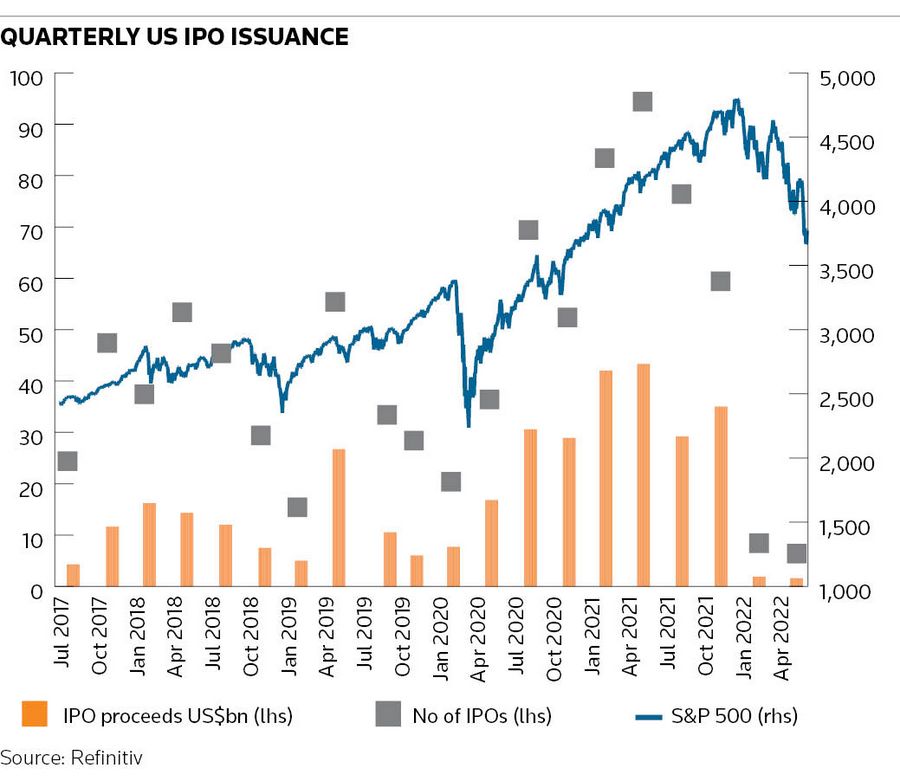

US ECM bankers are facing the slowest market for IPOs in more than six years with few obvious signs that conditions are about to take a turn for the better in the second half of 2022.

So far, just five traditional IPOs have priced for combined proceeds of US$1.6bn in the second quarter, the lowest by proceeds since the first quarter of 2016 and the quietest by deal number since Q1 2009, according to Refinitiv data (including only deals raising more than US$50m each).

If follows a first quarter where just US$1.9bn was raised across seven deals.

The first half of 2021 saw more than US$85bn raised as 175 companies listed on US exchanges.

The quarter is ending with a whimper as the US$180m NYSE American/TSX IPO of mining magnate Robert Friedland’s Ivanhoe Electric failed to price on Thursday night. The syndicate brushed off the delay as due to a technical matter and still hopes to consummate the deal early this week.

Assuming Ivanhoe prices in the coming week, the copper explorer’s IPO would rank as the first US new issue of substance in more than six weeks – since the US$288m debut of oilfield services firm Profrac on May 13. Profrac priced its IPO below range and its shares closed on Thursday only 2% above the issue price.

Slow going

Bankers are staring at a 95% slump in year-to-date IPO volumes with 2021’s record issuance led by a wave of highly valued technology and consumer companies an increasingly painful memory.

Rising interest rates in response to runaway inflation has stung growth stocks and means the average loss from the more than 300 traditional IPOs completed last year now stands at a staggering 45% (as of Thursday’s close).

The S&P 500 remains mired in a bear market (down 20.3% this year) but the pain has been even worse in the growth end of the market, with the tech-heavy Nasdaq Composite Index nursing a 2022 loss of 28.2%.

Bankers remain hopeful that more stable macro conditions and better markets in the coming months will restore IPO volumes. There is certainly no shortage of listing candidates.

“The backlog continues to be robust across products and regions, and issuers are open to executing when we provide them confidence in the certainty of the outcome,” said David Ludwig, Goldman Sachs’ New York-based global head of ECM.

“Once there is additional visibility in the trajectory of corporate profits, the markets will not only stabilise, but turn quickly," Ludwig said.

"We are encouraging both issuing and investing clients to stay nimble so they can have flexibility to act when the markets bounce back.”

Summer slowdown

Privately though, most ECM bankers are not expecting much improvement in the new issue market in the third quarter, which also has to contend with the usual summer slowdown.

Another senior banker said the reset in growth valuations did not appear to be over. Uncertainty ahead of the upcoming US mid-term elections in November presents another challenge for those looking to go public in the autumn, he said. Companies will also want to avoid so-called down rounds, in which they raise funds at lower valuations relative to their previous financings.

“I don’t think you will see a major improvement in the IPO market in the third quarter,” the banker said. “These companies can stay private. They are not rushing out to do a down round in order to go public in this market.”

The IPOs of AIG’s life and retirement unit Corebridge Financial and Intel’s autonomous driving software division Mobileye are among the largest IPOs expected to price in the next three months, but bankers now see little reason for either to push ahead until markets improve.

University of Florida professor and IPO expert Jay Ritter said the multi-year downturn in IPO volumes was not unprecedented (similar scenarios occurred after the early 2000s tech correction and the 2008 financial crisis) but much now depends on the performance of the stock market.

“Part of last year’s boom was not just that the stock market had been in an 11 to 12-year bull market but also that the valuations of growth companies went higher and higher. [The overvaluation] last year was not as unambiguous as the late 1990s but it was getting harder and harder to justify the price-to-sales ratios,” Ritter said.

“The main issue is that a lot of VC-backed companies were getting very attractive valuations in private markets and whether they are talking about private or public markets, now the likelihood of a down round is very high,” he said.

But with both VC and buyout firms possessing high levels of dry powder, companies could use so-called ratchets (extra shares to compensate for lower valuations) and other investor-friendly terms to raise money and “hide” their valuation declines, Ritter said.