Takahiro Okamoto, IFR/DealWatch: Welcome to the Japan DCM ESG roundtable from IFR and DealWatch. During this discussion we will ask the panellists for their opinions on topics such as how markets are preparing for the end of Libor, and what the prospects of domestic credit markets are as interest rates are rising across the globe. After that, a discussion about ESG bond markets will follow and we will ask for panellists’ opinions on issues related to domestic ESG bond markets. Regarding the end of Libor at year-end, the first deal using Tonar priced last month. Please explain the circumstances that led Mitsubishi Corporation to choose to refer to Tonar. Also, did you have any problems with the first deal?

Hajime Horiuchi, Mitsubishi: Many of the subordinated bond deals priced before used one-year JGBs for the reference interest rate after the first call. However, I believe JGBs are being used only provisionally because, when Libor transition was being discussed, we didn’t know what the succeeding benchmark rate would be. The problem when we use JGBs for the reference rate is a mismatch, where the one-year JGB yield is applied to semi-annual interest payments. Especially when interest rates are rising sharply, investors will incur losses. Assuming current market conditions, the possibility of that occurring may be small, but we think it’s best to have an alternative. We started considering issuing a hybrid bond, and we picked Tonar in the end. There are two reasons for that: the large number of overnight unsecured call transactions, which Tonar is based on so we know there is no issue with its robustness or liquidity. The second is that it’s consistent with the fallback rate of derivatives. Each company may have different circumstances, but we move funds raised at fixed interest rates to floating interest rates by using interest rate swaps. As TORF [the Tokyo Term Risk Free Rate] is still not established in the swap market, there is an advantage in using Tonar given the compatibility with the swap market.

With regard to whether we faced any issues, one drawback of using Tonar is that some people we talked to were not ready to use it because Tonar is a compound rate set in arrears [as opposed to the traditional rate set in advance]. But our company has completed the operational transition, including the system transition, so we didn’t have a problem. We used to use Libor for indirect finance and derivatives, but we have completed almost everything required for transition, and we are using Tonar as the alternative benchmark rate.

The remaining talking point was whether investors would accept it. We collaborated with lead managers, including Mitsubishi UFJ Morgan Stanley, Nomura and Daiwa, who are present today, and they conducted extensive research about whether investors would accept Tonar. After verifying this research, we used Tonar. During the process, investors asked why we picked Tonar, how we calculated accrued interests when selling in the secondary market, and whether we used any auxiliary function to calculate accrued interests. After clear communication with them, they understood, and we had 230 investors participating in the deal. There weren’t many investors who didn’t participate because of Tonar.

Takahiro Okamoto, IFR/DealWatch: Did you have any concerns about Tonar’s liquidity or price validity?

Hajime Horiuchi, Mitsubishi: No. As I mentioned earlier, the underlying asset for Tonar is the overnight unsecured call rate, so there is no issue with its liquidity. In terms of the pricing procedure, we adopted the spread pricing method using Tonar swaps to set the coupon for the first five years of the non-call period of the subordinated hybrid bonds. We believe it is important to use spread pricing because this can reflect the creditworthiness of an issuer. We had been using Libor swaps and have now switched to Tonar swaps.

Furthermore, the market has been transitioning quickly from Libor swaps to Tonar swaps since July. According to data from Japan Securities Clearing Corporation, Tonar swaps now account for 60%-70% of the market as of September, whereas Libor swaps have fallen to around 20%. We believe Tonar swaps will most likely be the mainstream option when mid-swap spread pricing gains popularity.

Takahiro Okamoto, IFR/DealWatch: Since Mitsubishi’s deal, we have seen BFCM use Tonar as a reference, but I get the impression that Tonar-based deals are not increasing overall. Why do you think that is?

Haruhiro Ikezaki, Mitsubishi UFJ Morgan Stanley Securities: At the moment, JGBs are widely used as a reference, but there is a mismatch [between the one-year of the maturity of JGBs used and semi-annal coupon payment], as Mr Horiuchi said. Solving this was a key discussion point in the market. Mitsubishi priced the first deal using Tonar in early September, only a short time ago. The difficulty we experienced during the first deal has been extremely useful. We had to overcome the operational hurdle and we, as joint lead managers, and Mitsubishi handled this deal conscientiously and carefully. Investors went from knowing nothing to learning about the instrument, including conventions and calculation methods. In the end, many investors worked on this and familiarised themselves with it. As investors are now prepared, I believe Tonar-based deals will increase beyond BFCM.

As also pointed by Horiuchi san, Tonar compounding in arrears is quickly becoming common in the derivatives space, but the domestic market has been leaning too much towards fixed interest rates, which we think is another reason for Tonar-based deals not increasing. In the low interest rate environment, floating interest rate issues have been rare, but if floaters increase in the future to avoid interest rate risk, we expect more Tonar-based deals.

Takahiro Okamoto, IFR/DealWatch: In the Samurai market, BFCM is the only issuer so far. Do you think more issuers will follow?

Haruhiro Ikezaki, Mitsubishi UFJ Morgan Stanley Securities: We are still in a transitional period, but there is a high possibility that deals will increase because we have seen existing floating-rate bonds use the Tonar compounded rate set in arrears.

Takahiro Okamoto, IFR/DealWatch: Thank you. Next, I’d like to direct a question to Kaori Nishizawa of Fitch. You often talk to banks and financial institutions. Are they ready for alternative benchmark rates? If not, why not?

