Singapore and Hong Kong look poised to allow shares with weighted voting rights in a bid to attract more listings from the new economy. But will it change anything?

After the latest run of hot IPOs, there is no doubt that technology is now the Asian equity investor’s sector of choice. The listings of ZhongAn Online P&C Insurance and China Literature in late 2017 caught the imagination in Hong Kong, with hundreds of thousands of retail investors piling in with orders. By first-day performance, the November debut of online publisher China Literature was the city’s hottest major listing for two decades.

Investors in the region are crying out for more opportunities to invest in fast-growing businesses, even welcoming companies that have yet to turn profitable. The surging interest makes it clear why Asian stock exchanges are so keen to attract more technology companies to list on their bourses, rather than the US.

The reforms deemed necessary to ensure that Asia companies choose to list in their home region, however, are proving controversial.

Hong Kong and Singapore’s exchange operators have each tabled proposals to allow listings from companies with dual-class shareholding structures – a popular feature in the technology world.

The Singapore Exchange tabled proposals in February to accommodate weighted voting rights, subject to certain provisions, and clarified in July that it would allow secondary listings from companies with a dual-class share structure that are primarily listed in any of 22 developed markets – as defined by index providers FTSE and MSCI.

In June, Hong Kong Exchanges and Clearing revived plans to allow dual-class shares in a concept paper on the creation of a new third board. The Hong Kong government has since weighed in on the debate in favour of allowing dual-class structures on the exchange’s Main Board, and the exchange plans to publish its response to the consultation process by the end of the year.

Both exchanges are expected to push ahead, but there are questions that need to be answered. Will the proposals attract more listings? What safeguards are required to protect minority investors? Will it trigger a race to the bottom in corporate governance standards? And, with Hong Kong-listed Tencent crossing a market cap of US$500bn in November, are reforms even necessary at all?

NO THIRD BOARD

HKEx’s proposals outlined the creation of a new third board for new economy companies, split into two segments.

These are the New Board Pro, targeted at early-stage companies that do not meet the current listing criteria, and the New Board Premium, which is for more established companies that are ineligible to list in Hong Kong because of their corporate governance structures.

Both would allow companies to sell shares with weighted voting rights.

HKEx also said it would accommodate secondary listings from firms with unequal voting rights.

The Hong Kong government has since hinted that it would drop plans for a third board to allow companies with dual-class structures to list on the Main Board through the creation of a special chapter.

“The first principle adopted is that perhaps we do not need to create a new board for these purposes, but instead, in the listing rule set up a new chapter,” Financial Secretary Paul Chan Mo-po said in November.

The latest comments have been welcomed by most market participants.

“My initial feeling is that it’s a sensible route forward,” said Keith Pogson, senior partner for financial services at consultancy firm EY.

Bankers pointed out that the purpose of the proposals was mainly to attract secondary listings from some of the large Chinese tech firms such as Alibaba. Listing on the Main Board would be a more attractive option for them than a start-up board with limited liquidity.

Still, there is a concern that by scrapping the third board, Hong Kong will need to do more to attract start-up firms.

James Fok, HKEx’s head of group strategy, declined to comment on the specific proposals since the conclusions to the concept paper have not been published, although he said that HKEx should do more to attract fast-growing start-ups.

“It’s certainly the case now that if you look at the price-to-earnings multiples of the [technology] companies listed here, Hong Kong is as competitive as any other jurisdiction, which has helped attract technology firms,” he said.

“But I do acknowledge that we should do more to accommodate certain types of companies, particularly those at the pre-revenue stage. We haven’t so far developed a sufficient ecosystem around certain sectors, such as biotech, to support these companies listing.”

SGX PROPOSALS

SGX rolled out its consultation on weighted voting rights in February, although so far has not given much indication of how it will proceed.

Mohamed Nasser Ismail, SGX’s head of ECM for small and medium-sized enterprises and head of capital markets development, declined to comment on the timing and specific rule changes, but pointed to a number of steps SGX has taken to attract tech listings.

In October, SGX agreed to acquire a 10% equity stake in CapBridge, a capital-raising platform for early-stage companies.

In an apparent nod to Nasdaq Private Market and with the number of tech companies that are delaying going public due to the abundance of VC funding, Nasser said that CapBridge would eventually offer secondary trading as well as primary fundraising.

In October, SGX also announced its tie-up with Nasdaq, with the aim of facilitating concurrent listings on the two exchanges.

“The tie-up with Nasdaq is a reflection of our thinking about how we can facilitate companies in Asia who wish to access markets beyond the region,” said Nasser.

“For those companies that are deemed too small for the US market, there is a potential to get lost. These companies can access capital here and when they’re ready, bulk up and we will facilitate their transition to the US.”

Nasser argues that Singapore remains competitive as a listing venue.

“The level of interest for companies to consider Singapore as a listing venue has intensified in recent months,” he said. “This goes hand-in-hand with the vibrancy of the market and the valuations that some of the more recent listings have achieved.

“This year, we had Y Ventures, a data analytics company, list and they’ve performed well since then.”

SGX, however, suffers from relatively low trading volumes and its lack of proximity to mainland China compared with Hong Kong. This year, two Singapore-based tech companies, Razer and Sea, opted to list in Hong Kong and the US, respectively.

“I think there are compelling reasons to list in different jurisdictions, but most of our conversations lately have centred around either Hong Kong or New York,” said Randy Gelber, head of technology, media and telecommunications for Asia-Pacific at UBS.

