in ESG financings across the region. Anita, would you like to share your experiences?

Anita Hoskins, Frasers Property: If we reflect on the journey for Frasers, overall, we have clearly and publicly stated our sustainability goals. First, we have to think about our broader framework. We aim to be zero-carbon by 2028 for Frasers Property Australia, and net-zero by 2050 for the global business.

The most important step around that journey has been demonstrating commitment in long-term focus on sustainability, of which green financing becomes an important part. In 2018, we established our group’s global sustainability framework and issued our first green loan the same year – a S$1.2bn (US$880m) five-year borrowing. Since then, we have issued 23 more green loans or SLLs for a total of US$5.5bn, and we have recently completed an SLB. We also announced yesterday [August 24] our intention to issue in Australia as well.

It may come as a little surprise that we are the largest issuer of green loans and SLLs in Asia at more than US$5.5bn. We were the first borrower in the market here to complete an SLL with an interest margin stepdown. There is certainly a lot of heavy lifting that goes along a journey like that.

There are about 20 financial institutions that completed their first green or sustainable financings with Frasers. Obviously, a lot of work was required to bring lenders along on that journey with us. It is important that we all go on this journey together.

We have had to play a really important role in educating ourselves and others about what sustainable financings can look and feel like, and how it can be relevant for everyone involved. We have faced a number of challenges along the way, and, frankly, in the first instance, simply getting access to funding was a challenge.

Banks were fairly resistant to participate initially, because it wasn’t a flavour of the month, it was an untested concept. When you can’t see that immediate payoff, and you can’t see that direct improvement to your balance sheet, it can be a difficult proposition in the first instance. We are a little bit more evolved now, and a little bit more sophisticated, but, certainly, that was a challenge at first.

We don’t always see much support from regulators to drive outcomes and implement policies or support to help drive the desired behaviour. You also have to contend with challenges in the sourcing. Under the Green Loan Principles, you have to have sufficient documentation and external assessment processes. It can raise challenges that cannot be underestimated.

In the same vein, a major challenge that the issuer underestimates is this process and thinking around managing internal stakeholders. There can actually be a pushback internally, whether that is from the product lines or business unit owners who may be resistant to pay more to upgrade their underlying product or factor these costs into a product or a property development, in our case. The pushback comes when they don’t see the financing improvement as significant enough as compared to the costs that are incurred to achieve the outcomes.

In our instance, it is not about if we should do it, because we play the long game. For us, it is something that we believe in, we are here for the long-term. When you are talking about built form, you are talking about structures that are going to be around for a while. Frankly, we just can’t play the short game, we have to invest in the future.

Everyone agrees internally it is the right and necessary thing to do, but the question might turn more towards not if we should do it, but what is the right time or the right way to go about that.

One more point I will mention is on greenwashing. The way we try to address this is by using independent assessors and frameworks to bring that credibility and transparency to what we do. One of the tools that we use for this is GRESB, and I was really pleased to hear Nneka’s statistics that Australia punches well above its weight in GRESB. We target a five-star GRESB rating across our portfolio, and a minimum of four-star in our framework, so we use these as tools to help provide that transparency. They are important. They are not fool-proof, frankly, but they are important.

We have had to tackle a lot of the challenges through education and patience, but we are at a much more evolved framework, albeit still a long way to go.

Prakash Chakravarti, LPC/IFR: What advice would you give to other companies that are looking to follow through in your footsteps? What are the considerations a borrower has to look at if it wants to issue a loan or a bond in the ESG format?

Anita Hoskins, Frasers Property: To my mind, the very first question is to look at a holistic ESG strategy, or even prior to that, first and foremost, I suggest you need to revisit whether you actually have one. That might sound quite basic, but, to our mind, green financing is simply a component of a broader strategy.

So, you need to ensure you are clear on your stated objectives because that will dictate and determine what sorts of instruments, formats and products you might want to look into.

From our perspective, it is important to think about your objective. For example, if we are developing a specific residential development over a three-to-five-year timeframe, a loan could be much better and more appealing to banks. We could structure it with some more of that flexibility that was mentioned earlier around drawdowns and repayments, as opposed to having that immediate negative carry of a bond issuance.

But if you are thinking a longer-term project or cashflow, bonds could be a better option. They can allow you to tap into a wider investor base that would be unavailable under a more traditional loan structure. So, I think the important thing to know is banks are generally quite up-to-date with sustainability as an area of expertise, and they have their own in-house sustainability teams that speak the language.

Not every bond investor is an ESG investor, so there may be some education that is required on that front. But I think it just provides you access to a wider base.

Mariko Ishikawa, LPC/IFR: Do the bankers on the panel also have any advice for potential borrowers looking to tap into the ESG financings?

Andrew Ashman, Barclays: One of the areas I found when talking to debut issuers into the ESG markets, is concern around setting up frameworks – the investment in time and resources that is required to set the whole programme up. There is a lot of focus on that from issuers who haven’t quite got up to speed with the product.