Kaori Nishizawa, Fitch: Large financial institutions are making progress in line with “The roadmap to prepare for the discontinuation of yen Libor”, which was published at the end of March by the Cross-Industry Committee on Japanese Yen Interest Rate Benchmarks comprising experts in various fields. There are two things to prepare for Libor alternatives. The first is internal preparation, and the second is to deal with contracts with customers. For internal preparation, such as changes in accounting, IT systems, risk management and operational flows, each company is on track or even ahead of schedule, aiming to complete by the end of December.

For the amendments to the contracts with customers, the degree of preparation varies. Unlike internal processes, a counterparty is involved. Amendments to syndicate loan contracts take a surprisingly long time compared with bilateral contracts as there are more people involved, but progress is faster in some syndicate loan contracts as arrangers take a leading role and manage coordination.

We heard concerns from abroad that the transition period is too short, because the plan was published when there were only nine months left. However, preparations had already started in Japan. Like vaccinations, once Japan sets about doing something, it will focus on the goal with a sense of urgency. Financial institutions were already aware of the issues with transition, and they have been preparing steadily for transition.

Takahiro Okamoto, IFR/DealWatch: Is there any impact on credit rating equity treatment if a hybrid instrument facilitates the transition to risk-free rates? Does Tonar referencing have any impact?

Kaori Nishizawa, Fitch: In Fitch’s rating criteria for equity credit, we don’t expect any impact on equity credit assessment from the change in benchmark rate. It is our understanding that a change in spread due to the interest rate transition would not be considered a step-up, a call, or refinancing, which would make a difference in our equity credit assessment. However, credit ratings could be affected if a failed transition leads to credit risk, whether as a result of litigation, reputational and conduct risk, operational or any other risks.

Takahiro Okamoto, IFR/DealWatch: Mr Horiuchi, how are you preparing for the end of Libor for bonds that currently use Libor as a reference?

Hajime Horiuchi, Mitsubishi: You’re talking about the reference interest rate after the non-call period of subordinated bonds that our company has already issued, and we must consider this from the perspective of issuers and investors. First, for issuers, what concerns them most is equity evaluation. As pointed out by Ms Nishizawa, that alone does not fundamentally affect equity evaluation. In February, the Financial Services Agency published its view that whether or not banks’ subordinated bonds contain fallback language does not affect banks’ equity capital. Moreover, ratings agencies have said that even if a meeting of bondholders does not take place to add fallback language, it will not affect their equity evaluation, so ratings agencies’ views are not a concern. For investors, there is no incentive to hold a bondholder meeting to add fallback language because, if we held such a meeting, trading [of the bond] would be suspended for at least a week, and that’s not something they want. We don’t need to do anything with our existing subordinated bonds that use Libor for the reference rate after the non-call period, and I think this is becoming standard.

Takahiro Okamoto, IFR/DealWatch: Mr Ikezaki, what do you think of the transparency bookbuilding method introduced this year in the domestic bond market? I understand there have been no big problems but I’ve heard that’s because the market environment is good. How will the transparency method function if the market environment worsens? There are also deals coming out that use the pot method. Will we see that more widely used in domestic bond markets?

Haruhiro Ikezaki, Mitsubishi UFJ Morgan Stanley Securities: This is a really big topic. Mitsubishi introduced the pot system in Japan when it publicly offered a hybrid bond in 2015, and now almost all hybrid bonds use the system. Even senior bonds use the pot, such as last year’s ¥1trn deal from NTT Finance, which is our country’s largest corporate bond deal. The advantage is efficiency, especially in a large bond deal, and speed, including information sharing, so the pot is well liked. The transparency method was introduced in January and started to be implemented in all deals in July, so it’s still too early to say which is preferred. I expect the pot and the transparency method will each be used depending on the situation. For example, when we do a large deal or need to do quick marketing, I think the pot will be used. Currently, the pot is used for 20% of deals on an issuance-volume basis. When the two methods are used evenly, people will be able to decide which one is better. The transparency method when market conditions are good is extremely effective, and the pot functions well when market conditions worsen because it organises everything in one book. We expect in the medium to long term the market will shift in favour of the pot.

Takahiro Okamoto, IFR/DealWatch: Mr Horiuchi, what do you think of the transparency method and pot system?

Hajime Horiuchi, Mitsubishi: Compared to the traditional retention method, not only has transparency improved dramatically but it also contributes to solving the so-called “unsold bond” problem. Our company has used the pot method when we sell foreign bonds and subordinated bonds, and we believe the pot has an advantage in terms of the transparency in pricing and understanding investor trends, which we use for our investor relations strategy. One concern is that, when market conditions worsen, lead managers can purchase bonds for their own proprietary trading books as long as they report it [and hence the unsold bond problem would be left unsolved]. I hear there have been no deals with orders from lead managers’ proprietary trading books because the market environment is favourable. As pointed out by Mr Ikezaki earlier, the pot method is preferable when the market environment worsens. When you assess the transparency method, you need to consider how lead managers’ proprietary trading books are used.

Takahiro Okamoto, IFR/DealWatch: The next question is about the prospects of the domestic credit market. Mr Ikezaki, yields have been rising globally because of expectations that Fed tapering will start next month [November]. What’s your opinion?

