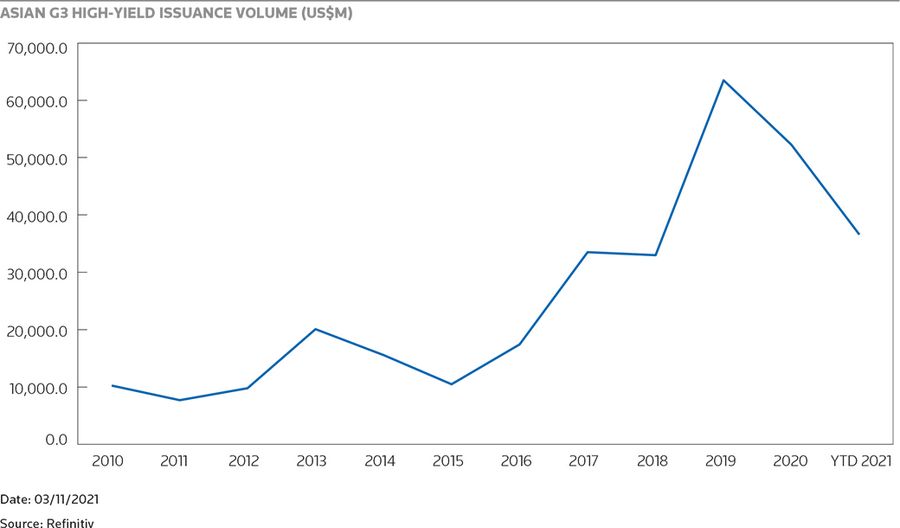

IFR ASIA: High-yield issuance from Asia has been on a hot streak in recent years, but the current market conditions are the most challenging since the taper tantrum in 2013. Last year, there was about $60bn of high-yield G3 issuance from Asia, but that was down about 20% from the year before, and this year’s volume is down on last year.

Chinese property companies have traditionally been the dominant issuers in the Asian high-yield space, but with concerns around companies like China Evergrande Group, which is not in default at the time of this roundtable but appears to have missed some of its coupons, combined with China’s tough policies on debt levels for developers and offshore bond issuance, there may be a bit of a change to the status quo.

Sibo, what does the investor base for Asian high-yield bonds look like, and is Chinese investor demand important?

Sibo Feng, CICC: Around half of the high-yield bond issues in Asia are from Chinese issuers. This year, a little bit less because of the decreased issuance in property bonds. As you mentioned, a big proportion of issuance is by the Chinese issuers, so naturally Chinese investors are big players in this space.

Locally, within that space, the majority of them are fund managers, asset managers and hedge funds. The rest, I would say, are split among private banks, corporates and some banks, but that’s a general landscape.

Obviously, this year the participation was a little bit less particularly as the property bond market issuance was less, especially for the second half. But we also see a growing demand for investors for the non-property space in high yield and going to the non-China high-yield space.

IFR ASIA: Deepak, are there more global institutions becoming relevant in Asian high yield?

Deepak Dangayach, UBS: What we have seen is most global institutions have either dedicated Asian bond funds or China high-yield bond funds. For example, you have Fidelity, our own asset management arm, HSBC, BlackRock and all those global asset managers.

All of them have dedicated Asian or Chinese high-yield bond funds, and those are a pretty important part of the investor universe for Asian high yield buy in. To Sibo’s point, most of the high-yield issuers print in Reg S-only format, not 144A, and that just shows the kind of investor demand and liquidity that we are seeing in Asia, not just from Chinese investors but from global institutional investors as well.

IFR ASIA: The Chinese property sector has traditionally dominated Asian high yield, but is there potential for issuance from other countries or other industries?

Sibo Feng, CICC: As we all know, it’s been a dominant part, especially with the Chinese issuers in the past within the property sector, but this year, both onshore and offshore, there has been materially less. Given the tightening policy environment and more property developers have high refinancing risks, year-to-date the net financing volume of property sector has shrunk a lot.

There are indeed other options in the Asian high-yield market, but it seems investors find issuance from other countries and industries to be relatively expensive at this point.

IFR ASIA: Deepak, what are your thoughts on the potential for new kinds of issuers to target the high-yield market, particularly from around the region?

Deepak Dangayach, UBS: The high-yield market is gradually maturing to an extent where you would see new sectors and new structures coming in. Specifically, in the last couple of years, you would have seen project high-yield bonds coming out of South-East Asia.

The first project bond that we saw in the Asian high-yield sector was from Studio City in Macau. It was an interesting transaction, but after that it took some time for other project bonds to come in. But I think we will see a lot more structured transactions coming out of Asia for the high-yield sector, as well as newer and newer sectors.

Typically, as we all know, the market is dominated by China’s property sector given the funding dynamics out there. But, as the companies across Asia mature and they’re able to access capital markets, they should offer competitive, flexible terms to the bank market that then typically uses the funds. So, you will see a lot more Asian issuers coming in. That has been shown in the volumes coming in. In the last 10 years, the volumes have substantially increased.