I think that is an investment you need to make. It requires some time upfront to set up the programmes, but once it is in place, it is very easy to roll out future incremental financings. That is one of the learnings I have taken from working with different companies on issuance and ESG financings.

Rob Ward, MUFG: Picking up on what Andrew just said around having a strategy prepared does sound simple, but that is the first step, and linking a sustainability strategy with a sustainable financing framework is the next step. I think we will see more transit towards the bond market in time, but for a lot of borrowers, it is easier to take that natural progression of bilateral to syndicated loan facility, and then into the bond market. That is a pattern we have seen not only here in Oceania, but also across Asia, as people get comfortable with the strategies that they are developing and putting in place. And probably a little bit of flexibility in the early years as they settle into their sustainable financing approach.

Tania Smith, ANZ: Customers are often a bit surprised about the external review piece and the fact that you can leverage some of their existing assurance work. When it comes to assurance on data, at least in the Australian context, we are really lucky that a lot of companies already have to report certain environmental information like their emissions.

A lot of those companies may already have external review or assurance on some of their environmental figures, or they may already be having an external reviewer look at their sustainability reports. Issuers that are thinking about taking part in the sustainable finance market can actually make some efficiencies there with regard to cost savings if they are using their current assurance parties or external reviewers for the purposes of issuing sustainable finance transactions.

Prakash Chakravarti, LPC/IFR: Nneka, what has your experience been with regard to Australian borrowers tapping ESG bonds? What are the factors that encourage them to opt for bonds over loans?

Nneka Chike-Obi, Fitch: The bond market is interesting because there has been so much innovation in the ESG product, but the fact remains that not every company is suitable to issue a bond. We are already looking at a universe of companies – probably the best managed, the best capitalised the ones with some kind of international operations – that were, in the first few years of the development of this market, most well-positioned to go into the market.

The real estate sector has been the most active, and then the public sector, different regional governments, and also some utilities.

Some jurisdictions have introduced specific policy incentives to encourage this market. In Singapore, the financial regulator, the Monetary Authority of Singapore, has introduced subsidies that will help offset the cost of issuing any type of ESG debt, be it a use of proceeds or an SLB.

Essentially, banks that help arrange these bonds will be able to tap into a financing facility from the MAS to help offset some of the costs associated with building the sustainability framework, post-issuance review, and things like that. Singapore has attracted a fair amount of sustainability expertise in the past year or so, by trying to encourage financial institutions to view the city as a place to build sustainability centres of excellence.

Not surprisingly, in Asia, even for issuers from Australia, for example, we do see quite active involvement from Singapore-based banks like DBS and UOB. And they are quite active in the real estate sector also given Singapore’s economy.

The Bank of Japan has also introduced some incentives recently to encourage green lending and green bond issuance from its mega banks. This is a monetary policy tool where the amount of green financing that a bank makes available, double that amount will be contributed to the balance where they avoid a negative interest rate with the resource available through the Bank of Japan.

This potentially could increase green bond issuance in Japan as well, which is another market where ESG bond activity has lagged the size of the economy.

Something that generally helps borrowers is when there are new regulations and requirements for disclosures, it helps a potential issuer know what their ESG position is. When you have mandatory disclosures on climate, labour issues, water use, any sort of combination of ESG risk you can imagine, once those disclosures are put in place, it becomes easier for those companies to then have a conversation with their bank about, “What solutions could fit with what my exposure is?”

That is part of what is driving the sustainability-linked market. Australia has been fairly active in loans. It is because companies can now say, “This is my position on carbon emissions, energy uses, etc. Maybe I can improve that by this much, and then that can help me with, potentially, improving my financing costs.”

What tends to happen is there is a bit of regulation, an increase in information, because companies start disclosing and reporting more consistently. That tends to support the structure and the financial solutions in turn. That is why Europe has clearly been ahead and is the dominant region, because there is just so much regulation in Europe requiring companies to report on non-financial risks that it is very easy to almost very minutely structure products for different types of companies.

The US is starting to pick up as well with indications of new mandatory disclosures coming for listed companies probably by the end of this year or the beginning of next year. Australia already had certain climate reporting requirements, and has a modern slavery act which is, kind of a world leader as far as labour risk in supply chains goes. There are a lot of supporting factors in the Australian market that we should see more opportunities for these products coming in the years ahead.

Prakash Chakravarti, LPC/IFR: We have a question from the audience to all the panellists. How do you keep yourselves accountable to ensure any projects funded will aim to have a high impact and low or negative externalities?

Andrew Ashman, Barclays: The best mitigant to greenwashing is the use of a third-party sustainability consultant to provide an independent review. Anita mentioned at Frasers, they are using the GRESB reporting, which is clearly one of the world-renowned sustainability benchmarks in the real estate sector. Adhering to those kinds of principles and being transparent, and using third-party reviewer services, it is very important to avoid that greenwashing concept.

