US derivatives traders are facing a race against the clock to move away from Libor ahead of a looming regulatory deadline to drop the controversial bank lending rate from new transactions from the end of this year.

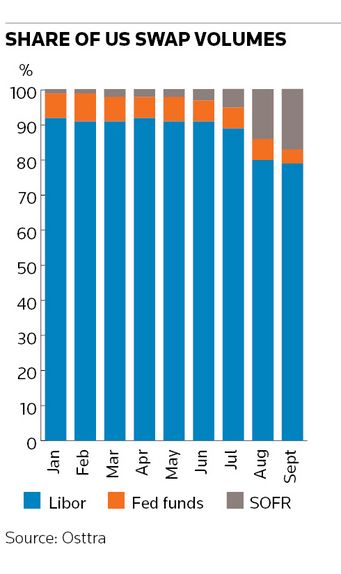

US swap trading volumes linked to the secured overnight financing rate, regulators’ preferred US dollar Libor replacement, have increased roughly sixfold since June, according to post-trade services provider Osttra. But Libor still accounted for nearly 80% of US swap trades in September, underlining the scale of the challenge that remains.*

And with year-end fast approaching, industry experts note there is still considerable uncertainty over how these markets will look in the future. That includes the potential role of credit-sensitive rates such as Bloomberg's BSBY index and AFX's Ameribor as well as the amount of Libor-linked trading that will need to occur next year to reduce risk as derivatives users adapt to the new market paradigm.

“There are still plenty of real-money accounts trading Libor and there’s a fair amount of work to be done to move people over,” said Bart Sokol, a managing director in rates trading at Barclays, who noted that it was mostly an issue around systems rather than fundamental objections to SOFR.

“We’re close to the finish line but there’s still a lot of finishing touches that are needed. Regulators have been pretty clear about not trading new Libor from the end of this year – that’s unambiguous. We have to wait and see what happens with our customer base and their interpretation of things,” he added.

Global regulatory efforts to eradicate Libor have accelerated this year. Libor’s sterling replacement Sonia made up nearly 80% of volumes in September, according to Osttra. There has also been a dramatic shift away from Libor in Swiss and Japanese swap markets, where the alternative rates (Saron and Tona) now account for more than 60% of volumes compared with 5% or below at the start of the year.

The roughly US$220trn market in US financial instruments tied to US dollar Libor has proved a far tougher beast to shift, though momentum has picked up since a regulatory-led push to move the interdealer swap market to SOFR in late July.

Brokers estimate 90% of interdealer volumes are now SOFR-linked, while Sokol said a decent cohort of his clients (mainly hedge funds) have also embraced the risk-free rate. Improved liquidity in SOFR swaps has been a pivotal factor.

Composite bid-offer spreads are now tighter in SOFR than Libor-linked US swaps across most major tenors, according to Tradeweb. Angus McDiarmid, rates product manager at the bond-trading platform, said an increasing number of clients have been conducting test trades with SOFR.

“The liquidity in SOFR swaps is good now, both in terms of bid-offer spreads and market depth,” he said. “Once the liquidity is the same and you have the operational parts in place, you have no barriers to switching.”

Sokol said the US dollar swaption market’s expected move to SOFR in November should further increase volumes linked to the risk-free rate. Daily trading volumes in US dollar swaptions are running at about US$27bn this year, according to data from ISDA.

Listed progress

There has also been considerable progress in the listed derivatives space. CME Group introduced fallback language earlier this year that will automatically convert eurodollar futures into SOFR futures when the remaining US dollar Libors stop being published in mid-2023.

SOFR-linked eurodollar futures contracts have grown 70% since then to more than US$20trn in notional, representing about 38% of all of CME's short-term interest rate derivatives. Meanwhile, average daily volumes in SOFR futures contracts are up 169% year-on-year, with over one million contracts outstanding.

“It is one of the most impressive product launches we've ever had,” said Agha Mirza, head of rates and OTC products at CME Group. "We are seeing growth in SOFR futures as well as eurodollar futures with SOFR-based fallbacks.”

Eurodollar futures are expected to be one of a handful of instruments traders use to reduce Libor-linked risk from next year. Such risk-reducing trades are also expected to be permitted in the swaps space.

“We still expect there to be a fair amount of liquidity in Libor after year-end. There are a lot of clients that have Libor trades on that will need to be unwound,” said Sokol.

Credit sensitivity

Still, it is not clear how regulators will police such activity. There is also a great deal of uncertainty over the role of credit-sensitive rates, which many participants have argued are badly needed in parts of the market such as corporate loans.

“There is a valid reason why a credit-sensitive rate like Libor has been so successful. The underlying credit sensitivity is an important part of the equation," said Mike Koegler, managing principal at consultancy Market Alpha Advisors.

SEC chair Gary Gensler said last month that Bloomberg’s BSBY index – the one-time front-runner among credit sensitive rates – has “many of the same flaws as Libor” and that he didn’t believe it met regulatory standards.

That has put a chill on activity in that part of the market, traders and consultants say. Bloomberg has previously said an independent review by accounting firm EY confirmed that BSBY is compliant with IOSCO’s principles for financial benchmarks.

“BSBY is kind of dead at the moment. My clients are not going to use it for the foreseeable future," said Koegler. "No one wants to do a transaction tied to BSBY if a regulator takes the position that it may not be IOSCO compliant."

*The second paragraph has been updated to clarify the nature of Osttra's business.