IFR ASIA: Monica, from the buyside perspective, would you like to see more diverse issuance?

Monica Hsiao, Triada: Definitely. After this year, I think everybody wishes that there was a broader diversity, not only by region but also sectors. For a few years, there was little market appetite for China industrials because a number of them had problems with either payment or transparency.

Similarly, for a long time until this year, the market had a preference for property developers in China, because people banked on higher recovery seeing that they had assets, there were bricks and mortar that they could see. But I think after this year, it’s been a lesson for everybody about the ‘lack of transparency’ in this sector because no matter how much work you do on paper, there are things that are unknown off balance sheet. This year, policy tightening measures have brought such issues to light.

We would look forward to seeing more South-East Asian issuers. We are starting to see some property developers come out of countries like Vietnam but we would love to see issuers from more diverse industries.

Some project structured bonds have come from renewables or the energy space, but we could see that eventually come from China property as issuers may have to become more creative about finding a structure that is more appealing in order to return to find funding in this market.

I would hope that investors and bankers will be a lot more stringent about covenants and the structuring to require more security backing or more protective measures after what we’ve learnt this year.

IFR ASIA: Sibo, we’ve talked about Chinese issuers selling offshore high-yield bonds, but do you see potential for an onshore high-yield market to develop as the domestic ratings are reformed and foreign investor interest in the onshore market grows?

Sibo Feng, CICC: Yes, we do. In fact, the onshore market is actually developing quite rapidly. Last year, the outstanding amount was over Rmb600bn, according to CICC research, and with the gradual removal of implicit guarantees, of guaranteed payment, the analysis of the domestic credit investment is more driven by credit fundamentals now. So that’s an important development.

If we look at foreign participation, it’s only about 1% of the onshore credit market. A lot of the foreign investment through the bond market has been in the government bond and the policy bond space so far.

In terms of reform of the ratings, we see that a bit of remodelling has been going on the domestic rating landscape. We see international rating agencies going into the onshore market, and things are going in the right direction.

According to CICC research figures, the size of China onshore high-yield bonds has been increasing in recent years with the number of high-yield bonds at 679 and a total outstanding size of Rmb641.3bn as of the end of 2020, according to China Money magazine in February 2021.

With the gradual removal of the implicit guaranteed payment for China onshore bonds, the domestic bond market has progressively returned to be fundamental credit driven. Also, taking into account the foreign holding represents only 1% of the total size of China domestic credit bonds, which shows a remarkable growth potential, we see great opportunity for the development of China high-yield bond market.

It should point to a monumental market opportunity.

IFR ASIA: Kenny, How has your bond investor base changed in recent years?

Kenny Chan, Zhenro: Before the current turmoil, I think our investor base has been improving very well. Historically, if you look at the past three to five years, private banks basically contributed around 3% to 5% of the whole field. Investors in Asia, including Singapore, Hong Kong, mainland China or even South Korea, altogether contributed around 60% to 70%.

But what I would like to draw to your attention to is that in the past two years, especially where we started doing our first green bond, I saw a significant increase in investors in Continental Europe. We have talked to many banks, many institutional investors in Europe, and we have frequent coverage in Germany, Switzerland and London.

But after the Evergrande case happened, definitely some of the investors panicked. Overall, if you look at the situation, I think investors in Continental Europe or even in the States are more panicked because of the different time zones and because of difficulties in getting access to information.

If you look at the past few days, most of the sellers are from Asia, but if the markets recover or if the markets become more stable, I think the overall investor mix will be back to the normal level, which is 5% PB, 60% to 70% Asia, and then the remaining will be back to Europe again.

IFR ASIA: Sticking with the green bond angle for a minute, does issuing the green bond introduce different kinds of investors that you don’t normally get for high-yield issues?

Kenny Chan, Zhenro: I still remember when we did our first green bond. The overall feeling was tremendous. In normal situations, the number of investors is ranging from 100 to 200, but when we launched the first green bond this year, or even last year, the number of investors reached over 300.

We have many good investors from Europe, and also some institutional funds in Asia even have separate desks to buy ESG bonds within the bond funds. Before the current situation, I think there will be clearly more investors that are interested in ESG products, but right now, it’s really hard to say.

IFR ASIA: From the issuance side, what are the advantages for high-yield issuers to issue green bonds?

Sibo Feng, CICC: China has become the second largest green bonds market with cumulative domestic green bonds issuance volume of Rmb1.1trn as of the end of 2020, according to Wind data.

Along with China’s carbon peak and neutrality targets, China onshore investors are getting more interested in ESG themes for investment. The issue yields of 66% of China onshore carbon neutral bonds are relatively lower than the other bonds with similar ratings and tenors.

On the supply side, there could be increasing policy support for issuers to issue green bonds, for example to speed up the process of green bond issuance and encourage ESG investments. For the demand side, more indexes and ETF products can be developed to foster the development of green bonds. We see there are more opportunities for Asian high-yield issuers to issue green bonds with the increasing demand.

