Asia’s investment banking industry has been through its fair share of upheaval over the past 20 years, and regulatory pressures and rising competition are adding to the challenges. What does it take to be successful in Asian banking today?

Twenty years ago Asia’s top international debt underwriters were all global names, with little competition from regional players, and names like Peregrine and Barings still featured on the region’s equity charts.

Investment banking in Asia in 2017 looks very different. The Asian financial crisis, dotcom bust and global credit crisis have put paid to many firms’ ambitions, while the region’s own growth has seen local players displace their global rivals.

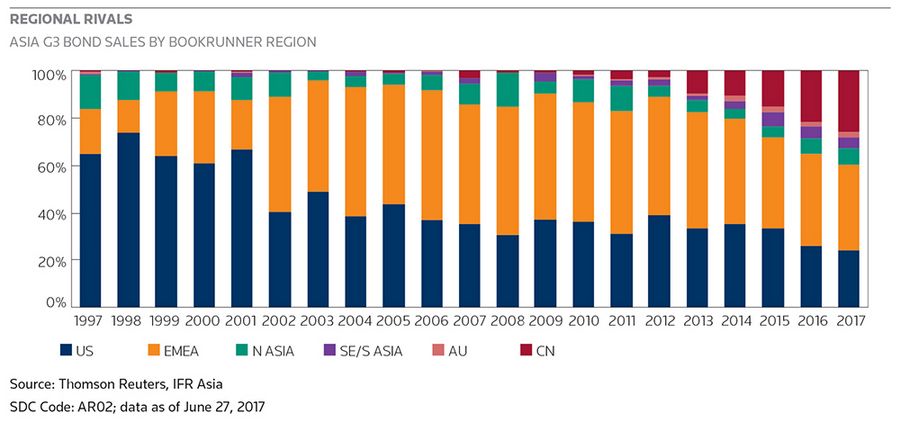

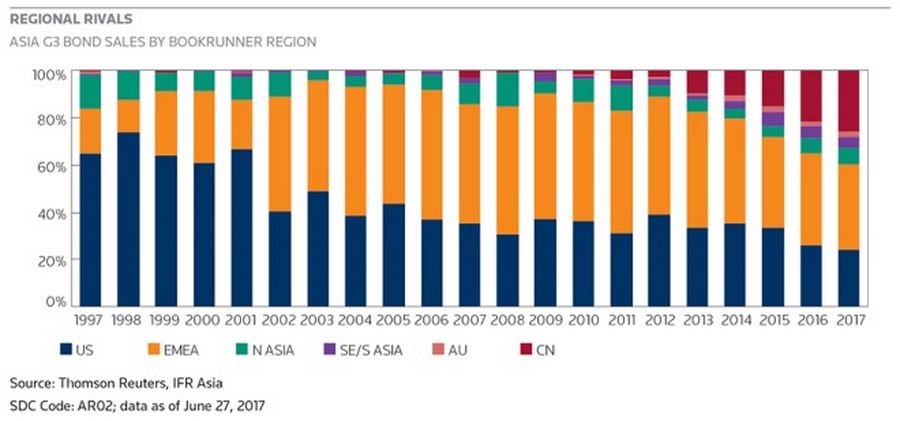

US underwriters accounted for 65% of all bonds sold in G3 currencies in Asia in 1997. In the first half of 2017 that figure was down to 24%. European lenders have given way to regional banks, who are happy to channel surplus deposits into low-margin loans for local borrowers.