Tania Smith, ANZ: I think most banks have set themselves targets for sustainable finance, whether it is arranging loans or bonds for their customers. ANZ and many other financial institutions have issued green bonds or sustainable development bonds, or social bonds. As part of that issuance, there is, obviously, the reporting element.

Because our loans are our assets, we then need to report on the impact of our portfolio in that regard. One way that many financial institutions track that is through their own impact reporting of their own green/social/sustainable bonds.

On an annual basis, particularly for the linked products, for the SLLs, banks are checking in. There are compliance certificates and reporting that is being assured by those external parties. So there are annual check-ins to see how customers are doing, to make sure that they are tracking in line with those targets that have been set. Those are other ways that the public can keep track of impact around some of the transactions that take place.

Ryan Rathborne, CEFC: From the Clean Energy Finance Corp’s perspective, there are two key things that we look to in terms of monitoring ongoing compliance and, also maximising the impact that we get out of the investments that we make. The first thing we look at is tiering the sustainability outcomes. We are very interested in the corporate targets because they are the light on the hill that set the trajectory of where you want to finish, but we are also very focused on short-to-medium-term impacts that we can have.

For us, it is about getting the right mix of those long-term, aspirational, ambitious targets, and matching them with the very immediate actions that we can monitor quite closely. We look for quite a high-touch engagement model with all of our partners across all of the investments that we make.

We try and meet with all of the groups that we lend to on a quarterly basis, understand what they are doing on the existing framework and also what is next, and how we can help with the next step, and how does that accelerate things towards that longer-dated outcome. Finance has an interesting role to play in terms of not just getting the original deal done, but really accelerating and building momentum.

We have seen that in a number of sponsors. There is almost a race to net-zero, at least in the property sector, where quite a large number of funds are already invested. I think finance can play that role, almost being that catalyst for change and acceleration.

Mariko Ishikawa, LPC/IFR: Craig, how do you integrate ESG analysis into portfolio constructions, and what are your strategies for ESG debt? There is a related question related from the audience about how the buyside screens for greenwashing in its investments?

Craig Morabito, First Sentier: It really depends on the portfolio and its objectives, and there is, a suite of portfolios and ESG investment vehicles out there. The most prominent is ESG integration in the fundamental risk analysis of a credit. Incorporating the ESG risks into a credit rating, which is a probability of default. That lends itself to pricing ESG risk. If it is cheap enough, you can add it to the portfolio. If it is not, then you screen it out, and, hopefully, you get a natural tilt to your portfolio, but that isn’t always guaranteed. But that is the mainstream right now.

The next step is more important, and it is definitely increasing in terms of the clients’ interests, as well as what I am seeing out there and in line with what we are doing, which is both putting limits and reporting in place. So, limits on making sure that you do have a portfolio that has an ESG profile that is better than the market, or the benchmark, or the risk profile that it is looking to target.

You can use external or internal ratings, or data like carbon footprint or intensity, diversity scores, to flesh that out. That helps manage overall ESG risks at the portfolio level. The next step, and this I think will be the most important going forward, is stating an ESG objective for the portfolio. This is definitely happening in Europe, and they are shaping what that will look like for the industry now, which is great.

That ESG objective needs to sit right next to your return objective. For example, you have to outperform the benchmark by 1% and ensure that you have a carbon footprint 15% lower than the benchmark or the universal risk profile that you are tracking. Those requirements on a portfolio will ensure that the portfolio invests in an ESG-focused way.

Obviously, there are targeted portfolios out there aiming to be carbon-zero, or green bond portfolios, and we will touch on greenwashing shortly. For us, the key is that the company has a company-level ESG strategy, that it is not just looking to fund a specific group of assets, that are not legally ring-fenced, and instead only report on them and say, “These are green. Please fund these.” We like to see a company-level strategy. We need them to be reporting at the company level. There is a lot of work and effort involved in that, but company-level reporting is necessary, and particularly for active investors like us, our credit analysts grind through them, and report on them.

We try to build databases. The key for us is to avoid greenwashing, particularly so if a green bond comes to the market, and the company doesn’t have a corporate plan at all. That is just a simple No straight off the bat for our ESG portfolios. Then it comes down to ongoing monitoring.

As an investor, we are lucky, we can vote with our feet. Obviously, engagement happens before then. But, we can vote with our feet, sell out, and, hopefully, the market prices adjust accordingly in secondary after that. We have obviously seen that in the oil and gas, and tobacco sectors globally. They are starting to price in for the risks that investors are seeing.

Prakash Chakravarti, LPC/IFR: Tania, do you have any thoughts on this topic of greenwashing?