So far offshore Chinese green bonds issuers are mostly financial institutions and property developers. We expect the high-yield green bonds market to expand further as the disclosures are standardised.

The amount of money that is coming into this space is growing, and we know a lot of funds are setting up green bond and ESG-themed or dedicated funds. We are definitely seeing issuance of that kind of product to meet that demand and meet the various global green targets.

IFR ASIA: Deepak, what potential do you see for green bond issuance from Asia high yield?

Deepak Dangayach, UBS: Green bonds or ESG-related bonds have made progress in the last few years. What we will see is these bonds commanding a premium to the regular ones as well, just because of the dedicated pool of the investor base.

You will see more and more investors only investing in ESG or SLB bonds. I would expect that this market will continue to grow, but for it to grow further you also need to have a more standardised set of parameters for some of these bonds because, currently, the parameters are still evolving. I think you will see that part of the market evolve further so that investors can objectively assess one ESG bond against another.

IFR ASIA: Obviously ESG involves deeper reporting, but Annalisa, how strong are Asian high-yield bond covenants compared with the rest of the world?

Annalisa Di Chiara, Moody’s: Some of my comments are probably just going to be really geared towards some of the work that we do on the proprietary analysis of our covenant team at Moody’s, which scores the covenant packages. We’ve scored over 400 bonds.

From a global perspective, Asian bonds still remain strongest in terms of debt protection measures and covenants. North America is the weakest, and then the EU and LatAm fall somewhere in between the two. The question is: “Why is that?” Really, it’s driven by the market and the issuance.

In North America, issuance is heavily influenced by private equity, and as you all know, the MO for private equity is to extract value and to also leverage entities up. And to do those two things, they need to have flexibility in their covenants. That sort of drive has not only affected PE-led deals, but it has also included non-PE deals in North America

Nonetheless, globally what we are seeing is a very consistent trend of weakening credit quality. So while the Asian bonds still have the strongest protection, there has been a weakening trend, and that, largely, has been driven by the influence of the China property sector, which has obviously accounted for a great deal of the issuance.

Repeat issuers that come back to the market tend to look for a little bit more flexibility in their covenants, and they are getting that. So the trend, globally, is weakening. It’s not unique to Asia, but it is global on the covenant front.

IFR ASIA: Monica, do you think there a need for stronger covenants in Asian high-yield bonds or is it just simply a matter of needing more transparency?

Monica Hsiao, Triada: We touched on this last year in the roundtable about the need for covenants, which I don’t think the buyside community here demands enough of. But I think the bigger problem is the lack of transparency which creates a lack of market confidence. This comes down to the willingness of issuers themselves to offer transparency to investors, because it really doesn’t matter what we have on paper as covenants if their financial reporting may not even include relevant data or if you can’t trust management disclosures in public conference calls, for example.

On the transparency side, the issuers have to come to terms with the fact that their willingness to engage in an honest way with investors – their trustworthiness – should have a direct impact on their ability to maintain market funding channels and reduce their cost of capital. Merely having financial covenants with metrics that they have to meet in an offering circular is pointless, when it still is a matter of what goes into that calculation, what’s behind it, what’s included, what’s not included, so ultimately issuers have believe that their behavior is correlated with their ability to tap markets, and this has to be encouraged through the market’s own discipline and demands.

IFR ASIA: Obviously, this has been a tough year for Asian high yield, especially for Chinese issuers. So how has Zhenro been able to maintain access, and have you done anything differently in your investor relations this year?

Kenny Chan, Zhenro: Zhenro has been diversifying our funding channels, and we have been doing it successfully. If you look at three years ago, our bond price was about 13% and the tenor was around two years.

We only have US dollar bonds, but as of today, we are one of the top 10 US dollar bond issuers in my sector, and we have funding channels that are very diversified. We have US bonds, we have Asian bonds, we have green bonds, we have syndicated loans and bilateral facilities.

So I think our funding channel is well diversified enough, but it’s really hard to talk about printing paper again because, right now, it is a matter of trust. But I truly believe we can go through this turmoil together. I think the good companies will definitely stand out.

If we can maintain transparency, I think people will trust us and will support us in the medium to long term. No matter what, I think my sector will still be very keen to find new funding channels. But for Zhenro, we are very diversified.

IFR ASIA: Obviously there have been a few issuers who have managed to come out against this market backdrop, but what kinds of new issue premiums have they had to pay to clear the primary market recently?

Deepak Dangayach, UBS: Obviously, the current market backdrop is not constructive, so high yield will take some time, especially out of China, to recover. But the new issue premium is actually a factor of the broader macroeconomic outlook. So, earlier this year when the market was at its strongest, you actually saw negative new issue premiums going through.

Then, during, say, July or August, you saw new issue premiums that actually rose up to 25 to 50 basis points for some.