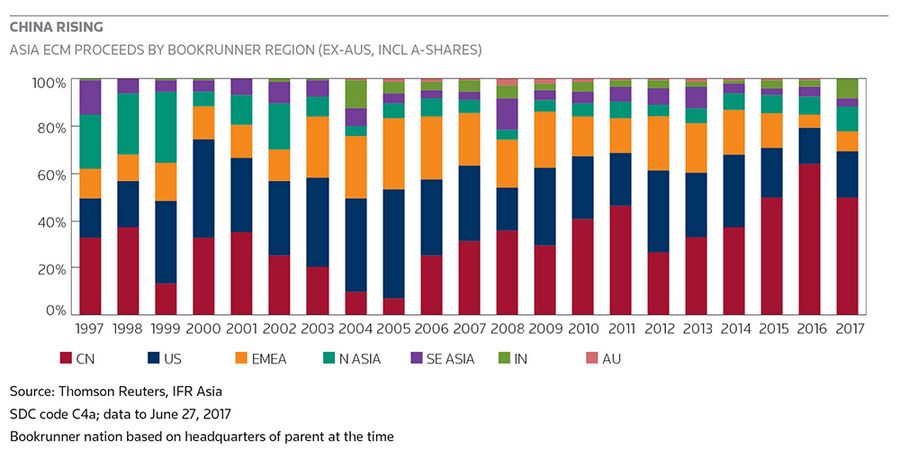

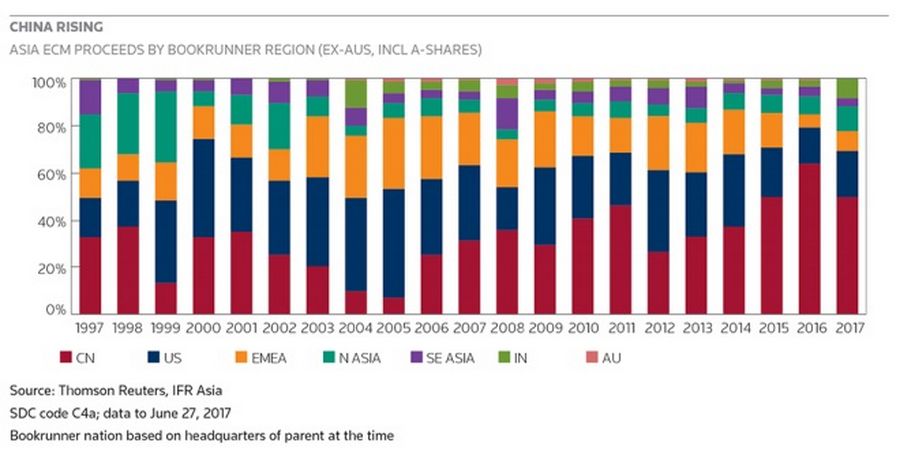

In the equity markets, Chinese firms underwrote 64% of all common stock sold in Asia, including Australia, in 2016, up from 33% in 1997 and a low of just 7% when A-share IPOs were frozen in 2005.

The shifts in market share are well documented. But questions over the outlook for Asian investment banking remain unanswered. Can global players still make ends meet in the region? Can local firms adapt to tougher capital adequacy requirements? Are new competitors diluting standards?

Other questions go deeper still. Is the entire banking industry under threat from the technology sector? Have the reforms since the last financial crisis left investment banks permanently crippled? And does anyone really want to work for a bank anymore?

For those who have been around a long time, some of the magic has certainly gone.

Francis Leung Pak-to, known as the “father of red chips” for his work on Hong Kong listings in the 1990s, believes the nature of the job has changed.

China Rising

“I joined the industry in 1980 when we were still called merchant bankers. We were well respected and trusted advisors for the bosses. Being a banker was inspiring and fulfilling,” said Leung, who built Hong Kong-based Peregrine into the region’s leading stock underwriter before the 1997 crisis and is now senior adviser to private equity firm CVC.

Leung argues that private-sector clients value advice and ideas, but the expansion of Chinese state-owned enterprises has transformed the market – and not necessarily for the better.

“Everything changed when SOEs started listing in Hong Kong. Relationship is what matters most in securing those mandates.”

“The SOE IPOs have turned the investment banking industry into a commodity business,” said Leung.

China’s growth poses several challenges for the established international banks. Mainland financial institutions have already pulled down loan margins and squeezed advisory fees across the Asian market as they have followed their domestic clients overseas, but further disruption may be more serious.

Farhan Faruqui, CEO of international banking at ANZ, sees a greater existential challenge.