Haruhiro Ikezaki, Mitsubishi UFJ Morgan Stanley Securities: This is also an important issue. While Fed tapering is expected next month, there are various factors coming together in our country from the second half of this year to next year, such as the election for the House of Representatives this month. Also, the end of the term of Bank of Japan governor Haruhiko Kuroda is in 2023. Looking at the post-pandemic future, we see risks of higher yields in the domestic bond market. However, we don’t expect a rapid rise in yields because the economy needs to pick up pace for that, even though it is extremely important for us domestic bond market participants to accommodate the risks of higher yields. As mentioned by Mr Horiuchi, the absolute yield pricing method has become mainstream in the domestic market because of the BoJ’s negative interest rate policy since 2016, but we expect we will return to the spread pricing method at some point. It is important to prepare for that in the second half of 2021 and next year, where we add a spread while watching the moves in risk-free rates, and that’s critical to create a smooth and stable primary market.

Takahiro Okamoto, IFR/DealWatch: In that case, are spread pricing cases appearing? When they appear it probably means that the market is preparing for interest rate increases. While we’re on this subject, Mr Horiuchi, could you please share with us the kinds of fundraising strategies you are considering?

Hajime Horiuchi, Mitsubishi: The risk of higher interest rates is an important topic. However, as I mentioned, our company moves funds we obtain by exchanging a fixed-coupon corporate bond to floating rates using swaps so we are not overly concerned about it. The reason we swap to floating interest rates is because our natural resources assets in our portfolio are affected by economic fluctuations and price movements. When the economy is doing well, our income from natural resources will increase, and central banks will tighten monetary policy and raise rates to fight inflation. This means that, while income will increase on the assets side, expenses will also increase, and it will act as a natural hedge. If the inverse occurs, our income from natural resources will decrease when the economy is doing badly, but there will be monetary easing and lowering of interest rates, so this will lower expenses. This natural hedge suits a portfolio like ours, so we use floating rates for liabilities. We won’t rush to raise funds just because long-term interest rates are expected to rise; instead we will carefully procure funds while observing the balance between direct and indirect financing.

Takahiro Okamoto, IFR/DealWatch: Let’s begin the second part of the panel discussion looking at how the domestic ESG bond market has expanded.

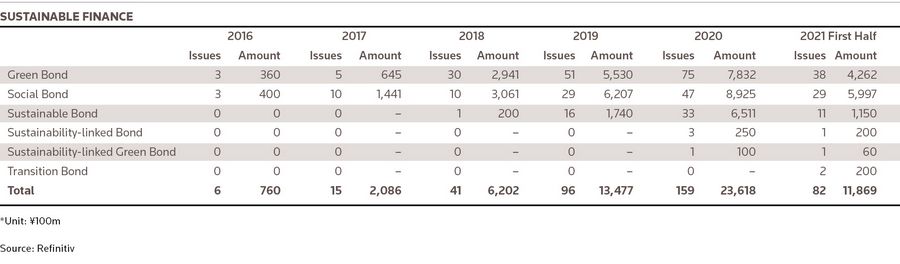

According to data from DealWatch, volume was ¥76bn in 2016, ¥208.6bn the following year, ¥620.2bn in 2018, ¥1.3477trn in 2019, and ¥2.3618TRN last year. Then in the first half of this year, the growth has continued steadily to ¥1.1869trn. Since Tokyo Metropolitan Government has contributed to the expansion of the green bond market, I’ll ask Mr Suzuki first. I understand there are limits to the use of proceeds of Tokyo’s ESG bonds. How do you decide the UoP, and have you experienced any challenges when you sell ESG bonds?

Kosuke Suzuki, Tokyo Metropolitan Government: To decide the use of proceeds, my bond issuance team looks at the budget requests from each bureau in Tokyo Metropolitan, examines whether projects meet ICMA’s Green Bond Principles and whether we can publicly explain their environmental impact, and then the team picks appropriate projects. We work with related parties, seeking permission from each bureau to see whether we can use the proceeds on their projects and obtaining certification from external evaluation agencies. We decide on the UoP after this process.

One hard part of the decision process is finding a reasonable amount of eligible projects for bond issuance. The selection of projects that can be used is quite narrow because, for local government bodies, there are regulations on the kinds of projects we can fund with the proceeds from municipal bonds. Other difficulties are explaining to external reviewers about the eligible projects’ environmental impact and receiving understanding and cooperation from the bureaus responsible for the projects. When we started ESG bond issuance in 2017, there were inquiries from various bureaus, such as how green bonds are different from ordinary bonds, and what are the advantages of issuing green bonds. My predecessors told me that it was hard at first to explain a lot of concepts but now we have been doing green bonds for five years. We have gradually created an environment where it is easy for other bureaus within Tokyo Metropolitan to understand.

Takahiro Okamoto, IFR/DealWatch: Can you tell us why you have increased this fiscal year’s green bond issuance by ¥10bn from the previous fiscal year?

Kosuke Suzuki, Tokyo Metropolitan Government: We have seen many investors participate in our green bonds for the past four issues. We wanted to respond to the high demand so we increased the amount when we priced our fifth green bond on October 15. Additionally, this year, we have seen a decline in tax revenues because of the coronavirus, so we decided to use metropolitan bonds, including green bonds, to compensate for that.

Takahiro Okamoto, IFR/DealWatch: Is there any message you’d like to share with other local governments?