For investment grade, typically we were able to pierce the curve, but now you’re seeing 10 to 20 basis points new issue premiums as well, depending on the credit curve. I would say that these new issue premiums are a factor of the broader macroeconomic outlook, rather than just a standalone number.

IFR ASIA: Monica, in the current market conditions, how has the market differentiated between the different kinds of credit this time compared to prior dislocations?

Monica Hsiao, Triada: It’s very clear that the dislocation has been widening dramatically between China and the rest of the regions, but also within China high yield, the Single Bs and the Double Bs are worlds apart, although the Double Bs are starting to get hit too. At some point, everything falls in contagion if fear spirals.

I think that our markets are beyond talking about anything fundamental anymore. We’re in a vortex of fear, as everybody who follows the China market knows right now. We are really going through the eye of the storm, and I think that we’re at a point now where just about any rumour, talk or speculation (whether true or not true) will cause bonds to move 8–10 points.

Unfortunately, some of the short sellers in our market are not like the Muddy Waters of the world. There isn’t necessarily a basis of deep analysis, but there’s a lot of talk, there’s a lot of rumour mongering. Some are true, some are not true, but it’s very difficult for people in the market to separate fact from fiction sometimes. As a result, there is just this herd mentality, and everything gets thrown out the door.

At some point, hopefully, the market comes back to some sense of sanity. I think it’s consensus now that we won’t see a broad-based policy relaxation anytime soon, if ever, because I think that the deleveraging trend and what China wants to do for the property sector has been made fairly clear at this point.

However, we are seeing signs of some mortgage easing, some policy easing in select cities or provinces to help cash collection. All of this so far hasn’t made much of a dent in the fear that the market has right now, but I think at some point there will be some normalisation, even assuming a status quo on current policy – which means that things don’t get tightened more, but maybe ease or adjust a little bit.

Even at a policy standstill, it’s down to the market decide when to settle down to return to think about fundamentals, to assess about what each issuer can or can’t do. It’s difficult for people to imagine that right now because we’ve had not only Evergrande but we also had an example like Fantasia, where they seemed to have the ability to pay and they had said publicly to investors that they would pay as well. Then at the last minute they decided not to. So assessing whether a company has that willingness to fight through paying each tranche has become more difficult in light of this tough policy environment.

Fantasia’s default case was in many ways more damaging to market sentiment than a case like Evergrande. It caused everybody in the market to question, “What can we believe from any issuer?”

I think that has changed our landscape. When you say, “How do you differentiate?”, when we used to think about relative valuations – now we wonder if there a “fair price” really? Because there’s a point right now of fear where some think there is no right price to determine if it’s cheap enough.

You dump at 60, you dump at 50, you dump at 40. If you look at our bond prices, a few weeks ago, I was saying, “Well, there should be some pickings here,” when 30%–40% of our bond world traded at 80 or below, 75 or below. Then, it became 60 or below and then even 6–8 month bonds fell into that zip code.

At some point, do people take a step back and think the levels are getting insane for even the performing credits? We all understand that this sort of negative loop has created a fundamental situation for issuers whose bond curves make it impossible for them to return to markets anytime soon.

Then issuers may just default voluntarily to just try to see what happens, and we don’t always have clarity or a standardised process on what happens post-default. You don’t have the predictability of a process that we have in more developed markets as in the west.

Hence we are in this no man’s land, where any bit of fear will send everything spiralling. I personally believe things eventually will normalise as is the case in any market, however painful it feels right now. Eventually, this should become an investable market again, but at this very moment, our market is very, very broken, so the differentiation isn’t with much logic anymore. It’s just black or white, and it becomes very emotional.

For bonds that are higher risk, some issuers can still have enough liquidity, or monetise assets or raise equity but I don’t think there’s much patience from the buyside to analyse this because of a general lack of confidence in management guidance or ability to execute so all the Single Bs get sold out together. The short sellers and dealers know this so it’s easy for them to push on fear.

I think we as an investor community have to think about how we want this differentiation to occur. Do we give so much power to the bloggers, the motivated short sellers, the people who can be momentum pushers? That’s a choice because I think we have given that power to that segment of the market and it has broken our markets. It hasn’t been good for anyone who wants the market to be an investable asset class in the longer term.

IFR ASIA: It sounds like the market is pretty broken. Deepak, how long do you think the primary market will be frozen?

Deepak Dangayach, UBS: That’s anybody’s guess, but you will start to see some of the investors’ concern and scepticism go away. What can bring the market back is an orderly restructuring of some of the names that have defaulted.

We expect a lot of liability management exchanges to come through the market. We’ve recently seen a couple of Chinese issuers looking to extend their maturities and doing liability management exercises. But, more importantly, some of the other issuers who have maturities far off would proactively look to do liability management exchanges just to fill a little bit of investment confidence. We would look to see that part of the market gradually pick up before you see more new issues, especially on the high-yield side in China.