“The biggest change has been the arrival of Asian liquidity, in particular Chinese, and the rise of regional and Chinese players in the banking sector,” he said. “Global banks are fighting hard to stay relevant and to compete against Chinese banks”

Chris Laskowski, head of corporate and investment banking for Hong Kong and head of financial sponsor coverage throughout Asia at Citigroup, sees Chinese money playing an even more dominant role in Asian finance in the future than it does today.

“At some point, the capital markets are going to gravitate to China,” said Laskowski. “The A-share and domestic Chinese capital markets have their own peculiarities but they’ll figure it out. I think that’s the biggest challenge looming on the horizon for Asia investment banking.”

“The biggest change has been the arrival of Asian liquidity, in particular Chinese, and the rise of regional and Chinese players in the banking sector. Global banks are fighting hard to stay relevant.”

Laskowski points to the development of the leveraged finance market as an example of Chinese banks’ rapidly growing influence. The buyout of US-listed Focus Media in 2013 came with a US$1.7bn loan with Citigroup and Credit Suisse as the original arrangers. Later financings had a much more Chinese flavour, for example with Bank of China going it alone on a US$1.9bn financing to back the proposed acquisition of Philips’ Lumileds business in 2015.

“When we did Focus Media we were able to hold on to a leading role because Chinese banks didn’t know how to do leveraged finance. Now those same banks are tightening margins and terms,” said Laskowski.

“Frankly, for the leveraged finance product we tend to target large, complex and multi-jurisdictional transactions where we can add meaningful value to the issuer.”

The way deals are done in the debt and equity capital markets has changed, too. The expansion of dozens of Chinese brokers into the overseas market means that giant underwriting syndicates are now standard practice on Chinese IPOs, especially from China’s public sector.

Mark Machin, president and CEO of the Canada Pension Plan Investment Board and a former head of Asian investment banking during a 20-year career at Goldman Sachs, is not a fan of the new model.

“It’s like two, three, four or five people appointed to drive the car all at the same time. You can have some people hold the steering wheel, someone press the brake and someone change the gears. But that’s not natural, efficient or effective,” said Machin.

Overall commissions are also lower, making it hard for individual firms to make ends meet. Major Chinese SOEs now typically pay less than 2% in underwriting commissions for their overseas listings, far less than in other markets. One Chinese investment bank recently offered to work on the US$1bn Hong Kong IPO of Shandong Gold Mining for an underwriting fee of just 0.2% – a level that one international rival quickly dismissed as “insane”.

RISING TIDE?

To some extent, the overall growth of the Asian markets means there is more cake to go round, even if there are more mouths to feed. Mergers and acquisitions, driven by outbound Chinese purchases, hit a record in 2016, and international bond sales are heading for another US$200bn-plus year, more than four times bigger than before the 2008 credit crisis.

Robert Scholten, who has worked in Asia with ING since 1991 and is now head of Asian real estate finance, argues that the growth of local and regional institutions has created new opportunities for global firms.

Asia, he says, has transformed step by step “from basically being the factory of West to a self-contained economic power block, exporting its wealth to the West”.

The emergence of liquid domestic capital markets across Asia, the consolidation of Asian banks and rapid wealth accumulation have raised demand for more sophisticated financial products and advice from both companies and investors. Scholten sees the growth of overseas acquisitions from Asian companies as part of a trend that also includes local non-bank financial institutions investing overseas primarily to diversify their risk into stable, revenue-generating assets.

