Signs that investors' desperate search for yield, so prominent in recent years, could be coming to an end began to emerge last week when a sharp rise in government debt yields claimed 2022's first deal casualty. And with the market going through the resulting readjustment, the going may be far from easy for some asset classes.

Austrian lender Raiffeisen Bank International was forced to pull the 15-year part of a dual-tranche covered bond exercise after lead managers (Barclays, BNP Paribas, Commerzbank, ING, Mediobanca and RBI itself) failed to muster enough demand for a €250m trade. And while the State of Berlin managed to get a €500m 30-year over the line, the issuer had to lean on lead managers who put in €125m of orders in the €500m book.

It is very unusual for a covered bond to be pulled. Especially in January and especially in recent years when central banks have unleashed vast amounts of liquidity into financial markets, leading to a compression in valuations across asset classes and leaving investors with little choice but to either go down the credit curve or move along the duration curve in order to make returns. However, that tide is turning as central banks begin to withdraw cheap liquidity and raise rates.

“The Fed has accounted for the vast majority of global QE, so once they start to tighten, everyone has to follow," said a head of syndicate.

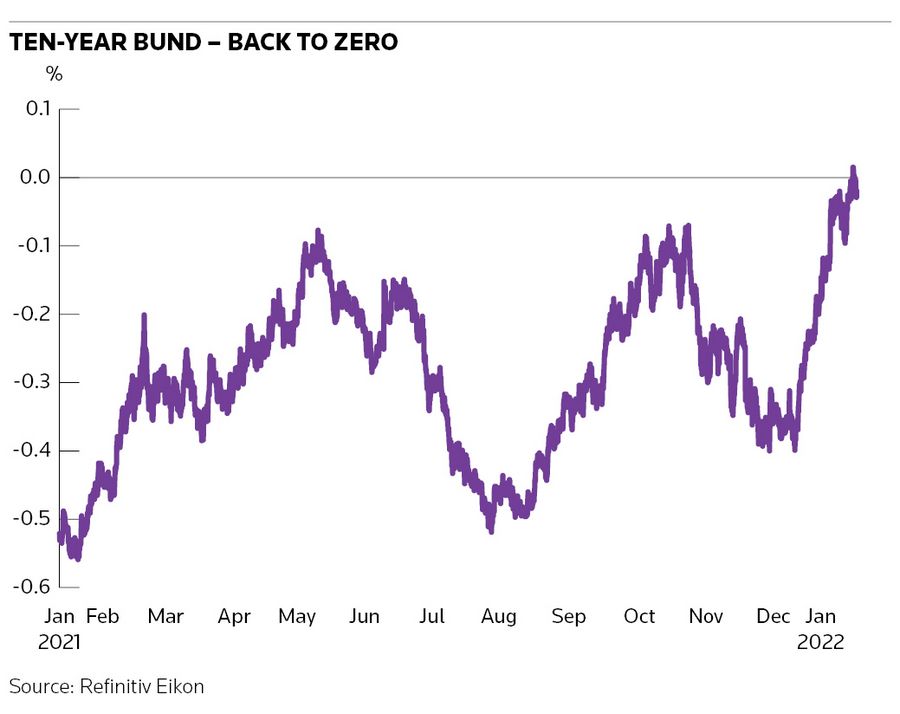

While the European Central Bank is not in lockstep with the US Federal Reserve, the pull higher in yields is still hard to resist. The 10-year Bund hit 0% for the first time since 2019 last week while two-year US treasury yields hit 1% for the first time since February 2020.

"In euros particularly, the big issue is the fact that we’re transitioning to a positive state," the head of syndicate said. "All our rates have been negative, so for a lot of people, going into a positive rate environment, that changes how you think about the opportunity cost. Where rates are negative, your opportunity cost is zero, that’s good enough. Now, there’s a good chance that the risk-free rate will have better value at some point and you have to look at things differently.”

Already, the universe of negative yielding debt has shrunk. Just over 52% of euro government bonds were negative yielding on January 18, well below the over 72% figure of December 2020. And recent issuance patterns suggest that borrowers are focusing more on the shorter part of the curve.

Ten-year SSA issuance, for example, has already reached €44.5bn this month, the highest volume of the last five years by the same point, according to IFR data.

"Duration is going to be a challenge," a head of DCM said. "EU sovereigns have flocked to duration in recent years. They've had it pretty good as investors moved along the yield curve but if we see the yield curve invert, who is going to want to lock in these rates at the long end?"

It is not just SSA borrowers that are going shorter. For covered bond issuers, the greatest depth of demand is below the 10-year point as shown by Bank of Montreal which priced a post-global financial crisis record-breaking €2.75bn five-year trade last week. Meanwhile, Banco Santander's €1.5bn three-year non-call two senior preferred was the first time the Spanish bank had raised such short-dated debt in a decade.

"If you come to market now with the high beta credit at the front end of the curve, it flies," said the head of syndicate. "It’s basically perfection. If you say buy 'high beta longer', I’m not even sure it’s a price discussion. I think people would say: 'I don’t need to take that level of risk to capture what I deem to be a sensible coupon or yield'. It’s a mentality change."

Not everyone is as gloomy about access to the long end, however.

"I think it's a nuanced story," another head of DCM said, adding that once the market stabilised, investors would return to the long end to pick-up levels they have not seen for some time.

"But while we have this volatility, investors are asking themselves: why take the extra risk when I can buy 10-year Bunds at zero and I can get much better yields than I am used to at the short-end."

Decompression

Still, it is not just duration that has become more difficult. Bankers expect that for those lower rated, riskier asset classes that have hugely benefited from the hunt for yield, market access will become more expensive and potentially more difficult.

"The hunt for yield trade was driven by ever lower interest rates, and when we see this back-up and expectation of more back-ups, then fundamentally that has to take the edge off that in terms of the demand," the second DCM head said.

Additional Tier 1 in particular has suffered. The Bank of America CoCo index closed at 4.105% on Thursday, almost 1% higher than the all-time low it hit in 2021.

"In AT1, you not only have the yield impact but also the convexity argument as well. So as soon as rates are going up, cash prices are going down, so call risk starts going up – you start pricing them to perpetuity and that magnifies the sell-off," the second head of DCM said.

With the hunt for yield no more, bankers expect the gap between credit to widen.

“Decompression will be a theme because now credit quality matters," the head of syndicate said. "There needs to be credit differentiation now."