On the flip side, I think you will see some issues in South-East Asia and India on the high-yield side keep coming, even though the situation has elevated other levels as well. But for China, you would probably need this market to heal before we can see new issues.

IFR ASIA: Annalisa, what could the consequences be for corporates if the primary market stays frozen for a while?

Annalisa Di Chiara, Moody’s: Refinancing risks are already rising. If I just speak to the China property sector, they’ve got about US$40bn worth of offshore bonds maturing through this environment next year, so we could see more defaults. We could see, potentially, a pick-up in distressed exchanges. I think those are the two obvious risks.

Going back to some of the comments that we heard from Monica and Deepak in terms of what could reignite the market here, I agree with both of their comments. It is an emotional market at this point in time.

There are and there have been companies that have been fundamentally sound that have been challenged to access the market. When they are accessing the market, they’re being strapped with higher coupons or shorter tenors. Again, that also is building another risk into the high-yield sector, where we’ve got companies that are needing to tap the markets more frequently on a perpetual basis.

Given some of the comments that we’ve heard today, we know that this market is a bit sensitive to non-fundamental factors. So it really is changing the dynamics of the high-yield market, and we’re also continuing to see a flight to quality. But how do you define credit quality if investors are basing their investments just on emotion?

So it’s a challenging time for the high-yield markets, and I think we’re going to have to see more transparency. We’re going to have to see some more transparency on restructurings. What happens with the recovery prospects for onshore lenders versus offshore lenders and vice versa?

Those are just some of the things, but the situation we are in right now is certainly elevating liquidity risks.

IFR ASIA: Are there any particular sectors that are under pressure? And how have the downgrades versus upgrades looked this year?

Annalisa Di Chiara, Moody’s: Not surprisingly, China property is under a bit of pressure. That’s interesting because that has been one of the more stable markets just because, from a fundamental perspective, there’s been a lot of growth and support. From a policy perspective, there’s been a lot of support, and we’ve looked through refinancing and thought that the market would handle it because the appetite was so strong.

So that sector has come under a little bit of pressure. Our South and South-East Asian regional corporates are also still under a bit of pressure, and that’s because they actually were hard hit through the pandemic. Some of those companies are still climbing out of the lower end of the rating scale and trying to restructure.

But aside from our focus on China property at the moment, I think there isn’t any real concentration. I think what is really causing some of the pressure is, obviously, access to liquidity, access to the market and refinancing risks.

We are continuing to see that bifurcation between lower-rated companies and better quality Ba companies. And obviously, the risk is more for those Single B ones. I think through September, we’ve already seen about 36 downgrades – again, a little bit more for property than other sectors – and that compares to only 12 upgrades this year. So that gives you some sense of where the momentum is.

Compared to the downgrades we took through the pandemic through 2020, we were up just above 50. So we’re already at 36. That compares to a pandemic nearer 50. There are probably a few more negative actions, however we want to describe them, to come because of liquidity situations. But we’ll have to see where we end up in the rest of the year.

IFR ASIA: Kenny, it’s not just the primary market conditions that you have to worry about as an issuer. How have the tightening Chinese regulations for property developers and tighter NDRC quotas affected your funding strategy?

Kenny Chan, Zhenro: For Zhenro, we have returned from yellow to green, and I think the majority of my peers could turn to at least yellow or even turn to green by the end of this year. I would say the majority of my peers could do that because the Chinese government has been talking about the leverage for months or even for years.

If you look at the past 15 years in my sector, there were three turmoils, and on average, the overall recovery took from six months to 12 months. Taking the Evergrande as the fourth turmoil, which happened in around May, I think that by the end of this year, I don’t expect the central government would loosen the policies. I think they would still request all the key players to behave or even to fulfil the required three red lines.

If you look at the first interim reports, many of my peers have already fulfilled the requirements. If you look at the past 18 months, because of Covid we couldn’t commence our previous activities for five months from January last year, and it really drew our attention and frightened us.

So starting from last year, the majority of my peers started doing all the cash-sale activities, and it successfully brought down the overall net gearing ratio. This year, we understand that the 345 rule will be very critical for developers. If developers fail to meet this guidance, they may not even be able to get sufficient LTV for the cost of the loans.

Even if we look at the offshore market, the syndicated loans market, the financial loans market or the bond market, investors and banks have started voicing their concerns on liquidity. They have also voiced their concerns on leverage.

We are pretty much done with the 345 requirements, except those companies who still fail to meet them by the end of this year need to speak up, otherwise they may feel liquidity problems in the local market.

IFR ASIA: It sounds like Zhenro has got everything under control, but there are undoubtedly some Chinese property developers that are facing a maturity wall next year. Deepak, what do you see happening there?

Deepak Dangayach, UBS: In the next 12 months or so you’re seeing something like US$47bn of China high yield coming due. That’s a big number. A lot of them, if they’re not able to refinance, will either have to find an alternative funding source or look to do an exchange to try and extend the maturity.

