The green bond market faces an uncertain future after Enel confirmed to IFR that it would ditch its high-profile green bond programme in favour of a controversial new bond format that bankers say could become a new industry standard.

The Italian electricity giant is one of the biggest corporate issuers of green bonds and the news could prove a major blow to the fledgling market if other actual or potential issuers follow the company's example.

Enel has spent the past few weeks in talks with investors in Europe about launching a second bond – to be denominated in euros – directly linked to its sustainable development goals, following the successful placement of a US$1.5bn so-called SDG-linked transaction at the beginning of September.

The new deal is expected to follow in the coming weeks, with Enel telling investors that it and all future transactions will be in the format. "The SDG-bond format is going to replace green bonds, meaning that the SDG-linked format will be used for Enel's future bond issuances," a company spokesperson told IFR.

Up to now Enel has been a regular issuer of green bonds, raising €3.5bn in the format since its debut in 2017.

The new SDG-linked bonds have been badly received by some green investors, with many arguing the format betrays fundamental principles around accountability and transparency. Under the terms of such deals, Enel will be free to spend proceeds however it chooses – even on coal-powered electricity generation.

CLEANING UP

Enel believes the new format is better aligned to its wider strategy. It reasons there is no longer a need to specify how money will be spent – and it will not provide any details about use of proceeds of its SDG-linked bonds – given that the entire company is now geared towards ambitious goals around clean energy.

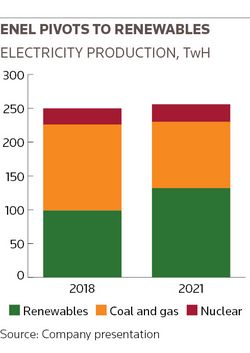

The power producer has committed to increasing its renewables base by 25% by the end of 2021. The addition of 11.6 gigawatts – enough to power 8m homes and equivalent to almost 5,000 wind turbines – will for the first time make renewable energy its main source of electricity.

equivalent to almost 5,000 wind turbines – will for the first time make renewable energy its main source of electricity.

The SDG-linked bonds are directly tied to that commitment and specifically a pledge, made a year ago, to increase renewables to 55% of its installed capacity by the end of 2021 from 48% at present (although actual energy generation using renewables is likely to be lower because renewable plants often operate below capacity). Under the terms of the bonds, the annual coupon will automatically increase by 25bp if Enel fails to hit the capacity target.

FORCED SELLERS?

So what would happen if the company missed that target? Would the bonds lose their ESG label? Would ESG investors be forced sellers? Certainly, some people involved argue that the 25bp step-up is designed to compensate investors for having to sell out. But Michele Cortese, head of Italian DCM at Societe Generale (one of the US dollar deal's eight bookrunners), argues that that would not necessarily happen.

"The bond is labelled as an SDG-linked bond and, even if the targets weren't met, it would remain as an SDG-linked bond. It will be up to investors to decide how they manage their positions," he said.

"It is clearly a much lighter type of structure, but it requires a more complex architecture to achieve this type of objective. The whole company is aligned – this isn't about a few individual projects."

STILL BURNING COAL

But many are not convinced. While Enel is unarguably decarbonising, even after 2021 a large chunk of its electricity will be generated by burning coal and gas. And spending on dirty energy will continue for years. In the first half of this year, for instance, Enel spent around €300m on its coal and gas power stations. The company said it would not be building any new coal power stations in future, and that some of the money spent would be on making current coal plants more efficient - as well as on general upkeep.

"The step-up in the coupon doesn't have any meat to it because they are already committed to reaching that target so the bond doesn't really push them to go any further," said James Hay, an investment associate at Mainstreet Partners, an investment and advisory boutique focused on sustainable finance.

"The step-up in the coupon doesn't have any meat to it because they are already committed to reaching that target so the bond doesn't really push them to go any further," said James Hay, an investment associate at Mainstreet Partners, an investment and advisory boutique focused on sustainable finance.

"Investors aren't interested in having a mechanism to punish companies – what they're really looking for is a carrot, which is the sustainability reporting. Our reward is when a company turns around to us and can identify the impact that our capital is having – that's our double bottom line."

ESG ALIGNED?

But with US$4bn of orders, there was clearly appetite for the new format – so much so that the bond priced around 20bp inside Enel's existing curve. Bankers on the deal say feedback was excellent, with about 70% of allocations going to investors that have an "ESG-aligned" strategy.

Indeed, that grey area of ESG-aligned – but not full-on green – investors have driven a number of recent controversial transactions, including a so-called transition bond from Brazilian beef producer Marfrig in August. The worry is these more generic investors, in their haste to tick a few boxes, look no further than the ESG label and will therefore undermine the true green bond market.

IFR understands that a large chunk of the Enel trade went to a handful of big, generalist US funds that had fallen behind their ESG targets, while bankers on the deal argue that, with a large chunk of money becoming more ESG-sensitive, it makes sense to look beyond pure green investors.

"The way investors are approaching ESG has evolved and is becoming a lot more sophisticated," said Karim Saleh, a DCM syndicate banker at Goldman Sachs (another bookrunner on the US dollar deal). "There is less of a focus on green-bond-only funds, with a much wider umbrella of investments where credits are assessed according to ESG credentials."

OPENING UP THE MARKET

The incentive for banks to open up the market is clear: more issuance means more business. But there is a wider argument that restrictions around use of proceeds in the green market is holding the market back. Issuance, which could reach US$250bn this year, is a tiny fraction of wider bond markets.

Banks argue that, by loosening the rules, more companies will be willing to issue. And if those same issuers make commitments similar to the ones that Enel has made, then that will have a much bigger impact in terms of decarbonising the wider global economy.

"Not every borrower who might consider themselves to be thinking about the environment or thinking about sustainability and social responsibility will be able to access that kind of liquidity because they don't have specific projects to raise a bond against," said Saleh.

Dedicated green investors beg to differ. "Without the strict reporting standards, without the ringfencing of proceeds, how can they really have the credibility to say capital is going toward sustainable activities? I see what they're trying to achieve, but I'm still not sure if it's the best way to do that," said Mainstreet Partners' Hay.

Still, developments outside the bond market could change the game. The European Union, for instance, is drawing up a comprehensive classification system for sustainable activities that many in the green bond market hope will help stop banks and issuers pushing boundaries too far.

"There is definitely a bit of a battle coming up ahead, when it comes to what the market is going to want to buy, and what regulators deem as acceptable products with a green stamp," said Hay.