Kosuke Suzuki, Tokyo Metropolitan Government: Many local governments experience difficulties in finding eligible projects, as we do. We have issued green bonds five times, including this year, so they can see what projects can be considered from our experience. Issuing ESG bonds, such as green bonds and social bonds, requires additional cost and effort but helps expand our investor base. We’d like to share know-how and information with other municipal governments as much as possible and energise the ESG market.

Takahiro Okamoto, IFR/DealWatch: I’d like to ask some questions to Daiwa’s Shimizu san. Do you think Tokyo Metropolitan Government’s ESG bonds will encourage other regional governments? Also, could you please share your views on recent developments in the ESG bond market?

Kazushi Shimizu, Daiwa: Let me talk about the characteristics of their green and social bonds. If you look at Tokyo’s green bonds that priced in October, Tokyo allocated the proceeds mostly for maintenance of small and medium rivers, which falls under climate change adaptation to protect against water disasters like typhoons. Because such disasters have been increasing, it is an urgent issue in Japan. We can protect human lives by quickly conducting levee work and can categorise this as a climate change adaptation project, which has both a social aspect of building social infrastructure and a green aspect. This has an immediate effect as you can quickly allocate proceeds to projects, in contrast with climate change mitigation which involves reducing CO2 emissions in the long term. Last fiscal year Nagano prefecture and Kanagawa prefecture and this year Kawasaki city and Kita-Kyushu city chose climate change adaptation projects for their first ESG deals.

With regard to social bonds, we pay close attention to special education school projects and challenge school projects that Tokyo allocated the proceeds to. These are categorised as education under the Social Bond Principles and lead to diversity. About 90% of the children with disabilities at special education schools go on to college or find a job, so these projects lead to diversity in our society.

I expect other local government bodies will choose climate change adaptation projects for their green bonds. We see water disasters every summer until early autumn, so I think municipal green bonds will definitely increase. I also think there will be more social bonds with the proceeds to be used to support children with disabilities, such as special support schools. It will lead to an increase in sustainable bond issues that include green and social projects.

Takahiro Okamoto, IFR/DealWatch: I think climate change adaptation is a good fit for the Japanese market. Let’s move on to NTT, which is preparing green bonds worth ¥300bn and is marketing the bonds at the moment. Momose san, could you tell us what brought you to this issuance?

Shinya Momose, NTT: NTT Group published its new environment and energy vision on September 28. There are two reasons behind this publication, the first being that NTT Group uses 1% of all of Japan’s electricity, and the second being that we provide decarbonisation solutions to customers through ICT services. One of our company’s missions is to contribute to climate change mitigation so we published this ambitious vision. After that, on September 30, we held our annual IR Day, where we picked topics not just on the environment and energy but also on the “S” and the “G” in ESG, which involves adopting a new management style, and explained these topics to investors. In order to promote these initiatives, we believe it is extremely important to reinforce the finance aspect of it and support environmental investing. With regard to the timing, we wanted to issue large green bonds at a global scale right after we published this vision because we wanted to attract the market’s attention.

Takahiro Okamoto, IFR/DealWatch: Thank you, Mr Momose. Could you talk a bit more about your new environment and energy vision?

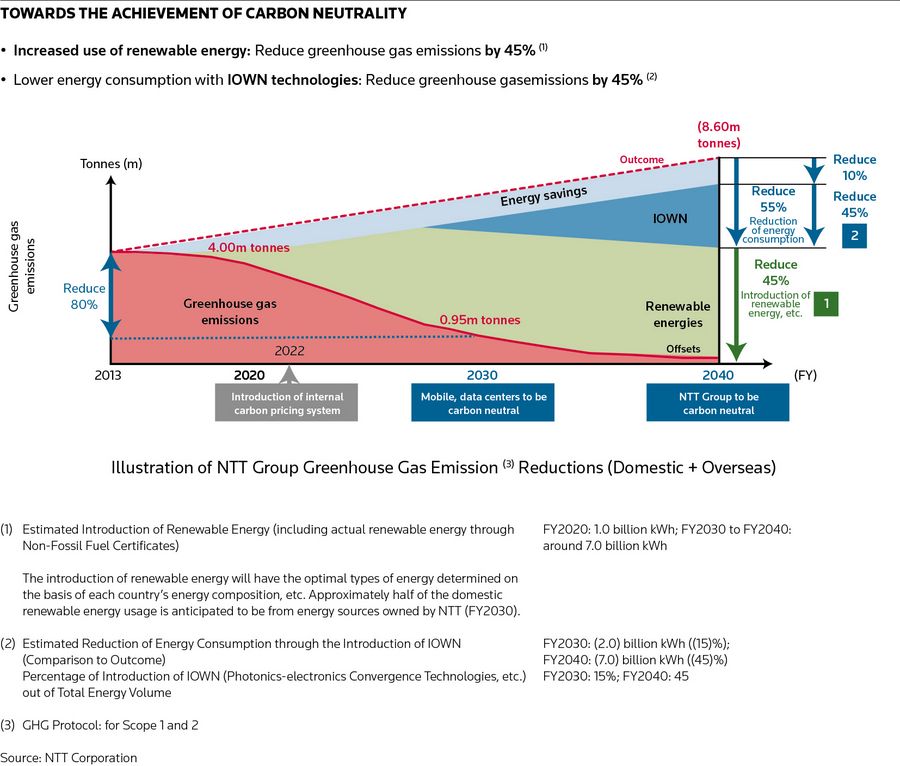

Shinya Momose, NTT: NTT Group’s target for fiscal 2030 is to reduce greenhouse gases emissions by 80% compared with 2013. As our mobile telephony and data centres use the most electricity, our target for 2030 is to be carbon neutral in these two segments. NTT Group as a whole wants to be carbon neutral by 2040.

