IFR ASIA: China bond markets have been on a constant pathway towards internationalisation over the past few years, from the introduction of Dim Sum bonds and Pandas to the growth of the offshore bond market, where China now dominates Asia.

FTSE Russell announced in March this year it WOULD be adding Chinese bonds to its world government bond index from October so that should be another impetus for foreign investors to add to their holdings. The hugely successful Bond Connect scheme, which allows foreign investors to buy onshore bonds more easily through Hong Kong, is expected to announce the southbound leg initiative to allow Chinese investors to buy offshore bonds very soon. [DETAILS OF BOND CONNECT’S SOUTHBOUND LEG WERE ANNOUNCED SHORTLY AFTER THIS ROUNDTABLE.]

So let’s kick off with a high level question. What progress is being made to internationalise renminbi bonds?

IVAN CHUNG, MOODY’S: I think in terms of the amount and the size of the transactions we have seen a gradual increase in foreign investor holdings of renminbi-denominated bonds in the past few years.

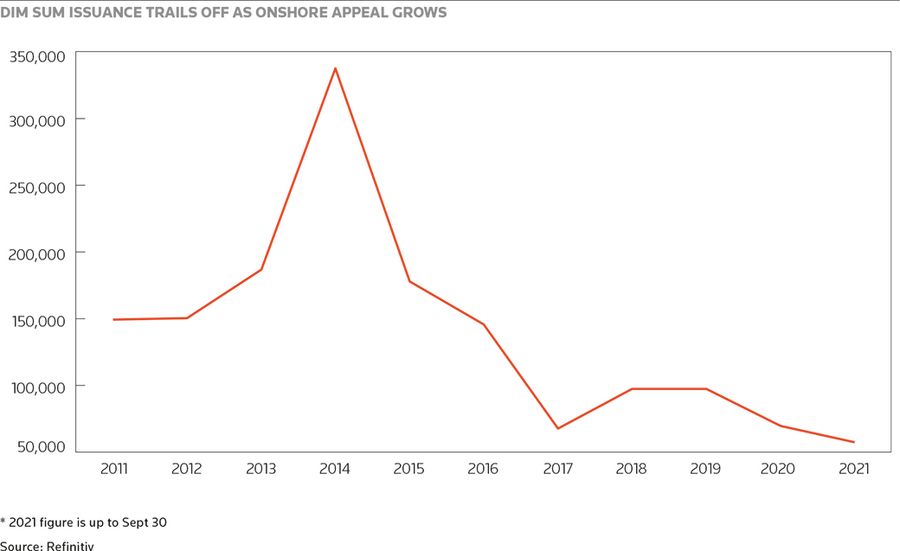

However, over the past few years, you see the changes as the money shifted from the Dim Sum market directly to the onshore market, due to the establishment of the Bond Connect and other avenues which allow investors to directly invest in the onshore market.

Given that the onshore market is now the second largest in the world, there are lots of choices and liquidity for them and that’s why more investment money goes directly to the onshore market. As a result of that you will see the Dim Sum market is relatively stagnant but overall in terms of internationalisation in a wider sense the foreign investor holding has actually been increasing.

Interestingly, in the old days, when you look at the Dim Sum market, there was a variety of issuance from corporates, from financial institutions, and Treasuries were relatively small.

But in the onshore market the international investors have a different view. The market is almost Rmb3trn, so close to US$500bn.