Whichever way you look at it, there is a huge maturity wall, and the longer this funding window remains closed, the more issues that it creates for this maturity wall.

In the last 12 to 24 months, you’ve seen a bunch of issuers looking to do 364-day bonds, and that also led to a maturity wall because you need to refinance all of those. So that’s why a lot of issuers have to proactively think about liability management and exchange some of these bonds and extend the maturities.

IFR ASIA: From the investor side, Monica, what kinds of risks do you see from this maturity wall?

Monica Hsiao, Triada: The reality is that it isn’t just what we can see on the reported financial statements. That’s what the market used to rely on, for both unrestricted cash and debt maturities. We don’t really know the true maturity wall because there are a number of companies who have done private bonds or private wealth management products that may be off balance sheet and that sort of thing. Then the cash shown may not be as accessible as they guide to you even on public investor conference calls.

On the other hand, when you’re pricing over half the market as nearing default – I would argue that a lot of it has been priced in because on some names you can discount heavily the unrestricted cash and still see some headroom over the next few quarters such that they can buy time to execute on asset sales and if not, the pricing isn’t far off from potential restructuring value.

The fear that’s being priced in right now is that almost every Single B can default next year and we should differentiate a bit more amongst those names.

All this is premised on policy changes ahead because we would have to really analyse by the end of this year whether the market is going to be closed for three months, six months or 12 months. Whatever diversification of an issuer’s funding channel, I don’t know any high-yield issuer who can be frozen out of the markets forever. Every developer even in BB relies on refinancing in capital markets eventually.

This year we actually had reduced net bond supply, because of the markets freezing up in the second half of the year and because of the redemptions, as a lot of the companies are paying from their own operating cashflow.

So next year, assuming the market normalises, you may end up very well with a situation where Chinese high-yield bonds, the ones who get through it, will become rarer and rarer. Then, eventually, the chase for yields will come back at one point because the market tends to have a memory of a goldfish.

For the property sector, which is really the main focal point of the whole Asia market right now, we will, hopefully, get a little bit more clarity on the direction sometime before the end of the year as we see what it is that the government might pronounce.

So there is a big part of it that’s technical in addition to the generalised fear that this market has to wade through. From the buyside, the market sentiment and technicals really feels like the global financial crisis right now.

IFR ASIA: Annalisa, so it feels like high-yield issuers earlier in the year were issuing shorter and shorter tenors. So that has created a vicious cycle and are there concerns for refinancing now?

Annalisa Di Chiara, Moody’s: Yes, that’s what I think. Obviously, the investor sentiment is impact-driving the shorter tenors, particularly for the riskier credits, and that’s also coming at a higher cost. So issuers themselves are feeling a double whammy, both in terms of higher costs and higher cashflows going out the door to service debt and then also lining up for that perpetual need to access the market and refinance.

Refinancing is the key driver of issuing bonds here in Asia. So again, it’s going to be causing pressure for some of our weaker credits that can’t access the market. The longer they can’t access the market, the higher the cost of the capital. That has an impact on the credit quality for the company in the future. So certainly these refinancing risks are rising, and it also points to further credit deterioration across the portfolio.

IFR ASIA: Kenny, have you had to change your funding approach this year in terms of tenors?

Kenny Chan, Zhenro: We are pretty much done with all the refinancing activities for this year. We only have one bond that will mature, in November. The necessary funds are already ready, and to be honest, I think that all the funding activities are dependant on demand and supply.

Right now, we have been managing short-term debt very well. We’re still able to maintain a cash to short-term-debt rate as of today of at least two times. We are expecting to lower our total debt in the next three to six months.

So yes, the market is not functioning well at this moment. There’s true panic. But I’m happy to see Double Bs start to have some kind of recovery. I think that people realise that maybe the market has been too panicked, and some names that are close to IG level have a double-digit return, and with no short-term debt maturing in six to nine months.

When the local liquidity recovers, I hope it will also help the overall secondary bond market. But for Zhenro, we are equipped to go through this turmoil.

IFR ASIA: Talking about the companies that don’t manage to refinance and don’t get through this, what kinds of outcomes have we seen in Asian bond restructurings in the past?

Annalisa Di Chiara, Moody’s: Across our rated base, we had about 15 defaults in 2020. A number of those companies are still going through restructuring, and that includes both companies that have defaulted on paying interest as well as distressed exchanges. What we see over and over again is even after a restructuring, even after a distressed exchange, which may reduce the amount of absolute debt on the company, capital restructures remain a bit untenable.

So there really needs to be a significant infusion of equity or restructuring that actually solves the problem so that, number one, the capital structure becomes tenable. At the same time, the base fundamentals of the company, the business, recovers from the pandemic. You’ve got to have those two things to see some recovery in the bond restructurings.

What we have seen is those companies that have defaulted are still at the Caa range. Some of them have climbed back into B3 or they’re hovering around that range, which still indicates that down the line, there could be another default. So they haven’t solved the problem. They’ve sort of put a Band-Aid on it.