If we don’t do anything, the outcome will be higher electricity use. To become carbon neutral, we are working on three fronts. The first is a continuous effort to conserve energy, aiming to reduce electricity use by 10%.

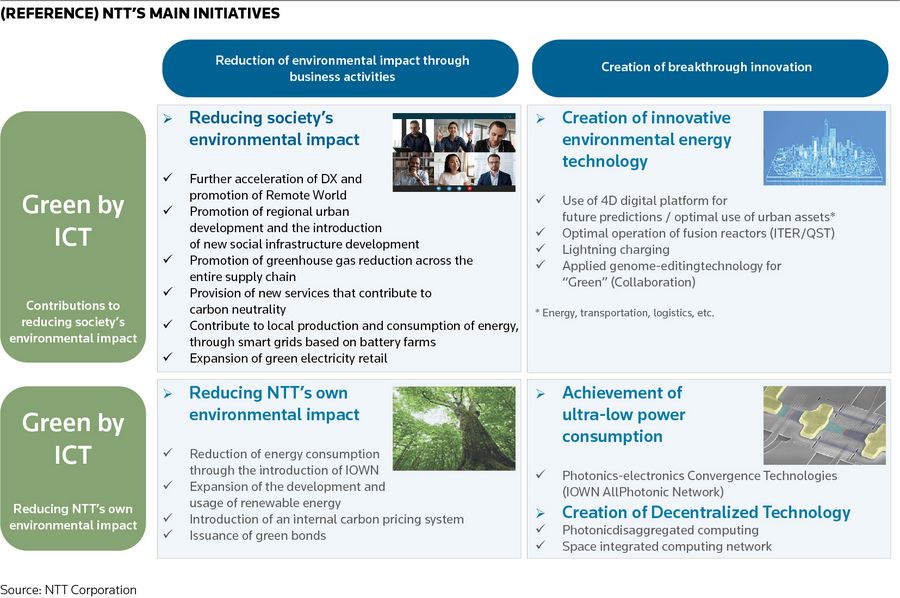

The second is the introduction of “IOWN” (Innovative Optical and Wireless Network) to reduce electricity use by 45%. This is the next generation network structure that aims to increase electricity efficiency by 100 times. For the remaining 45%, we will use renewable energy, and half of that from our own energy generation.

IOWN and renewable energy are extremely important elements and we have included them as eligible projects for green bonds.

The Green by ICT concept involves people moving less and using 5G and fibre-to-the-home connectivity, and we have added these as eligible projects for future green bonds. In this way, the eligible projects for the green bonds we are issuing this time were not selected from one specific part of our businesses, but instead from the most important elements for our environment and energy vision, and this is the key characteristic of this issuance.

Takahiro Okamoto, IFR/DealWatch: How did investors respond as you prepared to issue green bonds?

Shinya Momose, NTT: We issued a green bond last summer and there were a number of questions at the investor event about our corporate bonds. But at the IR event we did last week for the new bond, there were many – and quite deep – questions about our environmental and energy vision, and we saw investors’ strong interest in the environment. In this latest IR event, we were able to exchange a wide variety of opinions about ESG as a whole, not just about green bonds but also social and governance factors. Throughout the event, we detected strong demand for green bonds. Above all was the importance of direct communication with investors, and we will continue to communicate with investors and link this to green bond issuance.

Takahiro Okamoto, IFR/DealWatch: Mr Kawamura of Nomura Securities, I have three questions for you. My first is what role your company played leading up to NTT issuing green bonds. The second is how you bring in issuers to the ESG market who have found it difficult to do so or who have never issued ESG bonds before. Finally, please share your thoughts on the development of the ESG market.

Hitoshi Kawamura, Nomura: On NTT’s green bond issuance our role is structuring agent. We helped formulate the overall scheme for the green bond issuance. We were also documentation manager and bookrunner. We started helping NTT on their first green bond issuance last June with things like selecting an evaluation company and formulating the framework. We had them hire Sustainalytics, which is highly respected by investors and has a global presence. The main point was to update their framework to cover their large [corporate] investments, as mentioned by Mr Momose. We discussed the issue in depth with Sustainalytics so they could endorse its alignment, including the important elements of NTT’s environment and energy vision and the new use of proceeds. As a result, we were able to include a new use of funds for 5G and future fibre-optic communication technologies, and we have obtained a more up-to-date framework that can be used for future issues.

There are three main points I’d like to share about how to get issuers to participate in the market if they have never issued ESG bonds before. The first is whether you can obtain a reliable second-party opinion from an external evaluation company, and this is the starting point. Nomura can answer any doubts or concerns issuers may have by leveraging our know-how through the experience of completing deals domestically and internationally and leveraging our relationships with evaluation companies. We are conscious about providing detailed support.

The second point is to create a scheme for issuing ESG bonds, but I believe it is important to make this scheme appealing to all your stakeholders. There are a large number of issuers that want to improve their ESG scores and it is important to make sure investors understand your ESG story. Especially in the transition bond market lately, investors are evaluating issuers’ strategies and reliability of execution, so we put efforts into creating a story while being transparent.