INVESTOR SAFEGUARDS

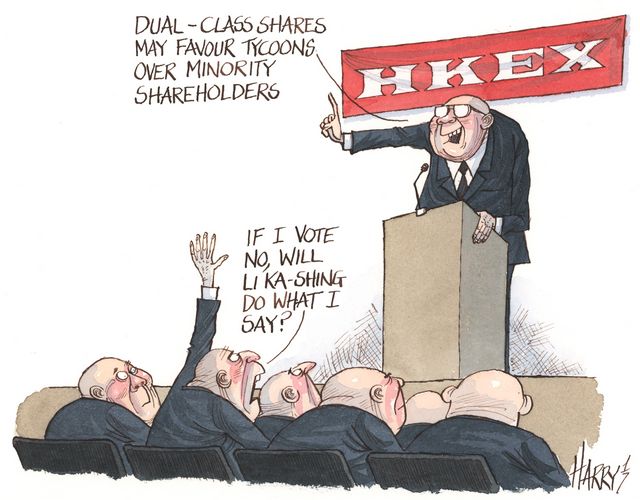

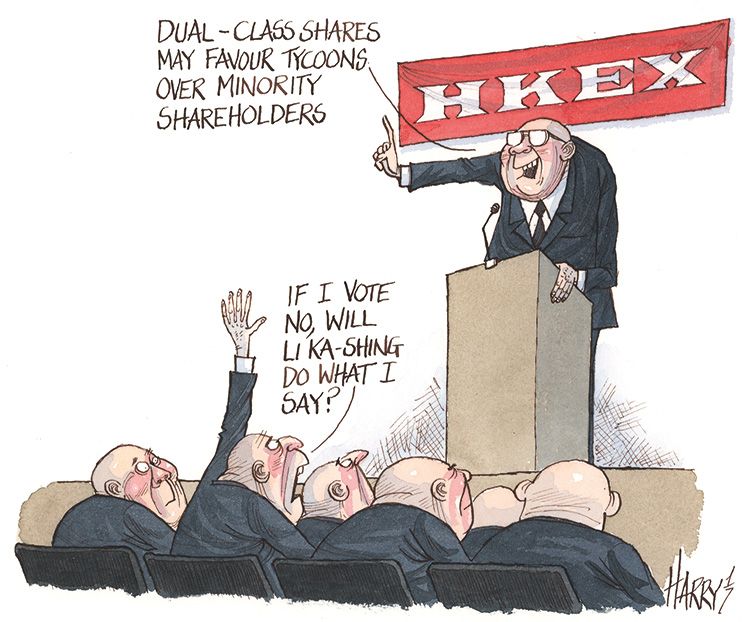

The debate over the merits of dual-class shares has polarised debate, generally pitting bankers, lawyers and accountants on one hand against investors and corporate governance advocates on the other hand.

Some of the feedback has been particularly critical. David Webb, an activist investor and former HKEx director, used scatological terms to refer to the exchange’s proposal for a third board in his submission to the consultation, made public on his website.

In April, the Asian Corporate Governance Association, a trade association representing asset management firms such as BlackRock, Fidelity International and Allianz Global Investors, hit out at SGX’s plans, stating that the reforms would be “damaging to the overall market”.

“The problem that people from the investment community like me have is that the proposals largely speak to the needs of issuers and intermediaries,” said Melissa Brown, partner at Daobridge Capital, a China-focused investment and advisory firm and former member of the Hong Kong Listing Committee.

“They don’t speak to the need of investors, who value the concept of one share, one vote as it’s the only thing that gives a long-term investor a voice at the table.”

Both HKEx and SGX have floated the idea of safeguards to ensure minority investors are protected. These proposals include sunset clauses, where the split voting falls away after a certain period of time, more stringent disclosure requirements and minimum market capitalisation thresholds.

Most investors, however, are unconvinced that these proposals would work.

“Perhaps, if there are ‘appropriate safeguards’, we could do away with electing people to [Hong Kong’s] Legislative Council, too, and leave the government to run everything,” said Webb. “There’s a method to their madness.”

More to the point, if Hong Kong is already an attractive listing venue for the new economy, this raises the question of why bother changing the rules at all?

The recent flurry of new economy listings – from the likes of Razer, ZhongAn, China Literature and WuXi Biologics – has put paid to the idea that Hong Kong is unable to compete with New York on valuations and liquidity.

“We’ve certainly got the wind in our sails,” said HKEx’s Fok. “There’s no doubt that sentiment is strong, which has helped generate interest, but we need to be cognisant that these things are cyclical. It’s about making sure we have the right policies and rules in place to build our share over time.”

Jason Cox, head of equity capital markets for Asia-Pacific at Deutsche Bank, shares the positive sentiment on Hong Kong.

“To the extent that there is a valuation differential between Hong Kong and the US, this tends to be more for smaller early-stage companies or certain sub-sectors,” he said.

Opponents of the proposals argue that scrapping one share, one vote increases the risk of corporate governance scandals. HKEx has a chequered history with some mainland firms that have listed in the city, with high-profile recent episodes involving Hanergy Thin Film and China Huishan Dairy.

One market observer dismissed this argument altogether.

“Practically speaking, what do Asian stock markets look like? They’re generally made up of companies that are majority owned either by the Chinese government or well-to-do families.”

“There are issues around corporate governance that need to be addressed, such as backdoor listings, highly dilutive equity raisings and so on, but how much of a difference will weighted voting rights really make? Not much.”

To see the digital version of this review, please click here.

To purchase printed copies or a PDF of this review, please email gloria.balbastro@tr.com.