IFR ASIA: Monica, from the investor side, do you think recent bond restructurings are becoming more or less friendly to offshore investors?

Monica Hsiao, Triada: The biggest problem is that it feels fairly unpredictable on a case by case basis. There isn’t a uniform process and it’s not so much based on rule by law, because there are so many factors at stake to see whether a situation is lending itself to a real commercial negotiation in good faith. If you have some liquidity issues but not a solvency issue, in theory, you should be able to find a way to move forward in a win-win outcome for long term recovery.

But many factors rely on the goodwill of the parties involved, and also potential government influences. There’s the China Fortune Land example. The offshore holders have not really received much information or had a seat at the table yet, and are asked to just sit out and wait until they’re ready to disclose a proposal.

We don’t know, but I suspect that Evergrande will be something similar and it remains to be seen whether onshore and offshore holders are handled together or separately.

This is something that we need to see if the government wants to promote more transparency in this restructuring process and find a more efficient way to manage and facilitate fair outcomes as we get more defaults, which seems inevitable at this point.

In my view if there is a commercial interest to negotiate properly, that still lends itself to a functioning distressed market. If you have situations where market participants perceive outcomes as unpredictable and dependent completely on whether a certain party in a committee is aggressive or not and whether or not the issuer has an interest to even engage to resolve, then how can investors analyse recovery scenarios?

Part of what has contributed to this market becoming like this is that in recent years, we’ve had some restructuring advisers, who have come to the market who have been sort of horse whisperers to some of these issuers to arbitrage situations against the interest of creditors. So it has actually affected the incentives of issuers to think about what they can get away with, and that has also added another element of both the distrust and unpredictability to outcomes.

IFR ASIA: How long will the primary market freeze and do you see any signs that things are improving or that we’re turning a corner?

Kenny Chan, Zhenro: Before Fantasia’s case, I think you could see that the local governments, even central governments or even Evergrande were trying to resolve the chaos, and I think they have really been executing. Right before the national holiday, I could feel that some of the local markets or the local banks stopped releasing liquidity. Even some of the banks in Tier 1 cities have stopped lowering the mortgage rate.

At that moment, I thought it was like a type of recovery. Unfortunately, the outcome of Fantasia has frightened everyone in the market. It’s a ‘trust’ issue right now. I think if you look at the fiscal market and the property market in China, if you look at the first nine months, in Tier 1 to Tier 2 cities, on an annual basis, the overall transactions were still up by 5%.

For Tier 3 to Tier 5, it was effective growth, but if you look at September’s performance, overall, it is down by 20% to 30%. I think the overall downturn of the quantitative sales is not caused by the sentiment. It’s basically caused by the mortgage approval period.

There are many willing buyers in the Tier 1 to Tier 3 cities. Unfortunately, they couldn’t get the mortgages on time. In the first week after the national holiday, I could feel that the banks are more willing to support the developers. In the fiscal market, I expect there will be some kind of a recovery in the next two to five months, but for the capital market, I think it may take a slightly longer time because these are trust issues.

For the rest of this year, I think the market will stay remain very volatile, and for peers like us, we totally understand the investors’ concerns, we totally understand where the agencies are concerned. I am happy to see many of my peers are now willing to host investor calls, to talk to rating agencies, and give more comfort to them.

However, companies like Sinic, Modern Land or even Fantasia are relatively small players in the industry. I hope the bigger players could become leaders in the sector and show the investors what we should do so that it could help to recuperate the sector and build the proper image.

But I am optimistic. I think what doesn’t kill you makes you stronger, and I think we could go through this turmoil together effectively and safely.

IFR ASIA: Deepak, is there a potential for high-yield issuers, especially from China, to issue secured bonds or have some kind of structural enhancement to help them get investor support at the moment?

Deepak Dangayach, UBS: In China there are certain regulatory considerations on getting your onshore guarantee. All security onshore needs regulatory approval specifically, so it’s very tough to get a secured bond unless you get regulatory approval. To the extent that they have something offshore, you can, potentially, have security on that, but I think that’s a very small percentage for China, and especially the property developers.

But where I see opportunity is, potentially, to have a lot more transparency in terms of disclosures, especially the off-balance-sheet liabilities that they might have. I think it will be good to have those kinds of disclosures up front because one of the questions that you see a lot from the investors is: “Yes, that’s on the book, but what is ‘off balance sheet’ that they might still be liable for?” And that is sometimes not disclosed in full detail.

I see that part improving further in terms of transparency and disclosures. That might help alleviate some of the concerns here.

IFR ASIA: This is a question that can’t be answered by definition, but how big do you think the problem is of off-balance-sheet funding that’s not disclosed and how do you know whether you can trust a balance sheet?

Monica Hsiao, Triada: I think the base-case assumption of the market right now is that nobody can be trusted. It has become harder to assess if you can trust management individually as they navigate changing conditions.