The third point is that we put efforts in offering high-quality advice by staying well-versed with global ESG trends. We hear about ESG trends globally, and we closely watch advancements in Europe in particular. Last week, our company was lead manager for the European Union’s first green bond, and I believe we can really help Japanese issuers, such as understanding how the EU Green Bond Standard will be created.

Regarding the expansion of the Japanese ESG market, as I briefly touched on this earlier, I believe it is becoming necessary even for existing issuers to update their frameworks and do maintenance checks so that they can issue continuously and make their ESG stories more appealing.

Takahiro Okamoto, IFR/DealWatch: Next, I’d like to hear from Dai-Ichi Life about their ESG investments. Ms Zeniya, could you please tell us a bit about the responsible investment report that was published recently?

Miyuki Zeniya, Dai-Ichi Life: Dai-ichi Life manages about ¥38trn of assets, and I promote and oversee ESG integration for all those assets. Since we signed the PRI [Principles for Responsible Investment] in 2015, we have published a responsible investment report every year on our activity, including stewardship. This is not just to receive PRI evaluation but also to make our activities known to our insurance contract customers as well as to the public, which we think is part of our role as an asset owner in the investment chain, with the aim to show how our activities contribute to society in general. We also publish this annual report to explain our investment policy to new companies we invest in or already have stakes in.

Takahiro Okamoto, IFR/DealWatch: When your company conducts an ESG investigation, are there any points you have trouble with?

Miyuki Zeniya, Dai-Ichi Life: It’s not just us, but the level of disclosure by Japanese companies seems insufficient compared to other countries. This is despite the fact that a TCFD [Task Force on Climate-related Financial Disclosures] consortium has been established in Japan, and that the number of businesses that support the TCFD is the highest on the planet. Disclosure is insufficient, not only on climate change, or the “E”, but also on the social part. Regarding that, a National Action Plan was published last year. This is about business and human rights. Interest in this topic has been extremely high abroad for many years now, but there is less understanding among Japanese companies. As a result, there is little information disclosed on this.

ESG themes keep expanding, including topics like biodiversity. Companies publish various reports annually such as integrated reports, environmental reports, and data books, and some advanced companies disclose information in great detail, but not every company does. Businesses write up reports and disclose non-financial information, but many just disclose policies and initiatives, but little numerical data on how these are linked to their business strategies. This can be the biggest obstacle for us when we factor their strategies into our business evaluation.

Takahiro Okamoto, IFR/DealWatch: When I looked on Dai-Ichi Life’s website, I saw that you examine and analyse specific “ESG issues” in the beginning of the investment decision process. Can you explain what they are?

Miyuki Zeniya, Dai-Ichi Life: Japan’s Stewardship Code was introduced in 2014 and the Corporate Governance Code was introduced the following year, and we started working on ESG issues from a governance perspective. Then we started working on climate change from an environmental aspect and then on business and human rights from a social aspect. Since we are a life insurance company, our perspective is also important, so we take that into account when we choose ESG themes. However, there are many considerations about industry type, company size, whether business operations are global or domestic, etc. We believe it is ineffective to talk about the same topics [with each investee company]. When we talk to them or meet them, we think about those large themes, but we prioritise each business’s issues. If a company is already putting in effort on issues that we think are higher priorities, that’s great. But if their efforts are not enough, we focus on themes we think they should prioritise when we talk with them.

Takahiro Okamoto, IFR/DealWatch: When you evaluate investee companies or talk with issuers, how do you check their position and efforts, and how do you organise and evaluate them?

Miyuki Zeniya, Dai-Ichi Life: Actually, more businesses are now publishing non-financial disclosures. They also publish not just integrated reports but also securities reports and governance reports. And more companies hold ESG explanatory meetings, in addition to their ordinary IR meetings. We participate in those meetings and look at public data. We also use ESG vendor information. What we look at most when we talk with companies is how much they actually do compared to what they say in their disclosures.

What we often find when we talk with them is, while their disclosures are written very elegantly, their initiatives are not actually progressing, so we pay close attention to that. Also, when we talk with them, they have managers from various departments join, but sometimes we find out that they work in silos. We also check if what they said last year is proceeding this year. Since we are a long-term investor, we don’t ask how things are going every quarter, but whether they are seriously making efforts is very significant for us.

Takahiro Okamoto, IFR/DealWatch: Fitch has been considering ESG factors in the ratings decision process for some time and has introduced something called ESG Relevance Scores. Could you please tell us more? To what degree do ESG factors affect rating decisions when you analyse financial institutions? And could you tell us what kinds of industries are affected by ESG factors?

Kaori Nishizawa, Fitch: Fitch introduced ESG Relevance Scores in 2019 but even before that, our company was factoring ESG elements into our rating decisions. ESG Relevance Scores were introduced just to visualise and clarify the extent to which each ESG element affects our credit rating decision. It is not about whether a company’s ESG strategy is good or not, but instead it is a score that measures how much it affects our rating decision. We apply four or five general issues from each of environment, social and governance to 100 sector-specific templates, based on the main risk factors of classification standards widely accepted and published by entities such as the Sustainability Accounting Standards Board, the Global Reporting Initiative, and UN’s PRI.

When we assign a rating to a company, we use a template for the sector that the company fits in, and we score the extent to which each general issue affects the rating, on a scale of one to five. A score of one means no impact and five means that this issue alone directly impacts the rating. These ESG Relevance Scores are disclosed in Fitch’s issuer reports.