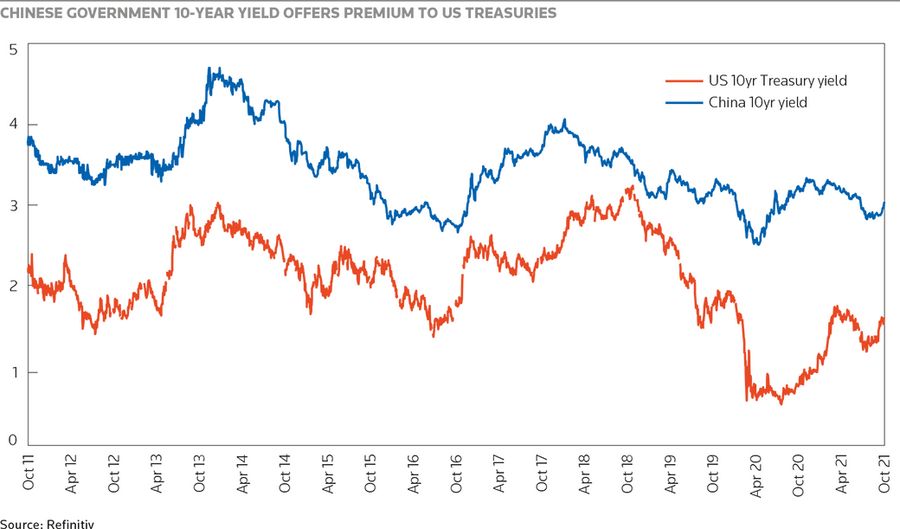

Almost 90% of foreign investors are in Treasuries or policy bank bonds, for obvious reasons because they are low risk and there is lots of liquidity in the secondary market. And more importantly, if you compare the yield with the G7 bonds, they are pretty attractive. Five to 10-year bonds are offering 3%, not to mention that the RMB exchange against the US dollar is fairly stable.

So investors don’t dare to spend more time to look at the corporate bond market onshore which has a different rating system and different disclosures than the US dollar bond market, which they can already buy and get China exposure.

I will say that it has been growing well and is quite likely to continue to grow. Even though the investor allocation in the Chinese market is small, many global indices now have increased the allocation of Chinese RMB-denominated bonds. Secondly, in terms of the diversification, this still needs some more work because investor interest is mainly focused on the Treasury and policy bank bonds. For corporate bonds it’s more selective on certain names that have offshore issuance or are big SOEs. I think the trend is that it will continue to grow, and I think they will see still a lot of development in the next couple of years.

IFR ASIA: Mark, how does Bond Connect broaden the appeal of Chinese domestic bonds?

MARK LI, CICC: Well, in my opinion, Bond Connect has been playing an important role in offering China’s interbank bond market access to a broad group of international investors. Also, the designated task of Bond Connect is to provide mutual market access to let investors from mainland China and international investors trade in each other’s markets through its market infrastructure linkage in Hong Kong.

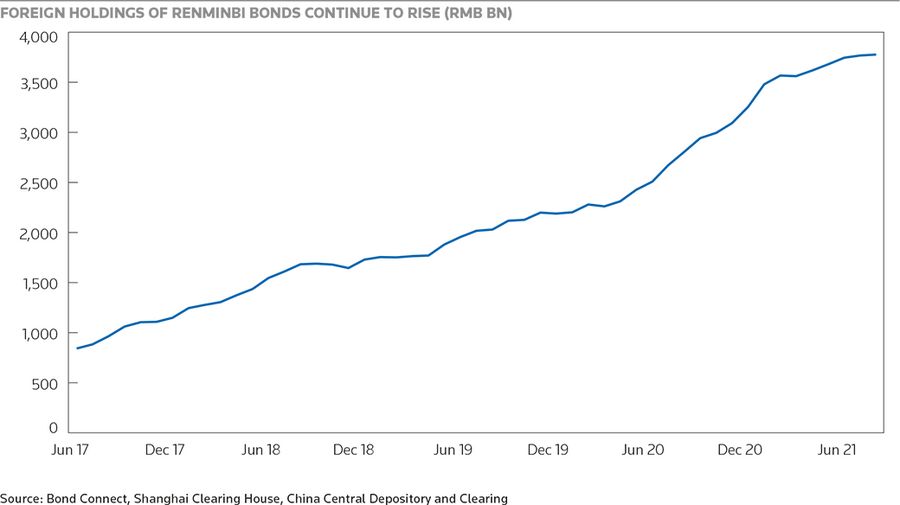

Currently, the Northbound flow has already been proving the bright future, broadening the appeal of domestic bonds. By having the Southbound flow, we believe that it will do even better. I have a few numbers to support this opinion. Up until August 2021, the average daily turnover at Bond Connect amounts to Rmb26bn. Over 2,700 investors are registered with Bond Connect. Right before July 2017, when northbound trading was officially commenced, the total holding of foreign investors in China’s domestic bond market was only Rmb843bn, and these numbers right now are more than Rmb3.8trn. So you can see that the compound annual growth rate stands firmly above 45%.

Nevertheless, taking into account the total size of China’s domestic bond market is well above Rmb120trn, and the foreign holding is only between 3% to 4%, it shows a remarkable growth potential by having the growth rate at nearly 46%. And we believe that cost saving and efficient Bond Connect infrastructure could do more for the world’s second largest fixed income market.

IFR ASIA: Jennifer, has Bond Connect has made foreign investors more interested in Chinese bonds?

