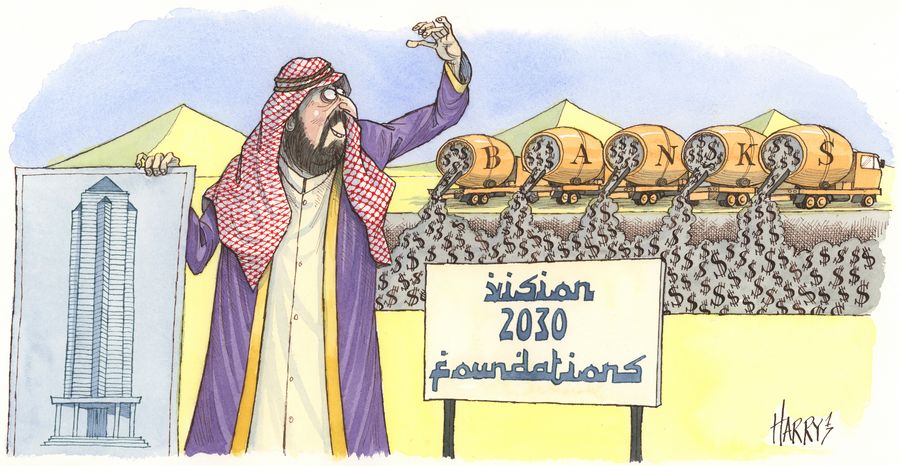

Grand plans to transform Saudi Arabia’s oil-focused economy have caught the attention of every major bank over the past year. But many could be in for a long wait as they seek returns on the resources being lavished on the country.

Saudi Arabia struggled to balance the budget through most of the 1980s and 1990s. But then, in 2003, with the country on the verge of being downgraded to junk because of its soaring national debt, its fortunes suddenly changed. The price of oil – the kingdom’s biggest export – rocketed, and began a long climb that would rain riches down on the country, funding what was to be a golden decade.

By 2012, oil revenues had swollen to US$305bn a year – five times what they had averaged before the boom. Flush with cash, the government spent freely, quadrupling its budget, and creating over a million new public sector jobs. GDP doubled, the national debt was paid off, and US$745bn of reserves were put aside for a rainy day. Saudi, once a debtor nation, became a major global creditor.

The good times are now over. An ill-judged attempt to kill off US shale drillers by ramping up production, and a subsequent attempt to shore up falling prices have hit Saudi hard. Oil revenues, the source of almost all government revenues, are down 70%. The deficit is almost US$100bn a year. Cash is so tight that businesses in the kingdom complain that bills sent to the government often go unpaid for months.

Riyadh, in a bid to fill that hole, has already spent US$260bn – one-third of its reserves. It is also once again a borrower: over the past two years it has borrowed US$39bn from the global bond markets and US$10bn in bank loans. It’s also launched a programme to sell off up to 150 state-owned companies. The process could raise US$300bn for Riyadh – and force major change on the way the economy is run.

“Saudi Arabia has been through challenges: it now realises that the economy has to diversify away from oil, and that it needs to attract capital from abroad,” said Steve Drake, head of Middle East capital markets at PwC. “It’s going to be a major shift culturally, organisationally and strategically, of the Saudis being subjected to very different stakeholders with very different expectations.”

CAPITAL MARKETS

Saudi hopes that the privatisation process, as well as raising much-needed revenue for the government, will also help bolster local capital markets at a time when the country needs to attract capital. As well as the financial pressures, the kingdom faces some big social challenges, including the need to provide work for the 4.5m Saudis expected to enter the workforce over the next decade.

The government is well aware that the current economic model is insufficient to absorb a glut of workers. The public sector employs two-thirds of Saudi nationals and provides 81% of household income. With public sector finances under acute pressure, the government needs to strengthen its private sector, which in turn needs capital to invest, grow, and put Saudis to work.

But the kingdom’s capital markets in their current state are likely to prove insufficient to fund the US$4trn of investment that McKinsey says is needed over the next decade. Trading activity on the country’s Tadawul stock exchange has fallen by two-thirds over the last few years, to just US$1bn a day. This year, equity issuance has fallen to its lowest in more than a decade.

“The government realises that it needs to get private capital flowing, and that it needs to dramatically boost liquidity in its domestic capital markets,” said a regional head at one major global bank. “The state has had to lead all major investments in the past, but now there is a need for the private sector to play a much bigger role. The appetite for change is real.”

Already this year, the kingdom has overhauled the regulatory apparatus in a bid to entice foreign money in and increase liquidity. Rules that heavily restricted the presence of foreign investors in the country have been eased, while the stock exchange has moved its settlement processes into line with global norms and allowed covered short-selling for the first time.

Recent rule changes have specifically been driven with one particular target in mind: index provider MSCI. In June, MSCI confirmed that Saudi’s reforms had been sufficient for it to be placed on track to join the flagship emerging markets index. The process is likely to take a couple of years, but is expected to increase liquidity markedly. Indeed, bankers say that investors are increasingly looking at the kingdom.

“People are eagerly waiting for the MSCI inclusion of Tadawul and have already started preparatory work to allow them to participate,” said Tamim Jabr, chief executive of Deutsche Securities Saudi Arabia. “Investors are closely looking at the kingdom’s privatisation programme….we anticipate that a number of international corporates as well as private equity players to be actively seeking acquisitions in Saudi.”

DEJA VU

To be fair, the kingdom has been – at least partially – down this road before. When the government privatised and sold a 30% stake in Saudi Telecom in a US$4bn deal in 2003, many hoped it would be the start of a flood of privatisations. As many as 80 potential IPO candidates were named but, as the oil wealth began to flood in, those deals were pushed further and further out – and then later cancelled.

Those hoping for an imminent deluge of deals are set for disappointment, however. Consultants working to prepare potential candidates for IPOs say much work is needed to overhaul corporate structures and culture. In some cases, SOEs have been run as extensions of government, with all manner of revenue and cost streams that need to be disentangled from the corporate operations before the deals can come to market.

“The privatisation plan will take some time…t o prepare these entities for listings, and the process normally has a long lead time,” said Drake. “Many of them won’t be ready for at least a couple of years. They need to completely adjust to a whole new world of enhanced disclosure, of enhanced governance, and in some cases of being separated financially from the wider Saudi state.”

Jabr agreed. “It is common for a privatisation process to take two or three years and sometimes more, this is mainly due to the amount of restructuring and corporatising needed at these entities,” he said. ”They only have one shot and the government wants to ensure that they do things right the first time around.”

HARD WORK

Aramco is a prime example of where hard work is needed. Although the oil giant is financially sophisticated, the SOE is also heavily involved in the financing of much non-oil work, including the provision of healthcare and social housing. People close to the company say much work is being done to disentangle financials, with a view to publishing accounts early next year. An IPO could follow in late 2018.

The oil price has recovered of late – it is now double the level when the privatisation programme was first announced. Still, most are convinced the government won’t about-turn as it did a decade ago. Bankers are optimistic that the deals will happen eventually, and are committing financially, building up their presence in the country and lending aggressively to curry favour and build relationships ahead of deals.

How soon they happen, and whether the Aramco IPO will come next year, is an open question. But bankers say the privatisation plan – part of the wider Vision 2030 overhaul of the kingdom’s economy – has already changed attitudes.

“One of the main changes I have seen over the last few years is a much greater willingness to take advice on board,” said the regional head. “Clients in the kingdom are more open to being educated. The rush of banks into the country has been beneficial.”

To see the digital version of this review, please click here.

To purchase printed copies or a PDF of this review, please email gloria.balbastro@tr.com.