Trading volumes in interest-rate swaps linked to the secured overnight financing rate have increased significantly in early 2022 following a year-end regulatory deadline for banks to drop US dollar Libor from most new transactions.

SOFR’s share of the institutional US interest-rate swap notional transacted on Tradeweb has roughly doubled from December levels to nearly a quarter of overall volumes in early January, according to data from the trading platform. That still leaves a sizeable portion of activity in US dollar Libor – over 40%, with the remaining balance referencing Fed Funds – during what has been a particularly volatile period for government bond markets following increased expectations that the US Federal Reserve will soon raise interest rates.

Banks faced a year-end deadline to stop offering clients swaps linked to US dollar Libor except for trades that would help investors reduce risk tied to the old benchmark. Analysts say that has accelerated the transition to SOFR, but hasn't halted Libor-linked trading entirely as investors look to manage legacy positions.

“If clients want to trade Libor swaps and [they] say this trade in some way shape or form reduces my risk … banks can keep making those markets,” said one senior hedge fund trader.

The amount of swaps trading still tracking US dollar Libor underlines the scale of the challenge regulators face in fully ridding markets of the controversial lending rate, while also raising questions about how long such activity will persist. Even so, analysts say the steep rise in SOFR trading in recent days is an encouraging sign that the migration away from Libor is picking up speed.

“The transition to SOFR is happening. From what we can see, all new risk trades this year have moved to SOFR and any activity in Libor is really linked to portfolio maintenance and hedging of legacy positions,” said Colm Murtagh, head of US institutional rates at Tradeweb. “There’s still a lot of work to be done across the wider market, but in linear derivatives SOFR is now the main rate.”

US regulators’ efforts to eliminate US dollar Libor have stepped up a gear over the past year as they look to bring the market in line with other regions that have taken far bigger strides towards eradicating these troubled bank lending benchmarks.

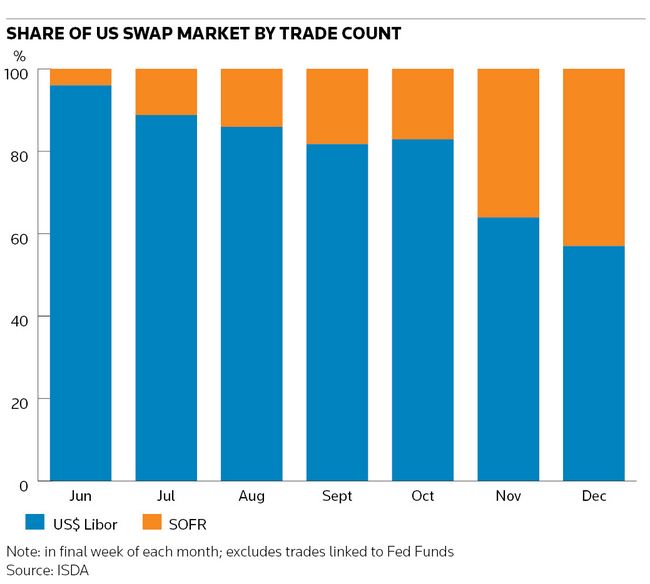

SOFR only accounted for about 4% of US dollar swap trades as of mid-2021, ISDA data show, prompting regulators to take a series of measures to encourage greater trading in contracts linked to the risk-free rate, which is their preferred replacement for US dollar Libor. Interest-rate derivatives are seen as a crucial component of the broader Libor transition as they account for the largest portion of the roughly US$220trn in US dollar-denominated financial instruments that reference the benchmark. Switching the interdealer swaps market to SOFR in July increased volumes and liquidity in these contracts over the following months and brought in more participants such as hedge funds.

Playing catch-up

US dollar swap markets still started 2022 with a mountain to climb even after these efforts. Nearly 4,000 swap trades referenced US dollar Libor in the final week of 2021, according to ISDA, compared to about 3,000 trades linked to SOFR. By contrast, Libor’s sterling replacement Sonia made up 97% of sterling swap trades in the final week of the year, while in Japanese swap markets the alternative rate Tonar accounted for 99% of volumes and in Swiss markets there were no trades at all linked to Swiss franc Libor.

Analysts caution against drawing firm conclusions from just a handful of trading sessions at the start of the year, but they say the early signs are promising in terms of the notable uptick in SOFR trading.

Moreover, some say the amount of Libor-linked trading this year may have been inflated by significant hedging activity related to swaptions positions following a steep rise in the 10-year US Treasury yield, which reached its highest level on Friday since before the pandemic.

“The market is moving around a lot. That generally creates a lot of hedging activity for investors with large swaptions positions, which are still mainly linked to Libor,” said Murtagh.

Murtagh said he expected more investors to trade out of US dollar Libor swaps and into SOFR later this year, particularly if Libor liquidity deteriorates. That potential for ongoing Libor activity is nonetheless a concern for investors keen for the market to unify around one rate as fast as possible.

"I just want to trade something that's liquid," said the senior hedge fund trader said. “If everyone converts over to trading SOFR swaps, and that’s the new thing, I’m totally good with that. But if all the liquidity is in Libor swaps then that’s a problem for me."