JENNIFER ZHANG, BARCLAYS: If we’re looking at the pattern as Mark mentioned, the foreign ownership of domestic Chinese bonds has increased dramatically. In the past four years, we have seen foreign investors have benefited from easier and looser trading systems as well as the settlement mechanism. They can place the orders using the electronic trading system, the one that they are very familiar with. Also, in terms of the settlement mechanism, there is a multi-tier settlement and custodian mechanism, which means offshore investors can directly face CMU (Central Moneymarket Unit), a unit of HKMA, and CMU in turn faces either Shanghai Clearing House or the China Central Depository and Clearing system.

Going forward, we do expect continuous and more active participation from these international investors in China’s onshore market due to a couple of factors. One is due to the low correlation of Chinese assets with global assets. Actually, Covid-19 has reflected China has more independent, lower correlated economic development compared with developed countries. Chinese assets would add a diversification effect to the global assets held by international investors.

Secondly, the inclusion of Chinese bonds into the global bonds fixed income indexes would definitely push international investors to take a closer and deeper look at the domestic bond markets in China.

IFR ASIA: Talking about the growth of the onshore market, will there still be a need for Dim Sum bonds as Bond Connect increases in popularity and the Panda market grows?

MARK LI, CICC: Being two of the leading facilities for the renminbi’s internationalisation, Dim Sum bonds and Panda bond issuances are both crucial for the market. Dim Sum bonds are the platform and bridge for Chinese issuers to get overseas funding while promoting the internationalisation of the renminbi, while Panda bonds aim to attract overseas issuers to get RMB funding in China’s domestic markets. Both are quite important. Until early September 2021, market statistics show that the total size of Dim Sum bonds and Panda bonds are respectively Rmb551bn and Rmb247bn.

From January to the beginning of August this year a total of 45 Panda bond transactions were printed, amounting to Rmb68bn, up 35% from the same period last year. Financial institutions have become the largest issuer type and in addition the tenor of issuances has also been better allocated.

Looking at the first half year of performance, there are some noticeable traits. For example, one of the world’s leading European car manufacturers successfully launched its Panda MTN and short-term notes, becoming the first European company to issue such bonds publicly. One of the leading supranational issuers in the region has issued Rmb2bn of Panda bonds in the interbank market, so that marks this issuer’s return to the Panda bond market after a hiatus of 12 years.

On Dim Sum side, it has been announced that China’s local governments will use RMB bonds in the offshore market for the first time. But this will be a noticeable test of the investment attractiveness to international investors. Local government issues with high credit quality from Guangdong province will be among the first batch of issuances. But these issuances are of great significance to the opening up of China’s bond market and interconnection in the Guangdong Hong Kong Macau Greater Bay Area. The market estimation of the annual issuance volume of Dim Sum bonds this year is at Rmb200bn.

Having summarized the above, we clearly find that from the perspective of cross-border financing, both China’s Dim Sum bond and Panda bond markets have been providing very constructive platforms and opportunities for issuers and investors. So in this regard, we believe that both of these two markets are mutually reinforcing, rather than competing against each other.

IFR ASIA: We’ve talked about how the market is providing funding options for international issuers. Are there any Chinese issuers that don’t get a good reception in the onshore market but have more options when they issue offshore?

IVAN CHUNG, MOODY’S: Yes, I think traditionally, because of tighter control of the property sector, many property developers as we have seen in the past several years are mainly using the offshore market to get financing, which as long as they’re willing to pay a higher yield is easier to for them to raise funds than the onshore market where they are subject to more regulatory scrutiny.

The other kind of company is the new technology or the new economy company, because traditionally the onshore market is more receptive to asset-heavy companies – companies like mining, electricity, and heavy machinery. At the same time, I think onshore investors are more sceptical about asset-light companies. For internet companies, in particular onshore investors feel less comfortable with the VIE structure, even though the regulator didn’t explicitly say that they couldn’t issue bonds. As far as we know it will be more challenging for them to go through the regulatory barrier and also get the market recognition.

On the other hand for an internet company like Alibaba or Tencent, international investors know them well, and also international investor have been investing in the equity and bonds for this type of internet company globally. So I think it’s much easier for them to access to the market and to attract more investment interest, and that’s why you see a number of the internet or technology players going to this market.

Another niche market is asset-light companies like the education sector. Previously they also entered the offshore market, but unfortunately they have had regulatory issues. So I believe for the new economy and these non traditional industries, it will be easier for them to go the offshore market given than they have a quite large presence and also international investors have more knowledge about these companies and feel more comfortable invested in them.