Tania Smith, ANZ: Adhering to the market guidelines and principles can really help ensure that customers avoid that risk of greenwashing. When the principles have been developed, they have really outlined three points that customers should be thinking about in regards to the ambition of targets, particularly for SLLs and SLBs. These relate to their historic performance, peer comparisons, and science or industry benchmarks.

Any company which is considering taking part in the sustainable finance sector and is nervous about greenwashing, needs to work with a qualified financial institution or have people working with them who have experience with applying these principles and ensure they consider those three points relating to ambition. If the company has a good strategy in place and is setting ambitious and meaningful targets that align with the market requirements, then it should be fine.

Anita Hoskins, Frasers Property: GRESB is really the output of our strategy. It is the output of everything that we do and strive for every day. It can be a time-consuming process at times, and a lot of time and resources are allocated to it to ensure that we can appropriately capture, and monitor, and go through that process. But for us, it is not the objective, it is just the outcome. If you approach it that way, you can feel very confident, as an organisation, that your results will shine through.

Prakash Chakravarti, LPC/IFR: Nneka, do you have any thoughts on how we can address this issue? Do you agree with what the others have mentioned here?

Nneka Chike-Obi, Fitch: It is a question we get asked a lot about greenwashing. It probably depends how you define it. Fitch views greenwashing as some action a company takes to make itself seem greener than it is. But I find sometimes when people ask the question, that they seem to think is that it means you issue a green bond and then you just don’t use the proceeds the way that you said that you would.

Now, that second one, I think, is quite rare. If you are working with a legitimate bank, and you have a proper second-party opinion, it is quite unlikely that you issue a green bond and you just don’t use the proceeds that way. I can think of a very small number of bonds where that happened, and it was unusual.

There was an airport project in Mexico City, and then a new government came in and decided to cancel building the airport, so then the proceeds were, kind of, stranded. There are dark green investors who will never buy a green bond from a fossil fuel company. It doesn’t matter what their sustainability strategy is, how much they are trying to reduce their carbon emissions. The investors have decided there are certain sectors that they will not invest in, regardless of what the label says on the bond. And that is their right to do so – different investors have different strategies, and it is fair enough to them if that’s what they want to do.

I agree with my other panellists who are saying that, as long as you follow international best practices, be that ICMA, the Climate Bonds Initiative, the EU now has a green bond standard that they are working on releasing, as long as you align yourself to clear, preferably science-based targets, in whatever ESG financing that you choose, there will always be investors who are willing to give you a chance as long as the financials of your company and the governance of your company are up to those standards.

But very few companies are going to be able to meet the standards of the most ESG, the most green, the most sustainability-concerned investors. What would be unfortunate is letting the perfect be the enemy of the good, and people being so afraid of being accused of greenwashing that they don’t even go into the market at all, when the reality is that we do need these activities to be financed to achieve a low-carbon economy by 2050.

People just need to have the right partners, the right programme, and the rest will settle itself. In general, green bonds are priced better than traditional bonds from the same issuers, and generally there is more demand for green bonds than there is supply. At the moment, it doesn’t seem like there should be an issue if somebody wants to issue a green bond, as long as they do it the right way.

Prakash Chakravarti, LPC/IFR: There is a question from the audience about independent validation. Nneka, would you like to comment on that, and then if Rob can jump in with his thoughts? Is there a body that SETS minimum standards for independent validation?

Nneka Chike-Obi, Fitch: There are international standards with regard to the use of proceeds of the SLB and SLLs. However, I don’t think there is any jurisdiction at the moment where it is legally required that, a green bond has to be aligned to those standards. That is important to know. When it comes to the external reviewers, a lot of countries have a registration process to be followed to be a third-party issuer reviewer.

What the EU is trying to do with its green bond standard is actually require those external reviewers to almost be like how a credit rating agency like Fitch is, where you have to be registered with the European financial regulator, ESMA [European Securities and Markets Authority], and that, I think, is going to be the strictest regime. But that is only going to be applicable for companies that want to issue bonds under the EU bond standard, and we don’t think that the majority of companies, even within the EU, would meet that standard. It is going to be, pretty much, the highest standard possible.

With these third-party review companies and also, external ratings, it is a bit of a mixed bag. If you look at different ESG ratings, correlations are not always great, especially in the social and governance categories, but a little bit more consistent in environmental issues. Something that I noticed about SLLs is that when the product first started developing in 2017/18, a lot of the loans were linked to a third-party rating. So, my ESG rating is an A from some company. If I get from a B to an A, then I will reduce my interest rate.

Over the years, borrowers seem to have moved away from that, with the exception of GRESB, which is pretty much a very well-respected global standard. Some of the other companies prefer to create their own sustainability targets that is more structured to their actual operations. It seems like a lot of investors would love to rely on off-the-shelf ‘this third-party reviewer is good, and consistent, and what they produce is always going to tell me the right answer’, but we are just not there yet.

