IFR: I’m delighted to welcome everyone to the Thomson Reuters IFR Seminar, sponsored by Daiwa Securities, HSBC and Moody’s Investors Service. To kick off this debate, I’d like to ask each of our panellists to introduce themselves with a few words on how they see the development of Asia’s bond markets.

Thierry de Longuemar, ADB: The question is: Can Asia fulfil its bond market ambitions? When you look at the finance sector in Asia, it’s led by banks. Assets held by banks in Asia are about four times the size of the outstanding bond market. It’s exactly the opposite in the US, so there is clearly a gap. That means the short answer is ‘yes’. Yes, because it will have to. Yes, because bond markets have been proven to be more efficient as a means of financing the economy than bank finance.

Yoshihiro Inoue, Daiwa Securities: I’m not an expert on these academic issues, but maybe I can comment on some practical ideas. From my experience with credit enhancement in the Samurai bond market, the first issuance with a guarantee from JBIC came from Indonesia. Now this market is growing significantly, but this first issuance was able to offer some investment opportunities to Japanese investors.

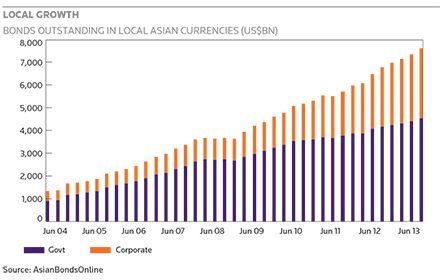

Reza Siregar, AMRO Asia: The ASEAN+3 Macroeceonomic Research Office was established in 2011 to work closely with the IMF to provide surveillance reports on the ASEAN+3 economies. One of the concerns we are actually looking at quite closely is financial market development. As you know, bond markets have been increasing significantly since 1997. In ASEAN alone, we have over US$18trn outstanding in the bond markets, and most of them are still pretty much sovereign bonds. We are looking at the development of the bond markets, and also how to ensure the stability of that process.

Alexi Chan, HSBC: HSBC is a strong supporter of the Asian bond markets. We have a highly developed infrastructure supporting the development of both global and local bond markets across the region, leveraging off our on-the-ground presence in many of the key financial centres in Asia.

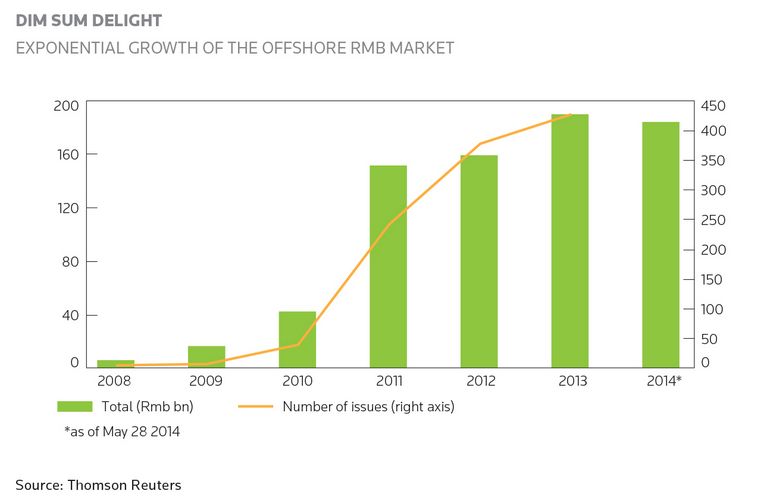

Our answer, in line with Thierry’s, is yes, we absolutely agree that Asia can fulfil its bond market ambitions. We’ve seen many developments in this space in recent years, the most significant and exciting of which has undoubtedly been the development of the offshore renminbi market, the so-call Dim Sum bond market, which has been a key element in the ongoing trend towards creating a deeper capital market in Asia.

Tom Byrne, Moody’s: What we’ve observed is that the Asian bond markets, and in particular the local currency bond markets, have indeed grown fairly rapidly in the past decade, and some of this growth was in part down to the Asian Development Bank and the East Asia Pacific Central Banks Association. It’s underpinned by the lessons learned from the Asian financial crisis, where the excessive reliance on intermediated credit through the banks contributed to the severity of that crisis.