In the onshore market, it will be more gradual process. For example, JD.com has also issued a bond in the onshore market, but usually these issuers will issue offshore first and then go onshore, unlike most other companies that issue onshore first and then go offshore. I think the key thing is the development of a bond market that allows the investors and issuer to make more measured, calculated decisions to take the best advantage. I think that’s the key driver of an internationalisation that will benefit both issuers and investors.

IFR ASIA: China’s onshore securitisation market seems very different to the offshore market. What kind of solutions and innovative products are there in the onshore securitisation market that we don’t see offshore?

MARK LI, CICC: Official statistics show that from a global point of view, having a compound annual growth rate of around 50% in the last five or six years, China’s ABS market is indeed the fastest growing market in the whole world. That gives all kinds of originators access to the capital markets in China. Until the end of August 2021, the outstanding total size of China’s ABS market amounted to Rmb6.2trn. We have good reasons to believe that these numbers will reach Rmb7.4trn at the end of the year. Meanwhile if you look at the total issuance size of China’s ABS market in the year of 2020, it reached Rmb2.7trn. A 30% year-on-year increase is estimated to be recorded at the end of 2021.

China’s ABS market is therefore gaining ground to become one of the most important ABS markets, while being firmly on the right track to overtake many of our peers all over the world. Looking at the underlying asset allocations in 2021, we have seen the following new developments. Number one, the acceleration of green ABS issuances. According to the latest figures 29 green ABS products, with a total amount of Rmb42bn, were issued in the first half of this year, an increase of 25% over the whole year of 2020. In March, the first carbon neutral asset-backed notes and exchange-traded carbon neutral asset-backed securities were issued. Out of the green ABS products issued this year, 17 deals with a total size of Rmb31bn were for the purpose of carbon neutrality.

Number two, intellectual property ABS innovation continues to advance in China. Under the support of policy and market promotion, various intellectual property ABS were successfully issued, in order to help invigorate intellectual property rights, clearing the financing hurdles and burdens especially for small and medium sized enterprises. In the first half of the year intellectual property ABS transactions with underlying assets covering human capital, new generations of IT, high end equipment manufacturing and copyrights were issued.

Last but not least, China’s first public infrastructure REIT went on sale and officially listed on the Shanghai and Shenzhen stock exchanges in June. The first batch of products includes assets like modern logistics storage, industrial park and all the sub REIT underlyings, including highways, water treatment, water power generation etc. Being designed under the public fund plus ABS structure, China REITs mainly invest in infrastructure projects, distributed in the key economic areas of China for the purpose of activating the nation’s inventories of infrastructure, broadening the investor base and of course, in reaching the underlying investments.

IFR ASIA: Looking at the offshore market again, we’ve got the National Development and Reform Commission (NDRC) quota approval system, which keeps issuance under control. So how has that affected offshore issuance?

IVAN CHUNG, MOODY’S: I think it is kind of a system that allows them to control the pace of issuance and also divert some of the financing to certain sectors. Having said that, I think for the past few years, we can see the pattern is that the priority is to give quotas for refinancing, which is good news for both issuers and investors because they don’t want a situation where an issuer wants to issue a US dollar bond for refinancing and cannot get the quota. Whether there’s a market or not is another issue, but from the regulation point of view, I think the regulator is well aware of the fact that they need to do refinancing and that priority will be given to do it.

On top of that, you can see certain sector preferences. Our understanding from issuers is obtaining approval for green bonds will be easier, and also for certain sectors that will drive the economic rebalancing and the new economic development. Then for certain sectors that regulators have concerns about leverage, for example, like the property sector and LGFVs, where in particular this year they have regulatory guidelines and announcements talking about controlling the leverage in these sectors. The approval both in onshore and offshore markets will be mainly focused on the refinancing, and it will be more and more difficult for issuers to have incremental debt and new financing for both markets. So for both onshore and offshore bonds, regulators will take the same attitude and obviously it will affect the way that issuers get the quota.

Other than that I want to highlight another thing. As far as we know from the issuers, even though there are no explicit rules and guidelines, there are also some regional allocations. For certain provinces that may have less issuance it will be easier for them to get new quotas. Also within the provinces, it will be easier also for certain SOEs and LGFVs to get that allocation. On the other hand, for some provinces that have lots of issuance, it will be more difficult for them to get the quota. So there are lots of dynamics.