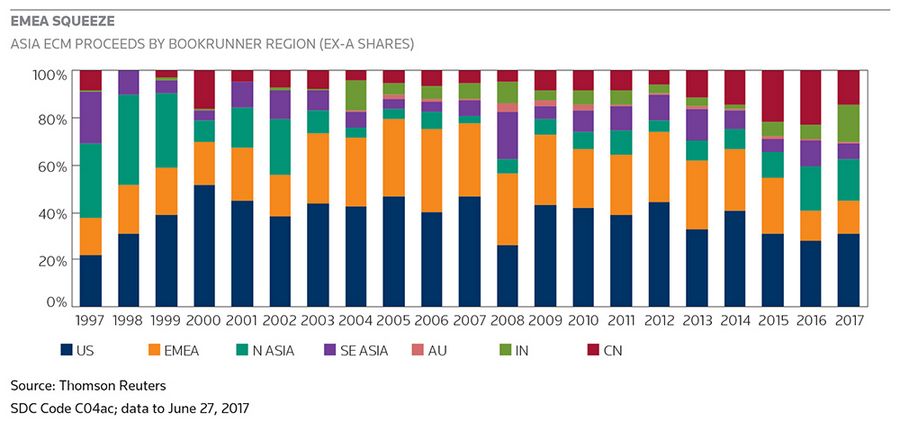

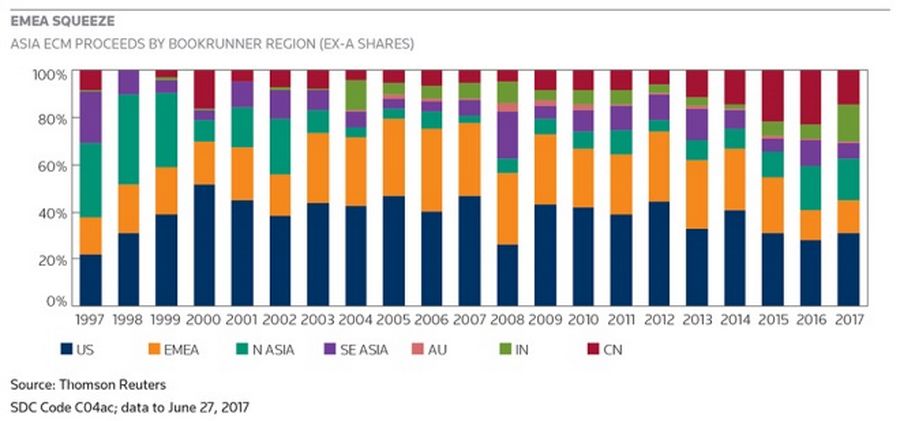

EMEA Squeeze

“These outbound trends play into the strengths of international global banks as they are able to leverage their global network, inter-regional connectivity, as well as local product and sector expertise when offering banking and advisory services to Asian companies and financial institutions in support of their overseas strategies,” he said.

Paul Yang, head of Greater China at BNP Paribas, agrees that foreign banks do still have a role to play in the growing Asian market.

“Think how much China’s GDP has grown over the past 20 years,” he said. “It’s like when Macau opened its gaming market. Yes, Stanley Ho’s market share has gone down, but the whole market today is so much bigger.”

Yang sees a viable future for banks offering a diverse range of products for a clearly defined group of clients.

“Anyone who set out on a single strategy in investment banking has taken a serious hit,” he said. “Anyone only targeting capital markets business is now struggling, because of the Chinese (rivals). Anyone only offering balance sheet liquidity is facing competition from the Chinese lenders. You have to be extremely diversified.”

Attitudes to China are divided. Some global banks, including RBS and JP Morgan, have recently severed ties with their securities joint ventures and others have sold their strategic stakes in Chinese banks. On the other side, however, are institutions looking to China for growth. That includes the likes of Credit Suisse, where CEO Tidjane Thiam has put China at the central of an ambitious Asian expansion plan, and HSBC, which has just won approval to open a joint venture in Shenzhen’s Qianhai district, where it will have a majority stake.

Both sides share a common driver, however, in regulation. Tougher capital adequacy rules and compliance requirements have squeezed returns across the developed world, and made it more expensive for banks to maintain a minority investment in any business. At the same time, China is gradually opening its onshore markets, allowing foreign investors, issuers and underwriters to participate in the domestic bond arena.

REGULATORY CHALLENGE

Bank capital requirements have transformed banking globally, but the contrast between the pre-crisis years and today is especially striking in Asia, where lenders enjoyed years of good returns.

“Nobody worried about capital,” said Faruqui. “Risk was low, and losses even during SARS or the dotcom bust were limited.”