I also think the growth and the increased sophistication of the East Asian bond market has played a role in allowing the region to respond favourably, at least relative to other regions, to the global financial crisis. The fact is that during the global financial crisis there was a sharp reversal of portfolio inflows into the Asian region, however the issuance of local currency bond markets continued almost apace throughout the crisis, and this has imparted some resilience to the financial systems in the region. It also reflects, or supports, the sovereign rating upgrades that we’ve done in Moody’s since the global financial crisis.

Turning to the role of rating agencies, we feel that ratings do not make a healthy bond market, rather they reinforce a healthy bond market. And for us a healthy bond market is one in which there is an environment of debate and dialogue is encouraged, and more rather than fewer opinions are available to the market. We think more opinion improves the efficiency of markets, and the overall health of credit markets.

IFR: We’re going to focus most of our time today looking at the local currency bond markets across Asia, and I’d like to start by asking Thierry to speak a little bit about the ADB’s initiatives there.

Thierry de Longuemar, ADB: Thank you. We’ve been a promoter of developing bond markets across Asia for a long time. We did the first Samurai bond ever in the Japanese market in 1970. That was 44 years ago, and Japan is no longer a developing country. More recently, we’ve been active in the Indian rupee market since 2004, in the Chinese RMB market in 2005 and 2009, and we did the first significant offshore RMB issuance in 2010. We have also been active in Malaysian ringgit, Philippine peso, Thai baht, and other markets including Kazakh tenge. We actually issued a tenge bond in 2007, which means there is potential there. We are also looking at the Nepalese market, the Mongolian market and others.

Just briefly, when it comes to issuing in a developing market, we aim to achieve a number of things. One, introduce best practice. We are a well-known issuer in the global capital markets and we strive to introduce that kind of best practice in the local markets.

Two, contribute to building yield curves and benchmarks, which should enable the development of those markets, particularly the corporate bond market.

Three, deepen liquidity. Many of those markets, at least at the beginning, lack liquidity, and that prevents new issuers from tapping those markets. We want to contribute to deepening liquidity in those markets.

Four, introduce the best regulations. Before we issue we have long discussions with regulators, and we try to suggest some adjustments when needed to enable the bond market to be more effective.

Five, we are also tasked with modernising settlement operations. Many of those local markets lack some essential clearing, settlement and listing practices, and we aim to introduce those when we issue in a new market.

Six, rating. Our issues are always rated, and in some markets there is little practice of rating. We value that greatly because it is a way to introduce a new pricing culture, and that is needed when you want to develop a proper bond market.

Seven, contribute to financing the economy. We generally tap those markets for maturities beyond five years. Because as I said most of those markets are bank-led, but banks seldom lend beyond five years. We want to complement what those banks are offering and in a way contribute to financing those economies.

IFR: Can we touch on the ADB’s involvement in things like the Asian Bond Market Forum, and any moves to unite some of these local markets?

Thierry de Longuemar, ADB: Beyond being an issuer, we are also actively engaged in the ASEAN+3 initiatives, including the Asian Bond Market Forum, set up in 2010, which is a platform to foster standardised market practices and the harmonisation of regulations related to cross-border bond transactions in the region. I could have said more about the need for cross-border integration, and a lot is being done under the auspices of the ASEAN+3.

IFR: Let’s bring in our dealmakers for a second here. What does it take to get an investor to look at a different currency bond for the first time?

Alexi Chan, HSBC: There are many different facets to developing local bond markets. The natural place to begin is with a well-functioning government bond market, and most sovereigns in Asia have taken steps to deepen and develop their market, and facilitate access for overseas investors. For example, HSBC worked with the Kingdom of Thailand to introduce the first inflation-linked bond issue in South-East Asia in 2011, which was a major step forward for the development of that particular local market.

The next phase is to move beyond a rates market to a well-developed credit market. As my fellow panelists have mentioned, Asia’s credit markets were originally very much dominated by bank lending, done with varying degrees of rigour. We’ve been working hard to promote a genuine credit culture across the various bond markets in Asia. The final element is to put in place the infrastructure in each local bond market that helps make it accessible to a wide range of international investors and issuers. That, if you like, is the holy grail of a pan-Asian bond market, but it’s not necessarily the overriding objective. The first priority for the Asian bond markets must be to provide a deep, source of finance for local companies to raise term debt as an alternative to the bank markets.

International diversification is clearly also an important step, and there are a whole range of factors that determine whether a market is accessible to international investors. Clearing systems are an important part of this: it may be unrealistic to expect all relevant global investors to set up custodian arrangements in each of Asia’s local debt markets. Similarly, the depth of cross-currency swap markets is also a critical factor in the accessibility of these local currency bond markets both to international issuers and investors alike. Those are just a couple of the themes which form part of the agenda for developing a deeper bond market in each Asian market.