That is the nature of a growing and developing market. Maybe we will get there, but it is possible that regulation may need to happen, like what Europe is trying to do, to get to the point that those companies are consistent enough and held to a high enough standard that you can trust that their reports are always consistent. A Chinese company issued a sustainability bond with a second-party opinion, but the amount of money from the bond’s proceeds that will go towards sustainable activities is not clear.

Just because you have an external review doesn’t mean that the bond is going to meet your standards based on the label. Not that the activities are not sustainable – they are – but the amount of money, of the offering that is going to those activities is not in the prospectus at all. So, that would be an issue for some investors, even though they did have a review from a reputable company.

Rob Ward, MUFG: Certainly there is clearly a tightening up in the market with regard to third-party verification. We saw the loan principles updated by the LMA, and, again, it kept pushing people more and more towards getting a third-party involved. We think that is sound, particularly as time goes on and we see more and more institutional investors in the market, be this in a loan or a bond format. The chances that there will be parties which actually require that, we think, will increase over time.

Just picking up also on the comments on using an external benchmark versus internally-generated KPIs. We are certainly fond of and keen on having a combination of the two. I think, definitely, a trend toward either internally-generated KPIs that meet certain benchmarks, and industry norms, and best practice, perhaps coupled with scores from some of the agencies, be it GRESB or some of the other providers. We think that it provides a good blend and gives investors and borrowers a sound basis on which to make an investment decision.

Tania Smith, ANZ: There are a few bodies which approve external reviewers. The Climate Bond Initiative has a list of approved parties, which can provide second-party opinions on transactions. We often look to the list of CBI-approved reviewers. As Rob mentioned, there is recent guidance that was updated by ICMA and/or the LMA around providing guidelines for those external review parties.

We are starting to see a lot more consistency in the output that is being produced off the back of those guidelines being developed. Regardless of the party that is carrying out the external review, if it is following those guidelines and if it has been approved by the CBI or an independent group, you are probably likely to come out with a fairly consistent output now as the market is developing. We have seen a lot of interest in ISCA [Infrastructure Sustainability Council of Australia] here in Australia as well, as a rating tool.

Mariko Ishikawa, LPC/IFR: Australia’s pensions market, which is the world’s fourth largest, with A$2.9trn of retirement savings. Craig and Ryan, what do you think is the key to unlocking this pool of capital for ESG/green financings?

Craig Morabito, First Sentier: They are well on the way. I can’t think of how many, surely more than 10, heads of sustainability have been appointed in the last 12 months. One of the points to note is that, institutionally, there has been a large push to passive investment, both in equities and debt.

And it is very hard to do passive investment in ESG. You can set up a green bond portfolio, but then we come to those issues that have been talked about here like greenwashing. So, again, nobody wants to be involved in any risk of greenwashing with their funds. So, it is working out the right strategy, the right portfolio objectives that also meet their underlying members’ requirements and desires.

Whether that is different types of product suites, so ones that are focused on net-zero, ones that are focused on SDGs [sustainable development goals], ones that are focused on just ESG as thematic tilting. Our super fund clients are talking to us about different ESG products. We have ESG-driven products from some of our superfund clients as well, so it is definitely picking up. It takes time, but I think the build-up in allocation will be there in time.

Ryan Rathborne, CEFC: There is a real craving for product, and good product, in the market. We have been involved with the non-bank lending market, the real estate or commercial real estate debt and worked with a manager locally here to design a new sustainable debt fund that sought to attract that offshore pension fund asset base into products here. We saw that really resonate, especially the ESG theme.

We built in minimum environmental standards that projects simply had to hit to be even considered for funding. We are finding interesting opportunities that resonate with both the domestic and offshore asset allocators.

I think that is something that we will continue to see, and more inclusion of minimum sustainability standards within products and fund strategies. That I think is really interesting and has the potential to make a huge impact in some of those harder-to-abate sectors as well. If they know there is capital there that requires a change to business or more comprehensive thought around long-term decarbonisation, that is a really powerful message, and something that the mandates of those large asset allocators firmly have their sights on as well.

Mariko Ishikawa, LPC/IFR: What do you think are the barriers to tapping the growing number of non-bank lenders to form the liquidity pool for ESG financings?

Ryan Rathborne, CEFC: We have spoken to some non-bank managers who are struggling with the potential spiderweb of rating tools and how they apply internationally. It is very hard to have a global approach and roll that across jurisdictions neatly, so each jurisdiction requires a bespoke approach.

I think that is one of the challenges that we have seen. It is like all challenges, there is a solution through it, but it does require a bit more thought to work out what is the right sort of approach for each market, building on either regulatory or voluntary rating schemes. One of the challenges has been to find a large enough opportunity to do that work to get into the space. To the extent that we can reduce friction around that, that would be a really positive thing.