JENNIFER ZHANG, BARCLAYS: The NDRC quota mechanism, to a certain extent, has affected certain issuers in certain sectors. But actually across onshore and offshore, we’re seeing increasing credit bifurcation, which means there is going to be increasing performance divergence between the stronger issuers and the weaker issues. Some stronger names still have a lot of financial flexibility, so they can tackle both onshore and offshore markets. For weaker names, they’re facing a tighter funding situation domestically, and also it’s not easy for them to get the quota. For those issuers, I think they need to improve their leverage ratios. To a certain extent we’re not only talking about improving the ratios, we’re also talking about containing the overall debt scale.

IFR ASIA: What difference does it make to companies’ credit risk when they’re diversifying between onshore and offshore bond issues? Does it add to the credit risk if they’re issuing a lot offshore or is it a good thing because they’re diversifying their investor base?

IVAN CHUNG, MOODY’S: I think by definition, the rating reflects the ability to repay, and whatever currency and what market they are in the rating will be the same. For example, if you look at the MTN programmes of many issuers in the world they include multiple currencies and multiple markets.

I think for Chinese issuers in particular, if an issuer has access to both the onshore and offshore markets, our consideration is more on their ability to access funding. So, in certain cases, it will affect the credit rating because the ability to raise funds will be stronger and the liquidity will be stronger. That will be higher in our consideration rather than giving a preferential treatment or different treatment in a different market, because at the end of the day, we will look at the instrument. If it is senior unsecured then it will have the same treatment as any senior unsecured bond.

But if an issuer can access both markets, from our liquidity analysis perspective it will be good because both markets are not moving in sync and both markets have different investors and different market dynamics. It will allow them to do better financial management and liquidity management, which is a quite a positive for all the issuers.

IFR ASIA: Talking of diversifying the investor base, obviously, the US dollar is the main offshore funding instrument for Chinese issues. But could Chinese issuers make use of any other currencies?

JENNIFER ZHANG, BARCLAYS: We think away from US dollars, euros and sterling would be the two alternative funding currencies that Chinese issuers can consider. For some Chinese conglomerates who have operations in Europe, they naturally will consider issuing bonds in euros for natural hedging purposes. Actually, for some Chinese companies, they tend to do euro-dollar coupled dual-currency trades to build up the pricing tension and then to achieve the optimal transaction outcome. Then for Chinese banks, for those with branch offices in the UK, in London, naturally will think about sterling-denominated issues, again to match the local funding needs in the UK. That’s why we think away from the US dollar the euro and sterling would be the two alternative currencies they consider.

IFR ASIA: Mark, do you see Chinese issuers exploring other currencies offshore?

MARK LI, CICC: The latest number shows up until early September this year, the market inventory of Chinese offshore bonds has nearly 93% of the transactions being denominated in US dollar, while the euro gains the position of runner up at 2.7%, followed by CNH and Hong Kong dollar. According to Chinese bond issuance stats of internationalisation, there would be, for instance, other major currencies like Japanese yen and pound sterling, Swiss franc or any other emerging markets currencies to be considered, as far as the bond issuers could match it to their global business strategy and relevant operational standards of bond issuances in their market.

IFR ASIA: In terms of G3 issuance from Chinese issuers, Reg S only is the most popular format at the moment, which means that it’s not targeting US investors. But do you see a need or an opportunity for Chinese issuers to expand beyond the Reg S market?

MARK LI, CICC: Yes, I do. The total issue size of China’s offshore bond early September again in this year was US$188.2bn up from US$155.8bn in the same period of last year, so the year-on-year growth rate, was 21%, in which US$9.5bn of 144A transactions were printed. Actually, that was down from US$11.2bn in the year 2020. Therefore, for the Chinese bond issuers the Reg S format is still dominating, while 144A remains one of the possible choices, so the year-on-year change for 144A doesn’t sound so promising to me.

To many of the market participants involved this is a purely market-driven approach. For example, when investors ask for easier and low-cost structures, issuers are expected to respond positively. So regarding whether there will be any needs for Chinese issuers to diversify funding beyond the Reg S market, it would rather depend on investors as well as the operational efficiency of the relevant markets.

JENNIFER ZHANG, BARCLAYS: The short answer would be it depends, subject to each issuer in a specific situation. So nowadays for unlisted companies, the transparency and documentation hurdle for tapping the 144A markets is higher. So that’s why historically we have some of the unlisted Chinese conglomerates, even for jumbo size transactions, they’re doing that in Reg S only format, especially given that Reg S markets do provide the liquidity that those transactions would need.

Then on the other hand there are listed companies, especially TMT (technology, media and telecommunications) issuers, which may be listed in the US. They have an investor base there. So for them, traditionally, they have been tapping the 144A or SEC-registered format.