IFR: One of the things that has been helping international interest is credit enhancement. Inoue-san, you mentioned the JBIC-backed Samurai bond, for instance, and there has been some development in Indonesian rupiah as well. Is there more to do there?

Yoshihiro Inoue, Daiwa Securities: Since Prime Minister Abe began the Abenomics programme, we have seen the Japanese Nikkei equity index rise, and risk appetite among Japanese institutional investors is rising. They are now looking to take more credit risk. This kind of trend is already happening. Japanese investors have started to buy very aggressively on the equity side, coming into the Indonesian or Thai stock markets. One of the reasons is that they can see the liquidity and the price, and the problem for the bond markets is they cannot see if a bond is liquid or not, or where this bond is priced as other banks are providing different prices. It’s not transparent – Japanese investors need that.

Japanese institutional investors are quite conservative, since they are company workers and they don’t want to take the risk, but the retail investors are very happy to take risks. We have been selling them bonds in Turkish lira, South African rand, Brazilian reais, so there’s a lot of demand if we can create the opportunity for Japanese money to come into the Asian bond market.

On credit enhancement, I mentioned the JBIC Samurai bonds. Unfortunately there is no sub-investment grade bond market in Japan’s domestic market, so that is the reason why we are providing this kind of credit enhancement to those issuers who want to tap the Japanese market. Another important thing is name recognition. Samurai bond issuers, for example Single A rated foreign names, need to pay 50bp higher spreads than Japanese issuers with the same rating. This kind of premium is because of the lack of name recognition. This will happen to other markets as well, if Indonesian issuers want to come to Thailand and their name is not recognised, I don’t think Thai institutional investors will be comfortable enough to buy that name. Name recognition is also very important in developing cross-border interest.

IFR: The impetus behind a lot of the developments we’re talking about here seems to be coming from regulators rather than from market forces. Tom, do you agree with that? And is that the right way for markets to develop?

Tom Byrne, Moody’s: I think that’s a good question, but I’m not exactly sure how to answer. If you look at overall local currency issuance volumes in Asia, it’s really being driven by China, where many local corporations are affiliated with the state. So is that being driven by the authorities promoting an alternative to the banks? Yes, in part, because of the regulatory restrictions on bank credit and efforts to rein in shadow banking. But on the other hand there is some growing maturity on the part of issuers looking to go elsewhere. Now for any market to grow in liquidity there has to be improved information and improved disclosure – it all works together. Perhaps the panellists who are in the market can comment on the impact of regulatory moves to develop market infrastructure.

IFR: That certainly makes sense. Initiatives like the Credit Guarantee and Investment Fund have been in place for a while now, but they seem to be taking time to build traction. Alexi, what’s your view on how hard it is to bring these deals to market?

Alexi Chan, HSBC: We certainly welcome the initiative of a CGIF guarantee from the ADB and ASEAN+3. It’s designed to facilitate cross-border issuance in Asia’s local currency bond markets, and mitigates some of the credit decisions that investors would need to make around a specific name. We’ve had some encouraging steps in the right direction recently with such credit guarantee mechanisms. These represent an intermediate step to a more broad-based pattern of cross-border issuance within Asia and from issuers further afield.

HSBC led a landmark transaction in 2013 on behalf of Noble Group, the Hong Kong-based commodity operator, in the Thai Baht market with a CGIF guarantee. The use of a guarantee structure was crucial in enabling the company to access the Thai market, and thereby diversify into a new investor base. Initiatives of this sort are very helpful in promoting wider access to Asia’s local bond markets, but they probably address only one or two of the points on Thierry’s list. For deeper cross-border flows across the regional markets we will need to see progress on other measures as well, including things like secondary market liquidity, settlement systems and so on.

IFR: When we look at the potential downside from some of these cross-border developments, Reza, is your office concerned about the build-up of international credit in Asia?

Reza Siregar, AMRO Asia: The governments of ASEAN+3 are very committed to the development of bond markets in the region. We learned from the East Asian Financial Crisis in 1997 that we depend too much on the banking system. There we had a problem not only with the connections risk but also the mismatch in maturities between long-term projects and lending that is typically short-term in nature. So the commitment to the bond market by the ASEAN +3 is indeed there. And this is something that most of our governments are working closely on, together with the ADB and other institutions, to help boost liquidity and develop market infrastructure.