Craig Morabito, First Sentier: I don’t think there are many barriers for ESG bonds as demand is definitely outstripping supply at this point in time. Maybe with ESG loans, where intermediaries are the custodians of the relationships historically, and are the arrangers. It is not a barrier, but that is the portal that a company needs to go through to tap non-bank lenders.

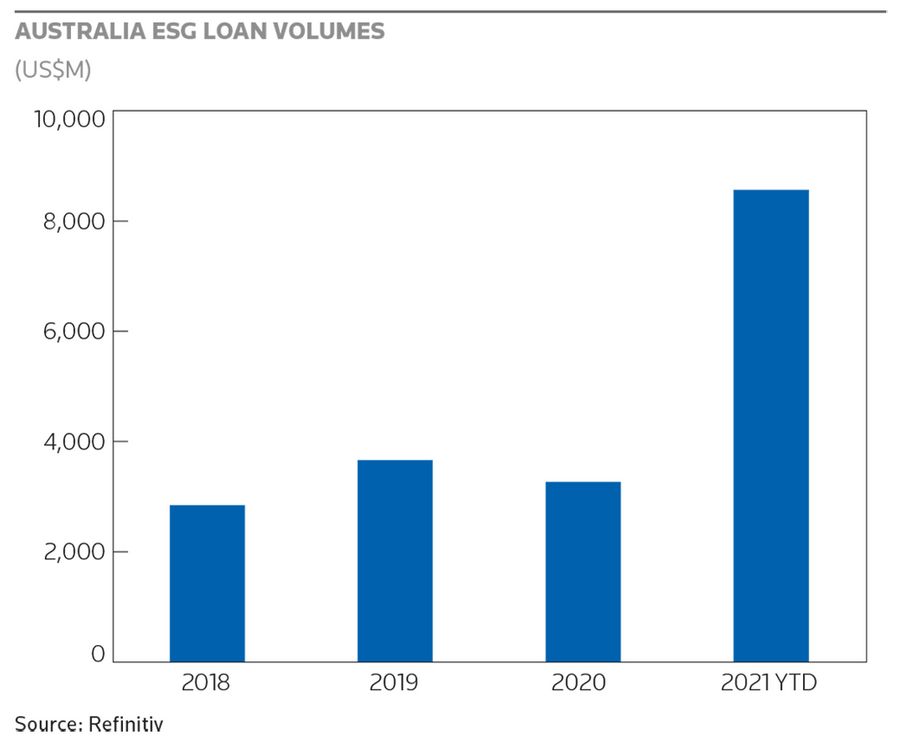

Prakash Chakravarti, LPC/IFR: Global ESG bonds account for 9.7% of all bond issuance, and that is up from 5.3% last year. ESG loans make up about 12.5% of all loan volumes. Again, this is also up from 5.7% last year.

Anita, my next question is to you. With regard to your future plans for funding, what is the strategy you would take with regard to ESG financings? Do you prefer a bond over a loan? You mentioned this earlier in the conversation, but it would be good to get a deeper understanding of your strategy.

Anita Hoskins, Frasers Property: That is quite a growth year-on-year. Frasers in Australia, 45% of our corporate funding is now secured in the form of SLLs. We do have some further facilities, a further green financing facility in place for some of our off-balance-sheet joint venture structures, but, from a corporate perspective, 45% of our funding is in that format.

At the Frasers Property level, approximately one quarter of our total external funding is in the form of green or sustainable financing. It is certainly something that we are committed to. To your question about future plans, the more the better.

Going forward, we are committed to furthering our sustainable financing positions. We have a clearly stated objective to finance the majority of our sustainable asset portfolios with green and sustainable financing, so it is safe to say that we see green financing as an important part of our strategy, and we intend and hope to do more in the future. Certainly, we would like to do more in bonds.

The majority of that one quarter of our external funding stat that I just mentioned is in the form of green loans, SLLs. We would like to do more in bonds, but it has to be right. You have obviously, got to look at factors such as the flexibility, the tenor, what is going on in each individual market.

We have to reapply that continued growth statistic when we talk about what the stat is next year. We have to be a part of driving a further increase to that growth that you just quoted.

Prakash Chakravarti, LPC/IFR: Andrew, when you have discussions with corporate CFOs, do you go in with a preference for a particular product? How does that work?

Andrew Ashman, Barclays: Like most banks, we are product-agnostic. Every situation has a different tool – sometimes bonds work better, sometimes loans – and it is our job to find the right solution for our clients. As bankers, we should be agnostic about what type of product we are offering to our clients.

What we do find is that, generally, the issuers that are coming to the ESG financing market for the first time are using the loan product, and that is because they have a group of relationship banks to form a syndicate, it is a little bit more flexible, there is prepayment ability, and you can tailor the product in more ways than a bond. As issuers become more experienced in the market, they start to look at the bond product.