IFR ASIA: What is the outlook for China for defaults and are there any particular sectors at high risk?

IVAN CHUNG, MOODY’S: I think the context is that the default rate, in China but also in the offshore market, as a percentage of the overall market is still small. So we see high profile default cases as an increasing default trend. I think it’s quite natural, as the market becomes more mature and develops and there will be more and more credit differentiation. So we believe that more defaults will be forthcoming, but relative to the total market it’s still small because we believe that if the defaults can create some systemic risk or undermine socio-economic stability, the Chinese authorities will step in.

However under most of the cases, they will consider this as an isolated default and they can tolerate this default and also certain volatilities in the market. As you can see in the past year, in both the onshore and offshore market there have been SOE defaults that created certain volatilities and even affected certain regions. But overall, you will see that issuance activities continue, the market continues to trade, and both the investors and issuers have become more mature. And under those kind of short term volatilities, it means that from the Chinese authority and regulator perspective, they want to develop a risk-based market, they want to reduce moral hazard. So they will continue to allow certain isolated defaults to happen, including SOEs.

So what is driving the defaults? China is a high growth market with lots of liquidity, and most of the SOEs are well protected. That’s why we didn’t see many defaults until after 2017 and 2019, when we saw some defaults when China handled the overcapacity in the commodity sector. And over the past two years, I think the Chinese authorities, have been very clear that they will use a more market-oriented approach to deal with SOEs’ debt restructuring, meaning that bondholders may suffer certain economic losses.

There are lots of means and tools for the government to handle the volatility. For example, in the past, the government needed to pay out to ensure that there will be no market panic. But now they make restructuring plans that will ensure employment and consider the operations of the issuer. But at the same time, the creditor and the bondholders and the banks need to suffer losses, in a debt restructuring or debt-to-equity swap. So that scenario means that the government support may be more selective on certain sectors, but they also might let companies go, given the fact that they have hundreds of SOEs in the market.

We see gradually some SOEs will get less support, which I don’t think will be a surprise, as we can see in this past year those in the commodity trading and fragmented commercial sectors that are fundamentally weak may not be able to refinance. In the past, because of the SOE background it was easy for them to borrow a lot. But now, the government may not support them, as in the past, and more importantly, investors realise that they have become more selective in providing support to them. And as a result of that, they may not be able to refinance and eventually get into liquidity trouble.

Another sector that we see that may be under more pressure is the property sector, I think for obvious reasons. Now, the central government is tightening the leverage in the sector and tightening additional borrowing in the sector. Investors see a couple of default cases happening, they become more risk averse, and so they become more selective in investing in these sectors. And SOEs such as those at the tail end have difficulty getting refinancing. On top of that, for the property sector, we have a negative outlook because of the tightened regulatory conditions and tightened funding conditions, which will not only affect property developers, but also homebuyers, because it’s getting more difficult to get a mortgage to buy a house. Also, the interest rate is higher.

All this will affect the fundamentals of property companies making them more vulnerable, plus the fact that they are all highly leveraged. But across the board, I think that the development and the evolution of the credit market means that there will be more weaker names that will be vulnerable, and we believe there will be more defaults. Having said that, if you look at the onshore market, the total amount of defaults there is less than 1% of the corporate bond market, and in terms of the number of issuers it is also less than 1%. The offshore market is a little bit higher, but it’s small.

I think the risk that these defaults become more serious and will affect the whole market is low. If certain default events become much bigger and have a contagion spill-over to the overall market that may create systemic risk and in that scenario, we believe the government still has to intervene, but they will tolerate some volatility if there are isolated defaults.

IFR ASIA: One of the most significant defaults in the last couple of years was Peking University Founder Group, as the court during the restructuring ruled that offshore bonds using the keepwell deed structure were not counted as claims. So what does that mean for the role of the keepwell deed structure in offshore bonds?

IVAN CHUNG, MOODY’S: I remember many years ago when I attended a roundtable to talk about the keepwell guarantee structure when the keepwell began to emerge in the market, I used this example: a guarantee structure is like a marriage certificate. If anything happens, you can go to court and the court will accept it. But the keepwell deed is like a love letter. It’s a commitment, it’s evidence to show the relationship, but whether the court will take it at face value or really consider seriously is a question mark.