As far as my office is concerned, what we do when we look at financial market development – whether it is a deepening of the banking system, or credit enhancement in a country like Cambodia or Myanmar, or the development of the bond market in Thailand or Malaysia – the main thing we are looking at is whether there is potential for a certain type of volatility that we need to understand. In our economy, as I said before, out of that US$18trn of bonds in ASEAN+3, roughly about US$15trn–$16trn are still sovereign bonds. Treasury bonds are there to help manage fiscal funding, but it also comes from an intervention policy to allow intervention from the central bank or from fiscal policy, so it’s closely tied to the operation of macroeconomic stability. So when we’re looking at this kind of financial market development we’re also looking at whether there is any impact of this kind of development in the bond market to our fiscal sustainability.

Just to give you a concrete example, when we had a massive QE in Europe and the US, what we have seen is that the cost of borrowing in our economy has gone down significantly. That actually facilitates a lot of fiscal funding in this part of the world. But, at the same time, we have to be sure that governments understand that those low costs of financing might not continue to exist. Eventually, when you have a normalisation of the credit curve and the interest rate, that cost should go up again, so we have to anticipate that possibility because it will feed into our bond markets as well. We have seen, for instance, since the Bernanke statement on tapering in May 2013, that yields started to go up in some of the bond markets. Again, anticipating some normalisation of interest rates in the US, that will feed into corporate funding costs and the fiscal costs of our macroeconomic policy. As our panellists have said, the costs to companies have gone up, and this is one thing that we are monitoring quite closely.

Just one more thing to add, while local currency bonds have reduced exposure to foreign exchange risk, we also look closely at investor risk. We watch closely, for instance, the types of investors that are investing in these kinds of bonds. It can be quite critical if the institutional investors are predominantly pension funds or some other type of institutional investor.

IFR: How much of the 2013 sell-off in India and Indonesia was down to foreign investors in those markets?

Reza Siregar, AMRO Asia: That’s actually a very good question. The regional investor continues to be bullish on the region, despite the fact that there are some concerns. There is some moderation in the size of investment, but in general we have found the regional investor continues to be quite active. But we do find fund managers based in Europe or in the US have shifted a bit. In the case of India and Indonesia it could be in part due to the macroeconomic situation – typically, in addition to market infrastructure, investors will look closely into the macroeconomic performance, balance of payments, current account positions, fiscal deficits. Those kinds of things have been quite influential among foreign investors.

IFR: The offshore RMB market is developing in an alternative way to some of these other local currencies, more along the lines of the standard Eurobond format. Alexi, what’s going on there, and how does that contrast with some of the other developments we’ve seen?

Alexi Chan, HSBC: The growth of the offshore RMB market has been one of the most significant developments in Asia’s bond markets in the last few years. The market developed in Hong Kong starting in 2010, based on a rapid growth in RMB deposits and, with the support of the Chinese authorities and a relaxation in regulations regarding use of proceeds, an offshore RMB bond market came into fruition. Clearly the ability for both international issuers as well as issuers from China to raise RMB offshore, in a format that is essentially identical to a typical Eurobond, and potentially bring those proceeds into China, has been a major development.

It’s been interesting how the market has developed – and to the earlier question of whether market forces or regulators (or other official bodies) can drive these forward – I think we need both factors for any Asian bond market to work efficiently. In the case of the offshore RMB bond market, we have seen regular issuances from the Chinese Ministry of Finance itself, coming into the market on an annual basis and issuing across tranches to build an offshore yield curve and help to promote liquidity. From HSBC’s perspective we have established a 20%-plus market share as the #1 underwriter of offshore RMB bonds, and we’ve have invested significant resources in facilitating the development of the market. This includes a commitment to secondary market trading and the development of a cross-currency swaps market, and these elements have facilitated access for a number of international issuers who’ve tapped the offshore RMB market to broaden their investor base. We’ve had issuers from a very diverse range of jurisdictions, from Western Europe, the US, Latin America, Russia and from other Asian countries. Some are using the proceeds to fund their operations in China, some for cross-border payments, and others are looking to execute a cross-currency swap back into, say, US dollars or another currency.

Clearly as we see China continuing with capital account liberalisation we’ll see the offshore and onshore RMB bond markets progress and converge, and that’s going to be a very interesting development to watch. The offshore RMB market is a unique phenomenon in Asia, and has provided a new dimension to the debate on Asia’s bond markets.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.