On your question about how relevant this is to Japanese banks and other financial institutions, what has the most impact for Japanese financial institutions is governance. Even then, there are many cases where that score is three. However, some financial institutions that have a wide variety of businesses in complex group structures receive a four. In developing countries, we see many cases where the impact of governance becomes even larger.

In more than 10,500 issuers or deals that Fitch has rated, there are a high number of issuers where the impact of governance is large. When it comes to which companies’ ratings are most affected by environmental issues, corporates, especially automobile manufacturers, oil refiners and sellers, and public works, are high on the list.

Takahiro Okamoto, IFR/DealWatch: You recently established a new team called “Sustainable Fitch”. Could you please tell us what this team does?

Kaori Nishizawa, Fitch: We announced on September 15 that we established Sustainable Fitch, which assigns ESG ratings. This differs from the ESG Relevance Scores in that Sustainable Fitch assigns scores for ESG levels and was created to objectively assess ESG performance and characteristics of issuers and bonds. Of course, it will do other things as well. These scores are backed by clear ESG rating methodologies. As I previously mentioned, this is different from a credit rating. These ESG ratings comprise three major pillars: ESG entity ratings, bond ratings, and framework ratings, and each of these has a rating from one to five. Sustainable Fitch will publish integrated credit research and analysis for ESG using the ESG Relevance Scores. It will also provide various services, such as climate risk assessment based on climate vulnerability scores, new ESG analysis and reports based on the aforementioned ESG ratings, and ongoing sector and thematic ESG research. Regarding the ESG entity and bond ratings, we are preparing to start publishing them early next year.

Takahiro Okamoto, IFR/DealWatch: Thank you. I’d like to ask some questions to Mr Suzuki of Tokyo Metropolitan and Mr Momose of NTT. I believe there are various expenses and time-consuming efforts involved in ESG issues. How do you view such costs, and what is your view on the benefits of integrating ESG? Let’s start with Mr Suzuki from Tokyo Metropolitan.

Kosuke Suzuki, Tokyo Metropolitan: Yes, there are costs associated with ESG bond issuance, such as time working on the issuance and fees. However, the reason we issue green bonds is not just to raise funds for our environmental policy, but also to strengthen the ESG market and accelerate ESG investments by expanding the range of issuers and their investors. We believe these costs are necessary to achieve our goals and policy. In fact, since Tokyo Metropolitan became the first local government to issue green bonds, the number of local governments issuing green bonds has been steadily increasing and we feel that we have contributed to the expansion of the market. I am not saying this is solely down to us, but the expansion is a result of us paying these costs to issue green bonds. Moreover, a wider variety of investors participate in our green and social bonds than in our ordinary metropolitan bonds, and that helps us issue bonds and have stable funding, which is a great benefit. And there is public support [for ESG bond issuance]. Subsidies are available from the Ministry of the Environment, and even from Tokyo Metropolitan. We have subsidies in addition to the ones provided by the MoE, so I believe the burden on issuers can be alleviated to some extent.

Takahiro Okamoto, IFR/DealWatch: Mr Momose of NTT, what do you think of the costs and benefits of ESG?

Shinya Momose, NTT: As Tokyo Metropolitan mentioned, there is a wider range of investors for ESG bonds, so that’s a benefit. It’s an extremely significant opportunity to appeal to the market and get to know our approach to ESG. We did IR this time so we know that investors are extremely interested in green bonds and that there is high demand, and that can affect pricing. There are costs incurred for external reviewers, but it’s not large. Generally, as mentioned by Mr Suzuki, there is also the extra work of collaborating internally with other departments, and also the extra work reporting. However, the climate issue is becoming extremely important for the company so collaboration with other departments is now easier, or perhaps I should say we are now receiving extremely forward-looking, active support from them.

In terms of ESG reporting, the importance of disclosure was brought up by Ms Zeniya of Dai-ichi Life. We have increased ESG disclosures and integrated reports, and would like to disclose more. It is not reporting just to issue green bonds anymore. Today’s issuers must disclose such information anyway so we don’t have to go and get information from other departments. Perhaps this varies depending on issuers, but we don’t particularly feel like this is a large cost. Overall, the benefits outweigh the costs.

Takahiro Okamoto, IFR/DealWatch: I see. I was actually wondering whether the costs would hold issuers back, but it seems that’s not true, and the benefits are larger. I said at the beginning of the discussion that the ESG market is expanding. It looks as if everything is moving in a positive direction, but are there any problems? Or is there anything that could become an issue in the future? First, let’s hear from Ms Nishizawa of Fitch.

Kaori Nishizawa, Fitch: With growing interest in ESG, issues for credit rating analysts include how we evaluate the impact of each company’s approach to ESG on its ratings, how firmly we grasp that, and then how we reflect that in our ratings. We also have issues such as how we provide the ESG-related information that investors, issuers, and everyone in the capital markets need, and how we provide objectively comparable, highly transparent, and visible information in a timely manner. It would be great for us if we can hear everyone’s opinions and requests.

Takahiro Okamoto, IFR/DealWatch: Indeed, there are a lot of investors looking for information, and how you provide that information seems like a significant topic. Ms Zeniya, what do you think about the issues of the ESG market, and how do you think they can be solved, or what do you expect?