I think it has been proven that a keepwell deed is not a type of discounted guarantee, it’s just a commitment to provide support. It works, particularly when the issuer is in good shape and they want to get financing. Particularly in the past when there were some regulatory barriers for them to issue offshore, keepwell was the alternative to convince the market that the parent company is willing to provide support. But in a liquidation scenario, as we can see in recent cases, it has opened uncertainty about how the court will treat it for a senior unsecured bondholder. I think the Peking University Founder case has shown it has limited protection.

We really need to look at the context and the situation to decide whether it can really provide support. At the end of the day it is still all about the ability and the willingness of the parent company to provide support, because the keepwell, as far as it is proven, is not legally binding as a guarantee. Now that more Chinese companies are able to get an NDRC quota to issue bonds using a direct guarantee structure or direct issuance structure, there will be less issuance of the keepwell structure. I also believe that on the investor side, given the recent incident they will be more selective in investing in keepwell bonds, and the keepwell structure I believe will become less and less in terms of the total amount. If an issuer can issue a guaranteed bond and they issue a keepwell bond instead, we need to understand the reason why – whether it is a willingness issue or other structural issue like a regulatory issue that means they have to use the keepwell structure.

IFR ASIA: What do you think will be the role of keepwell deeds going forward and what kinds of issuers will use them?

MARK LI, CICC: The history of the keepwell deed could be traced back to 2013. The cross-border debt transactions using keepwell deeds generally require companies to provide support to their overseas subsidiaries, in this case, issuers, promising international bond investors that those issuers will keep appropriate level of assets and liquidity from bankruptcy. Nevertheless, just as Ivan correctly mentioned, the keepwell deed is not a guarantee and does not give bond investors any rights to directly claim the parent company to repay the principal and interest of the bond. Investors may, however, seek legal support under the deed if the parent company fails to meet its obligations to keep the issuer’s financial condition.

Secondly, according to the statistics of one of the global rating agencies in May 2020, some US$96bn of keepwell deed attached bond inventories were recorded. However, since September 2015, after the examination and approval system of China was replaced by the registration rules for foreign debt issued by Chinese issuers, as well as additional cross-border regulations being announced in January 2017, the necessary credit enhancement facilities like keepwell deeds have been decreasing. According to official numbers of NDRC, in 2017, the total keepwell deed related issuances amounted to US$32.3bn. These annual numbers were then lower at US$30bn in the year of 2018, and then around US$25bn, or below that, since 2019. The compound annual change rate shows minus 6%.

Between July 2020, and June 2021, 65 keepwell related bonds with a total amount of US$20bn were launched. The issuers were mostly financial institutions, while others were local government owned enterprises in some of the most developed provinces with a combination of keepwell deed plus guarantee or standby letter of credit. So you’ve seen the keepwell deed is not only playing a sole role, it has to play together with the others. Together with many alternative credit enhancement facilities, we believe that the keepwell structure is still playing a certain role, especially among those inventory trades.

JENNIFER ZHANG, BARCLAYS: I would agree there’s going to be a smaller issuance volume for the bonds that are supported by the keepwell structure. But I think from the investors’ perspective, for sure, they’re going to apply additional scrutiny when they’re evaluating the keepwell structure. We think they are going to look deeper at the underlying credit, they’re going to reassess the strategic importance of the offshore subsidiary to the onshore keepwell provider. And then they’re going to do analysis related to the onshore keepwell provider’s willingness to pay and their capabilities to pay especially under the FX capital controls in China.

Also if we’re looking at pricing, we think the keepwell premium is going to diverge subject to the parent distinction. Lastly, in terms of keepwell structures, probably some enhanced features will be added, including an extra account, basically investors asking the issuers to keep a couple of coupon payments under an account related to the transaction.

IFR ASIA: Now let’s look at China’s green bond market, another area of huge growth. So, Mark, you touched on the carbon neutral ABS, but what developments have there been in China’s green bond market?

MARK LI, CICC: We firmly believe that China’s green and sustainable market has a very promising future. In the year of 2019, for instance, Chinese issuers issued a total amount of Rmb386bn, which is US$56bn of labelled green bonds in domestic and offshore markets, with an increase of 33% over 2018. From 2020 onwards believe we believe that the growth rate will be even higher in the context of global challenges of global climate warming, as China shoulders the international responsibility of achieving carbon neutrality and carbon peaking targets, and we began to carry out our own energy and industrial structure overhaul facing unprecedented financing needs.

