Identifying opportunities

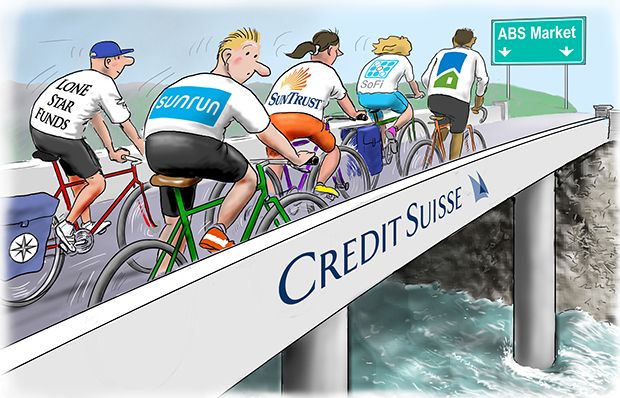

Sweeping changes were afoot this year at the world’s best-known investment banks as newly-installed top brass slashed jobs, pared business lines and vowed to boost capital. But Credit Suisse demonstrated that its global structured finance business knows how to earn its keep, making it IFR’s Structured Finance House of the Year.

Credit Suisse’s structured finance team showed its prowess during the past year by piloting 11 first-time issuers through a tough market. Heightened volatility that took hold in the second half of the year left many of the bank’s rivals either reliant on fees from cookie-cutter deals – or on the sidelines completely.

But rather than ducking for cover, the Zurich-headquartered investment bank instead channelled its focus towards expanding in 2015 by undertaking the difficult task of ushering nearly a dozen newcomers through the securitisation process.

That push is expected to differentiate the bank in the years ahead as it continues to cultivate one of the industry’s more robust and diverse global securitisation franchises.

Already the team’s strategy of keeping nimble while staying patient in slower-burn areas with big growth potential has paid off.

Its savvy in both respects spared the Credit Suisse securitisation team painful cuts experienced by other franchises in the past year, including keeping its robust private-label residential mortgage business intact.

Competitors, including RBS and Deutsche Bank, have turned their backs on the once highly lucrative private RMBS business following recent senior management changes. But with their loss, Credit Suisse appears poised to seize opportunity.

“Amid all that discussion about change, the one thing that stands is that the securitised products strategy remains consistent,” said Jay Kim, the bank’s head of securitised products asset finance. “There was no change to our capital allocation or to our geographical footprint.”

The team completed marquee securitisations during the year that spanned jurisdictions unreached by their competitors, ranging from the UK mortgage market to the US solar ABS industry to Asian unsecured consumer loans.

Expansion

And while new Credit Suisse chief executive Tidjane Thiam said in July that he planned to “right-size” the investment bank by focusing on more highly profitable and capital-light areas of finance, its structured finance group emerged unscathed.

While up to 2,000 jobs will be cut from the bank’s London investment banking operations, Kim told IFR that his group actually had plans to grow the business in 2016.

“I think the reason we’ve been insulated is because we already adapted to a lot of the regulatory changes, and changed our business model,” Kim said.

Credit Suisse has made a niche out of structuring off-balance sheet transactions through the issuance of credit-linked notes. And the bank has captured a 65.5% market share of the US$19bn of balance-sheet optimisation securitisations created and sold since 2011.

“Within the regulatory framework, the only means for achieving capital relief through a securitisation is by selling all of the economic interests,” said Jon Claude Zucconi, a Credit Suisse managing director. “[But] it’s going to be structures like this that US banks look to in 2016.”

The bank also dominated as a go-to source in the residential mortgage market.

Credit Suisse ranked number one in both jumbo RMBS and in non-performing and re-performing home loan securitisations over the past year, which saw a combined total of nearly US$30bn in transactions completed by November.

United Guaranty

Away from purely non-agency mortgage securitisations, it also led United Guaranty’s first securitisation of mortgage insurance policies since the crash. The US$300m transaction, called Bellemeade Re Ltd Series 2015-1, was priced in July and paid investors roughly 2.5% on the one-year, 4.3% on the three-year and 6.3% on the four-year notes.

The trade, which took roughly a year to come to fruition, came just before spreads started to gap out to multi-year wides.

“We needed a bank that we felt had the capacity to do new and innovative things,” an executive close to the transaction told IFR. “Obviously, Credit Suisse’s position in the MBS or mortgage credit space speaks for itself.”

The bank beat roughly a half-dozen other investment banks competing for the mandate. But ultimately, the executive said, Credit Suisse prevailed due to its expertise in structuring prior Freddie Mac and Fannie Mae credit-risk transfer bond deals.

“We were able to raise capital for [United] at Libor plus 400bp, which is obviously dramatically lower than if they were to go out and capitalise,” said Mike Dryden, a managing director at Credit Suisse.

In terms of other debuts, US solar company Sunrun also tapped Credit Suisse for the successful completion of its inaugural US$111m ABS trade in June 2015. The bulk of the seven-year debt financing was oversubscribed and priced to yield 4.45%–5.45%. Indeed, the longer-term securitisation financing got done under the wire before increasingly volatile winds blew through financial markets.

Another notable transaction was speciality retailer Conn’s US$1.1bn unrated subprime ABS of consumer instalment loans, which was 11 times larger than its last transaction in 2012.

“They delivered on what they promised they could deliver,” said Mike Poppe, Conn’s chief operating officer, of Credit Suisse.

Why go with CS?

In Europe, meanwhile, Credit Suisse led the way in portfolio sales of legacy mortgage books, most notably arranging a massive £1.6bn acquisition financing for the Project Landsdowne trade in July.

The deal saw Irish lender Permanent TSB sell its Capital Home Loans platform to US private equity firm Cerberus Capital, along with a £1.9bn portfolio of primarily UK buy-to-let mortgages.

Credit Suisse had to provide a same-day closing financing package for the deal to work, which was no mean feat due to the challenging timing. With tensions around Greece at their height, spreads in the secondary market were blowing out dramatically, making the prospect of publicly selling the RMBS piece particularly difficult.

But despite these headwinds, Credit Suisse was able to upsize the Auburn 9 deal to £525m from the initial target size of £300m. Of this, £483m was placed with investors, making it the largest placed UK buy-to-let RMBS deal post-crisis.

As well as being sole arranger on the public RMBS deal, CS also arranged a £1.16bn private warehouse facility, which was syndicated to five lenders.

The two-year facility will act as a bridge to future securitisation take-outs.

As well as arranging the large acquisition financing package, Credit Suisse acted as buyside adviser to Cerberus throughout the acquisition process. This also included advising on portfolio selection, with the buyer selecting the final portfolio from the entire £4.5bn mortgage book owned by Permanent TSB.

Portfolio sales such as Project Landsdowne are expected to drive the European securitisation market in 2016 and by arranging a same-day financing package, with both public RMBS and private warehousing, Credit Suisse has provided a crucial template for others to follow.

The buyer Credit Suisse advised is also asserting itself as the foremost purchaser of legacy mortgage books. Cerberus bought £13bn of former Northern Rock mortgages – which includes the famous Granite portfolio – in November, which is earmarked for securitisation next year.

To see the digital version of the IFR Review of the Year, please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com .