Miyuki Zeniya, Dai-Ichi Life: From an investor’s point of view, as all the participants today are already aware, I think the biggest issue is greenwashing or SDG-washing. According to a recent report, more than 70% of ESG funds do not comply with the Paris Agreement. There are also reports coming out that half the funds specialising in climate change do not comply. And two months ago there was one about a banking group where its internal ESG evaluation included some greenwashing. These are big issues. The reason is, for long-term investors like us, it is problematic if what we were told were green bonds when we purchased are actually not green, and if the bonds are actually closer to brown. For banks in Europe, this is included in their assessments. For asset owners like us, whether our assets are truly green is closely linked to whether our assets are resilient, so this is an important issue. This is not something we can handle alone; large issuers like the ones here today, securities houses, and everyone involved in investment chains need to collaborate to resolve this issue.

Takahiro Okamoto, IFR/DealWatch: Indeed, it’s a problem if green assets turn brown mid-way. Mr Shimizu of Daiwa Securities, what do you think?

Kazuhi Shimizu, Daiwa: There are two main issues that we need to acknowledge and manage. One is engagement. When you issue an ESG bond like a green bond, you engage with investors and get an external reviewer to publish a report, like NTT and Tokyo Metropolitan do. Investors then make sure they are very clear about everything before they actually buy it. If the bond is a five-year, 10-year or even longer, investors will have to judge whether the bond actually improves the environment or is beneficial to society, based on public information. It is important that issuers and investors have an opportunity to talk with each other, like this webinar. But even such dialogue may not make all things clear. Securities houses and external reviewers will step in to provide support. External reviewers can check the bond’s environmental impact by publishing a review once a year after issuance. Creating such a framework is extremely important to prevent greenwashing. Very recently, the Financial Services Agency and the Tokyo Stock Exchange set up a working group to develop a sustainable finance platform, and I believe engagement will be even more important.

The other issue is support from public bodies. For NTT and Tokyo Metropolitan, costs were not a factor when they issued ESG bonds. But there are concerns among some Japanese issuers about the costs, such as preparation and fees. When it comes to fees, the Ministry of the Environment has provided green issuance support in the form of subsidies since 2018. In addition, Tokyo Metropolitan in June proposed the Tokyo Green Finance Initiative, and its policy directions include development of the green finance market. As a first step, Tokyo provides subsidies covering 20% of the total expenses for issuers with an office in Tokyo that have already received subsidies from the MoE.

In relation to the EU Green Bond Standards, Japan has also clarified its standards. In 2017, the MoE published its Green Bond Guidelines. This year, the FSA published Social Bond Guidelines, which, referring to the SDGs Action Plan 2021 announced by the government, established a solid framework to tackle social issues specific to Japan.

Support is needed for private corporates so that they can invest confidently in sustainable projects, such as renewable energy and electric vehicles to become carbon neutral by 2050, as announced by former prime minister [Yoshihide] Suga. I think it’ll be important for public bodies to provide support to establish frameworks for sustainable financing.

Takahiro Okamoto, IFR/DealWatch: Thank you. Mr Kawamura, what do you think?

Hitoshi Kawamura, Nomura: When viewed on a global scale, ESG bonds in Japan are still too small, in terms of the number of deals and volume. We are still at an early stage. I hear the world’s ESG investment funds are estimated at ¥3,000trn. Japan, on the other hand, has advanced technological capabilities that can contribute to becoming a decarbonised society. Japan also has, even when viewed on a global scale, a relatively big bond primary market. We also have high-quality investors, including retail investors, so it is extremely important for Japan to get involved in ESG.

When it comes to ESG evaluation, there has been a move towards formulating a taxonomy like in the EU, and this involves unification of standards and centralised set of rules. If such a taxonomy is created, it will make it easier for us to judge whether this bond or that bond can be ESG or whether a bond is green or not, but that means more costs and maintenance to decide whether such standards are truly objective, whether they are based on scientific grounds, and whether they are up to date with technological advancements. For Japan and Japanese issuers not to be isolated from the global trend, Japan should exert its influence during the creation of global rules, and everyone, including the participants here today, should get involved in the creation of global standards so that they will be balanced and include Japan’s point of view.

Takahiro Okamoto, IFR/DealWatch: So if Japan does not participate in the creation of such standards, they might end up being not really applicable in Japan, and Japanese issuers might end up at a disadvantage. Mr Ikezaki of MUMSS, what do you think?

Haruhiro Ikezaki, MITSUBISHI UFJ MORGAN STANLEY SECURITIES: I agree with the other panellists. The Japanese and global ESG bond markets started with green and social bonds, but issuers now have more choice, such as transition bonds and sustainability-linked bonds. Issuers will be expected to explain their sustainability strategies – not just put a limit on the use of proceeds. They will need to explain what strategies they employ to pursue ESG as a company, and that will become more important. As mentioned by Mr Momose about reporting, even a company that doesn’t issue ESG bonds will need to be in touch with [ESG] reporting. 2030 and 2050 are key dates, but many companies’ medium-term management plans, including ours, deal with timeframes that span just three years. Companies will need to present their visions for next 10, 20, 30 and 50 years for investors who hold bonds for a long period of time like Dai-ichi Life, and this will be extremely important for the ESG market to expand.

Takahiro Okamoto, IFR/DealWatch: Thank you. Our time is up, so thank you to our viewers, thank you for participating, and thank you to the panellists for sharing their opinions.

To see the digital version of this report, please click here

To see the Webcast of the event, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com