There are advantages and disadvantages of both, but the bond market is very open at the moment, there are pricing advantages by having that ESG label on the bond over a standard bond, and it is a way of diversifying your funding sources with a non-amortising debt product.

Tania Smith, ANZ: We look to understand what the client’s funding needs are, and, usually, their treasury team will have a strong view on what sort of products they want, whether it is bonds or loans. Because we have sustainable finance options in each of those formats, we can tailor products that are appropriate for their funding needs.

It has been really great in the last couple of years, we have seen a real diversification of products. SLLs have only been around since about 2017, but now we are seeing green guarantees, sustainability-linked derivatives and the like. There is a diversification of different types of products that can now have that sustainable finance label associated with them. That means there is a greater breadth of ESG products that customers can tap into based on their normal funding needs, just adding that sustainable finance element on top.

Rob Ward, MUFG: The decision whether a loan or bond really is independent with the ESG decision. It is to respond to a financing need more so than a positioning one. The key is probably setting up structures for our clients that are able to be replicated in either.

One of the most annoying things for a borrower would be having different regimes applied to different facilities and different bonds. So, having something consistent that makes a lighter impact on the borrower in question that can be used in either a loan or bond format, or for other products, indeed, is probably the best starting position to get.

Mariko Ishikawa, LPC/IFR: What are the guidelines that are necessary for growth of ESG financings?

Tania Smith, ANZ: The Australian Prudential Regulation Authority is already looking at banks in Australia, at least, stress-testing their portfolios, and I think that it helps the banks to further understand ESG for themselves and their customers, but things like capital relief would be really helpful for the banks, and help drive more ESG funding.

We have seen it in certain jurisdictions, mandatory-disclosure-type regulations and requirements also help corporates and the financial sector understand the risks and opportunities. That mandatory disclosure can help drive greater activity and volume in ESG markets.

In Hong Kong regulators have helped subsidise some of the costs around external reviews. That has also helped companies which might have been unsure about whether or not they should take part in sustainable finance transactions. That has removed another one of those barriers for them, and so it has allowed more borrowers to take part who might not otherwise have. They are some of the factors that regulators could help influence that would drive greater volume in ESG markets.

Rob Ward, MUFG: The regulators have a role to play, but I think whether they remain relatively active or not, this drive towards ESG financing is as much coming from the investor base and the corporates themselves. Stakeholders other than regulators are equally important.

We are seeing as much drive to ESG coming, and including regarding disclosure, whether more specific disclosure is required or not by regulators. Investors, other stakeholders and third parties are insisting on heightened levels of disclosure. Regulators have an important role to play, and many of the points that Tania made, are absolutely valid. Whether the regulators move fast or not, this tide is already moving, and the requirement on borrowers and arrangers of finance will be there whether regulators move fast or not.

Andrew Ashman, Barclays: I completely agree with Rob there. The private side is really important in driving ESG financing here, but the regulators have a very important role in acting as a catalyst to support that growth. In Singapore, we have a very strong regulator driving that ESG financing trend. We have already spoken about the grants the MAS is offering to local corporates to cover ESG financing costs. They are also offering very extensive training schemes to local banks operating in this market. The MAS is also encouraging the setup of regional-based sustainable financing teams in banks in Singapore.

The regulator here is dedicating a significant amount of capital to asset managers for the ESG financing market. So, there is a role for the regulators, but growth has to be driven by the private side initially.

Prakash Chakravarti, LPC/IFR: Anita, I would like to ask you one other question about your acquisition and growth strategy. Does decarbonisation play a big role in this now?

Anita Hoskins, Frasers Property: I would suggest our decarbonisation and broader sustainability targets form a really important part of how we assess an investment opportunity. If I talk specifically about Australia, we are a property development company, we generally focus on land acquisition. And these sustainability targets that we have form an integral part of our assessment of returns.

The role that we take in development and risk is great because we can shape the design and the planning of these developments that we have in play. When we are building these initial acquisition feasibilities, we just build all of that planning in, and it just becomes a simple part of a broader picture of the returns that will be driven by this opportunity.

There are a number of examples of where we have actually implemented that practice. Our Burwood Brickworks retail shopping centre in Victoria was awarded the world’s most sustainable shopping centre under the Living Building Challenge, which is the most advanced measure of sustainability in the built environment. It is a really exciting and interesting solution, and it includes a rooftop urban farm, installed solar panels, capturing reuse of rain water, and much more.

But to your question about growth, we can factor all of that thinking into our investment committee process of assessing the broader returns. So, sustainability becomes a part of that. There are other examples as to how we have been able to identify a range of quite novel and interesting solutions to help drive those targets.

There is no simple silver bullet for achieving decarbonisation or wider sustainability targets. We have a project in Queensland, where we first trialled an offering of carbon offsets for purchase by residential buyers. What we learned from that is bringing your customers along the sustainability journey is also really important. But, again, there is a whole range of different solutions that we can employ.