In this regard, China has been constantly exploring more subdivided green themed securities, such as climate bonds and transition bonds. Under the guidance of the long-term goal of achieving carbon neutrality, we are sure that the financing demand for green and sustainable financing will be large. We already have a hugely existing deal size from China. The size of green bond issuance in China has been maintained at more than Rmb200bn in recent years, and continued to increase rapidly. According to the Climate Bonds Initiative and other international organisations, China became the world’s largest climate related bond market in 2018.

China’s green and sustainable financing has broad prospects in the future. 2021 will be the milestone year for the issuance of China’s green and carbon neutral bonds. It is estimated that the amount of relevant issuance in China may reach Rmb5trn–Rmb8trn in 2021, accounting for 20% to 25% of the whole world.

China’s goal is achieving complete carbon neutrality, so the supporting government policies will be beneficial to the market environment. What we’re seeing is that while the investment concept of ESG at home and abroad is becoming more and more popular, the market demand is increasing day by day.

IFR ASIA: From the offshore market point of view, how do you see Chinese green BONDS growing to meet the national carbon neutrality goal for 2060?

JENNIFER ZHANG, BARCLAYS: In the offshore space, there are a couple of recent themes that we have seen. In the ESG space, we think corporate issuers are becoming more sophisticated, and many have published very well defined ESG strategies. Some early movers have released a carbon neutrality plan, and some are even committing to specific ESG targets. Previously in the offshore green bond space, we have seen green bonds, blue bonds and social bonds. Later on we are probably going to see the offerings in the sustainability-linked bond format. With these type of offerings, there’s no limitation on the use of proceeds, as long as issuers are committing to a certain set of ESG key performance indicators.

We’re seeing broader corporate participation in the ESG space, specifically from Chinese real estate developers and TMT companies who have tapped the green bond markets. Going forward we think the issuers from other sectors, even including non-traditional sectors, would tap the ESG space. Issuers in the high energy consumption sectors might be interested in doing transition bonds.

From the investors’ side, we think they are paying more attention to responsible investing. Some investors are doing very extensive due diligence work, evaluating ESG credits and asking very targeted bespoke ESG questions. We definitely think responsible investing is becoming more and more important from the global investor perspective.

IFR ASIA: Do you think the Chinese ESG bonds attract different kinds of investors compared to regular bond issues?

JENNIFER ZHANG, BARCLAYS: There are some independent dedicated ESG funds that can only invest in ESG eligible assets, and there are also some ESG funds at the global asset managers. So for example, Fidelity has their typical funds, and they also have ESG dedicated funds. So if the bond issuances are in ESG format, then the issuers can access this additional liquidity.

IFR ASIA: In the light of recent high profile defaults, do you see that there could be new bond listing rules or stricter official oversight or disclosure rules for Chinese bond issues?

IVAN CHUNG, MOODY’S: I think this is not necessarily due to the default cases – as I said the regulator has expected some defaults will be happening. But Chinese regulators are still trying to improve the disclosures as you can see in the past few years. In the onshore market they introduced covenants and better bond documentation, or creditor committees to handle debt restructurings. I think the default cases will not affect the listings, but will affect certain arrangements after default. There is still a learning curve, but you will see more transparency on these things although there are still some teething issues like treatment between onshore and offshore bondholders and other things. You can see that they are gradually developing some mechanism for investors and the issuers to negotiate restructuring.

I believe there will be more developments, but in terms of the listing requirements, I don’t think they will change given that currently they focus more on disclosure. Although there were other issues over the past few years, I don’t see there will be material changes. As a matter of fact, the regulator has also highlighted that they are improving the market environment, but they are not the gatekeeper for the credit quality of the issuers.

IFR ASIA: Will we see more public issues of Panda bonds, compared with the placement type format?

MARK LI, CICC: Yes, we are going to see more Panda bond issuances. We are going to see all types of Panda bond issuers, along with the internationalisation process of the renminbi.

IFR ASIA: Which sectors and industries from China will see more ESG bond issuance in the next year?

JENNIFER ZHANG, BARCLAYS: The green bonds issued by Chinese developers have got lots of traction from the international investor space, and also sustainable bond issuance from Chinese TMT companies has been very well received by offshore investors. Going forward, we think some issuers from sectors such as the industrial and consumer sectors will join the ESG camp.

IFR ASIA: Do you see more covered or secured bonds being issued?

MARK LI, CICC: Yes, we’re going to see some covered bond issuances. We’re going to broaden the underlying assets for investors.

JENNIFER ZHANG, BARCLAYS: Chinese financial institutions have issued covered green bonds before offshore. Going forward, we think the issuances will be subject to market conditions and a structure premium.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com