These days even if a company does not have that much off balance sheet, they get judged with suspicion anyway with all the other bad apples.

As Kenny alluded to, it really is a crisis of confidence. Some companies try to be fairly upfront about disclosing exactly what they have that’s off the balance sheet but the market will continue to have rumours about additional debt whether or not that can be proven.

There are ways that I think you can triangulate to have some of the picture, but ultimately, this process will force a clean-up to some extent because issuers that they have to get in line and do things in a more kosher way in order to survive.

It is inevitable in any financial market that is becoming more sophisticated that issuers will have debt underlying some structured products and wealth management products blow ups are one of the recently reported triggers. In the global financial crisis, everything structured became dirty, but it’s not about the instrument being bad in itself. It’s really just how the participants use it and the choice of transparency.

Unfortunately, there is no bullet-proof way to be able to be sure about off-balance sheet debt. If there were, I think the market wouldn’t be in so jittery and we could return to trusting fundamental valuation.

IFR ASIA: Taking Monica’s comment about a ‘vortex of fear’, how far will this vortex reach? Do you see this panic even affecting investment grade or is it strictly limited to the high-yield issuers?

Deepak Dangayach, UBS: There is a lot of concern out there in the market, so that has impacted high yield in China, and has gradually trickled in via the trading levels for the South-East Asian money.

Investment grade has been impacted, but that’s broader. You see some of the concerns around regulations of the tech industry, etc.

Some of the real-estate names which are in the crossover segment or near to investment grade have widened. I would say that it has had some impact on investment grade, but frankly, not a lot. I do not see this as similar to what we saw during March or April of last year due to this pandemic, where everything was sold off.

Investment grade has widened, but not at the same quantity. Where you’ve seen investment-grade new issues, that’s where the new-issue premiums have widened. That’s the part that the market has penalised.

Monica Hsiao, Triada: It’s spread beyond what I would have told you last week and the week before. It just got to the point where everybody was thinking, “Okay, maybe all the bonds should just keep falling until they get to 40 or 30.”

I think that’s how the dealers were thinking in terms of making prices with a liquidity bid. In reality, I don’t think there’s necessarily been that much volume. When you see a bond fall 20 points, it isn’t as driven by the number of sellers as much as panic seller might have a hit a liquidity bid that is 8 points lower than indicated.

Selling begets selling, just like buying begets buying because there’s such a herd mentality behaviour in Asia as an emerging market. I thought last year we should have grown up beyond that, but apparently not.

Today is the first day we’re starting to see a few green shoots, some semblance of trying to normalise. Some of the higher-quality property papers did have some rebound, but it feels like a lot of it is also short covering. For the true recovery to come back it will take a bit of time.

I expect our markets to remain volatile in the foreseeable future. As soon as some bonds start to recover, if there is one headline, one blogger with something remotely negative, dealers will start to push the other way again.

What the market is searching for is some clue, some line from the government. People want some kind of saving grace that will come from the heavens. I don’t think that we can have a full reversal of recent policies, but we hope for normalisation of the sector as banks start to loosen their balance sheet to fund legitimate projects and loosen mortgage loans.

It’s true that many, many companies did comply and are trying to meet the three red lines, and they’re making progress with deleveraging. However, this compliance will be thrown out of balance and simply by sales going down too quickly. The recent restrictions have affected cash collection ratios as well.

You have a number of announcements now of some lifting of some quota restrictions around mortgages that will help with cash collection, mortgage applications, loosening, things like this.

That so far is happening at a province or city level. Whether or this is coming from a centralised decision to allow them to do that, we don’t know. Another thing market will see is whether before end of the year there’s a reserve requirement ratio cut, which seems needed.

The one disappointing factor for the market right now – and I think this is what did not stop the vortex of fear – was that when we came out of China holidays, people all expected that there would be, potentially, a RRR cut and that, in the very least, PBoC would continue to pump liquidity into the markets.

But that didn’t happen, and instead, they were withdrawing liquidity in the week after, because they had pumped in a lot before holidays. So that threw that market into some confusion.

This fear will take some time to dissipate. A large part of the flows in Asia are driven by retail, and retail is not just your mom and pop. It’s big family offices, big high-net-worth individuals, tycoons, people with a lot of money who could take down US$100m of a deal, potentially – some of those guys that come through private banks.

That flow will probably take a bit of time to return because the LTV, the borrowing for which you could use bonds as collateral, has been cut across the board for all the property sector bonds starting with Single B rated. So the fear has been: “Will that cut start moving towards the BB rated bonds?”

Today, there’s a bit of stabilisation, but if that spiral continues in the bonds, then the banks may consider that and their credit risk committees may further cut available leverage capacity.

We have all come to the point where we’re sort of numb to what the next day brings in terms of markets, and part of it is because dealers also are not providing much trading liquidity in either direction as we go towards the end of the year. It’s all these factors that happen to be creating this perfect storm.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com