Faruqui does not believe the good old days will ever come back, regardless of recent US moves to review the Dodd-Frank act, imposed in 2010 to safeguard US taxpayers from the risk of another financial crisis. President Donald Trump has called the legislation “horrendous” and proposed revisions that would remove some of the burdens on banks. The House of Representatives passed Trump’s proposals in June, but the measures have yet to clear the Senate.

Major banking stocks have rocketed: JP Morgan has gained 36% since Trump’s election and hit a record of US$94.51 a share in early July.

“For younger talented individuals who want to build a business, be opportunistic, take the initiative, they want to be working for a tech firm, or a privately held enterprise like ours.”

European regulators have struggled to build a consensus for the so-called Basel IV proposals, which could squeeze bank capital ratios further by increasing risk-weighted assets. But other pieces of legislation are arriving all the time. The European Commission has set a deadline of January 2018 for compliance with the Revised Markets in Financial Instruments Directive (MiFID2), and is beginning work on a review of the European Market Infrastructure Regulation (EMIR). There are also calls for tougher rules on total loss-absorbing capacity (TLAC) for the world’s biggest banks, and a binding total leverage ratio.

“We’ve gone from a period of feast to a time of more fasting,” said Faruqui. “Anyone who thinks it’s coming back is just in denial.”

Stricter bank regulation is here to stay, says Michel Lowy, who left Deutsche Bank to co-found high-yield debt specialist SC Lowy in 2009.

“A deposit-taking institution that is taking risk can have a systematic impact on the whole banking system, and it’s logical that regulators have to create some heavy infrastructure to protect the taxpayer from those risks,” he said. “The implementation of those rules means the decision-making process is slow. The back office and management is a lot heavier than it used to be. And I think that’s all justified.”

In certain segments, the impact of these changes leaves banks at a disadvantage.

“There are some niche areas of banking where you need very acute expertise that will not be covered heavily by the investment banks anymore,” said Lowy. “It’s a logical evolution.”

TALENT CONTEST

Global banks face another challenge: talent. Before 2008, competition for staff was intense, and the key question for international banks was whether Asia could provide the homegrown talent to support their expansion plans. Ten years later, the whole industry is struggling to attract – and retain – top performers.

Regional Rivals

The regulations imposed in the aftermath of the global financial crisis and rogue trading scandals transformed the way investment bankers are paid and incentivised. The days where individuals could expect cash bonuses worth several times their base salaries are gone: in some countries regulators impose a cap of no more than twice base pay, while others require payouts to be made in stock over several years or subject to clawbacks if wrongdoing or trading losses are discovered further down the line.

Rather than bring banker pay in line with other industries, Lowy believes this led to an enormous inflation of base salaries for senior staff, creating another challenge to the traditional banking business model.

“A very large percentage of staff in banks are paid what CEOs earn in other industries, and that’s just plain wrong,” said Lowy. “That is an incentive for senior people not to go anywhere else, but it means there is little money left for the younger staff.”

“For younger talented individuals who want to build a business, be opportunistic, take the initiative, they want to be working for a tech firm, or a privately held enterprise like ours.”

Faruqui at ANZ says the talent in the industry is changing, but he argues that the “brain drain” from investment banking to buy-side funds, emerging industries such as financial technology or other start-ups has been exaggerated.

“Of course, everyone wants to work on the next big deal, but intellectually this is the most exciting time in my entire career. The changes we’ve made and the initiatives we’re involved in are some of the most interesting things I’ve ever done,” he said.

“Bankers will look different 10 years from now and banking teams will be composed of data scientists, more creative people, more innovative – more entrepreneurial.”

Finance remains a sought-after career choice for thousands of young graduates, but, as one former investment banker puts it, the connected offspring of Asia’s political elite – the princelings – are now joining technology firms, not banks, in search of a better lifestyle as well as the chance of future riches.

Laskowski recalls a similar experience in the late 1990s, during the rise of the dotcom era, which came to an abrupt end when the bubble burst.

“People only see the success stories,” he said. “I see those too, but I also know a lot of smart guys who don’t make it work – and there’s a lot more of those out there.”

“It means changing the mindset and culture, changing our systems and our architecture, changing the kind of people we have. It means recognising that it’s a different world out there today.”