When we think about it in terms of growth, we have learnt that it is imperative to apply that sustainability lens to opportunities at a very early stage, at a pre-acquisition stage, because, we know it ultimately drives better outcomes.

Mariko Ishikawa, LPC/IFR: To all the panellists, what do you think are the prospects for ESG financing in Australia, and what do you think we will be talking about next year?

Rob Ward, MUFG: In five years’ time in Australia, we probably won’t be talking about ESG as much, and the reason for that is it will be just ubiquitous, and it will almost be a passport to getting finance in a meaningful quantity from the market, rather than what has been actually a novelty that has turned into an advantage.

We are going to continue the growth we have seen for the foreseeable future until we get to a mature single-digit growth kind of market. But in five or 10 years from now, it will be an essential part of finance, rather than a minority component.

Ryan Rathborne, CEFC: I am probably looking forward to two factors. One is a very integrated link between debt issuances and net-zero trajectories. That is a real area of potential growth across the economy. So actually drawing your curve down to net-zero and then tracking how you are going against that. I think that is a really interesting development in terms of linking potential step-up, step-down ratchets to ongoing emissions performance, which we have been thinking a lot about at the CEFC.

The other interesting area as well is the very strong focus on scope 1 and 2 emissions. But I think a day will come where scope 3 starts to get a lot more attention. The Green Building Council of Australia recently issued a report that said in 2019, 16% emissions came from construction in Australia, within the property sector. By 2050, that will be 85% because the electricity grid will decarbonise and other things will happen.

That has to come into focus, and that creates the sort of demand to help other sectors decarbonise, as well, which are potentially more challenging around concrete, industrial sorts of companies. We are going to see a little bit more collaboration between sectors and their respective targets.

Tania Smith, ANZ: I might echo Ryan’s comments around scope 3. We are hearing a lot of that in the market at the moment. And the other things to watch out for are focus on biodiversity. With the development of the Taskforce on Nature-related Financial Disclosures in Europe, I think that, over the next year or two, biodiversity is going to take an increased focus for a lot of companies.

There will be a focus on carbon markets as corporates make these net-zero commitments and start trying to find ways to manage their emissions through power purchase agreements and offsets. I think carbon markets, particularly in Australia, will become a greater focus, because we are lucky, we have high-quality carbon credits.

I also think that the focus on the social element will continue post-Covid, focus on a company’s social licence to operate will still be important. The prospects look pretty promising for the sustainable finance market in Australia going forward. We are certainly very busy, and I am sure the other banks are as well.

Andrew Ashman, Barclays: I completely agree with all the comments. From a European bank’s perspective, some of the trends that we are seeing in Europe are often leading indicators for this part of the world. Disclosure is something that we have spoken a lot about on this panel already, but the European Financial Stability Board’s Taskforce on Climate-related Financial Disclosure is a key development in Europe at the moment.

The TCFD is going to create more climate-related disclosures from the fund management industry. This will not impact Australia directly, but a lot of the global funds are now implementing that as a gold standard across their platform globally. I can see more of that kind of disclosure coming, more regulators in this market will insist on increased climate-related disclosure from the asset managers, and disclosure will certainly increase in the future.

Craig Morabito, First Sentier: We are looking for more information so that we can build portfolio level reports, but also so our clients can set the objectives for the portfolios, which is key. It is very hard to set objectives versus a universe when there is little information in the universe to set it against. So, definitely there is a build-up of information and data for companies that is needed, which will be difficult for companies to work through. It is obviously, just going to take time, but, hopefully, sooner rather than later.

Prakash Chakravarti, LPC/IFR: Nneka, would you like to comment on this topic?

Nneka Chike-Obi, Fitch: On the social side, for sure, particularly companies which have an environmental and social supply chain, will be in focus. Obviously, you are not just talking about downstream emissions, but also looking at where and how products are being produced and sourced, I think, is something that is getting a lot more attention.

Just as an example, people are going to electric vehicles because they have a positive environmental impact, but there are concerns about the metals that go into those vehicles, and whether or not those have other environmental or social risks related to forced labour, and things like that. I think that is going to be interesting.

There are already some really interesting projects happening in Australia. What I am interested to see is the step change with grid-scale batteries and what that is going to do for the renewable sector and the amount of financing that can go into renewable energy once there is more reliable large-scale storage of renewable power.

There are a couple of big grid-scale battery plants that have set up in Australia, and I think that is an important testing ground because that will be the next important step in achieving these goals towards net-zero in 2050.

Also potentially, sovereign issuances focused on conservation, echoing what was said about biodiversity. There is a lot of opportunity where private companies don’t have a role, but in a country like Australia that has some incredibly sensitive and important ecosystems, there could be the potential for either an international or supranational agency or the Australian government, itself, to look at sovereign issuances around nature conservation.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com