The younger generation’s shifting priorities and familiarity with technology can also present opportunities for banks as more of their clients explore new investments and new ventures grow.

“We’re involved in numerous family-level dialogues on what to do next,” said Laskowski. “With the younger generation coming through and the opportunities around the new economy, people realise they have to adjust their business models for this digital disruption.”

“The adoption rate of the Asian consumer is amazing,” he said. “They are picking up these new technologies at incredibly rapid rates.”

Asia’s local banks are not immune to the impact of technology, or to other pressures on the established business model.

Capital adequacy rules have become a problem in India, where greater disclosure on non-performing loans and the transition to Basel III standards have forced banks to raise capital or cut back on risk-weighted assets. In China, analysts say the arrival of TLAC rules will force the country’s biggest banks to adjust their business model. Rather than relying on deposits to fund loans, the TLAC framework requires the most systemically important banks to issue billions of dollars of loss-absorbing debt as a buffer to protect depositors and taxpayers in the event of a crisis.

China’s Big Four banks have an extension to 2025 to meet TLAC requirements, but the scale of the shortfall – US$1trn by some estimates – raises questions over how they plan to supplement their income to cover the additional interest expenses.

There is no doubt that the traditional banking model is under pressure, but those who have stuck with the industry are confident that they can make the changes needed to thrive in the new economy.

“Banks can survive if they adapt to the new environment, and that comes in different forms,” said Faruqui at ANZ. “It means changing the mindset and culture, changing our systems and our architecture, changing the kind of people we have. It means recognising that it’s a different world out there today.”

For other articles in IFR Asia’s 20th Anniversary report please click here . To read the digital version of this report please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com .

| Table of IFR Asia Award Winners | |||||

|---|---|---|---|---|---|

| Table of IFR Asia Award Winners | Bank of the Year | Issuer of the Year | Bond House | Equity House | Loan House |

| 1998 | Citibank | ADB | HSBC | Goldman Sachs | Citibank |

| 1999 | Citibank | Republic of the Philippines | Merrill Lynch | Merrill Lynch | Citibank |

| 2000 | Morgan Stanley | MTR Corp | Morgan Stanley Dean Witter | Morgan Stanley Dean Witter | Citibank |

| 2001 | Citibank/ | Hutchsion Whampoa | JP Morgan | Merrill Lynch | JP Morgan |

| Salomon Smith Barney | |||||

| 2002 | Citigroup/ | Korea Development Bank | Citigroup/ | Goldman Sachs | Citigroup/ |

| Salomon Smith Barney | Salomon Smith Barney | Salomon Smith Barney | |||

| 2003 | UBS | Hutchison Whampoa | UBS | UBS | DBS Bank |

| 2004 | Citigroup | Export Import Bank of Korea | Citigroup | Goldman Sachs | Citigroup |

| 2005 | Deutsche Bank | Foster’s Group | Deutsche | UBS | Citigroup |

| 2006 | Goldman Sachs | Reliance Group | Deutsche | UBS | Citigroup |

| 2007 | Deutsche Bank | ICICI | Citigroup | UBS | Citigroup |

| 2008 | HSBC | Export-Import Bank of Korea | HSBC | UBS | RBS |

| 2009 | JP Morgan | Noble Group | Deutsche Bank | UBS | Standard Chartered |

| 2010 | JP Morgan | Republic of the Philippines | Deutsche Bank | Goldman Sachs | HSBC |

| 2011 | Citigroup | Cheung Kong (Holdings) | HSBC | Goldman Sachs | ANZ |

| 2012 | Goldman Sachs | Alibaba Group | HSBC | UBS | ANZ |

| 2013 | UBS | China Petrochemical Corp | JP Morgan | UBS | Standard Chartered |

| 2014 | Citigroup | Islamic Republic of Pakistan | HSBC | Goldman Sachs | Standard Chartered |

| 2015 | HSBC | Reliance Industries | Citigroup | Morgan Stanley | Deutsche Bank |

| 2016 | Morgan Stanley | DBS | HSBC | Morgan Stanley | HSBC |