Jumping ahead

In a year when US domestic mega-deals dominated, Goldman Sachs increased its market share by advising on many of the most heavily contested transactions for both bidders and targets. It is IFR’s M&A Adviser of the Year.

Goldman Sachs has been the dominant force in mega M&A over the decade following the financial crisis. And yet last year was still a vintage one for the bank as it represented clients from industrials to retail. Even Tiffany’s popped the question, engaging Goldman to represent the luxury brand on its proposed sale to LVMH.

Goldman was the only bank that advised on deals with a total value of over US$1trn in IFR’s awards period. The firm notched up US$1.22trn of completed transactions, an impressive rise of 31% on the previous year, according to Refinitiv data.

Its nearest competitor, JP Morgan, managed US$898bn of league table credit and Goldman’s total was nearly double that of fifth-placed Bank of America with US$611bn. Impressively, Goldman increased its market share by 11.5 percentage points, easily the largest increase of any adviser in the top 25.

All this was achieved despite a weaker year overall for M&A, with the total value of deals falling 8.5% to US$3.15trn. The number of transactions dropped 12.9% to 35,092 but Goldman’s tally held up relatively well, only falling 3% to 360 and making it the most active adviser globally by number of deals as well as by total value.

Of the six major deals that involved a bidding war, when a hostile buyer muscled into an agreed deal, Goldman was involved in five of them, arguably the most complex and high-profile mandates available.

“It’s hard enough getting two companies together. But when there's a third that's jumped into the equation, it gets to be three or four-dimensional chess,” said Michael Carr, Goldman’s global co-head of M&A, alongside Gilberto Pozzi and Dusty Philip.

“Clients want an adviser who's been around the track. People come to us for our experience and our ability to think outside the box. We've been fortunate that way in terms of how people think about us and where we can weigh in on particular situations.”

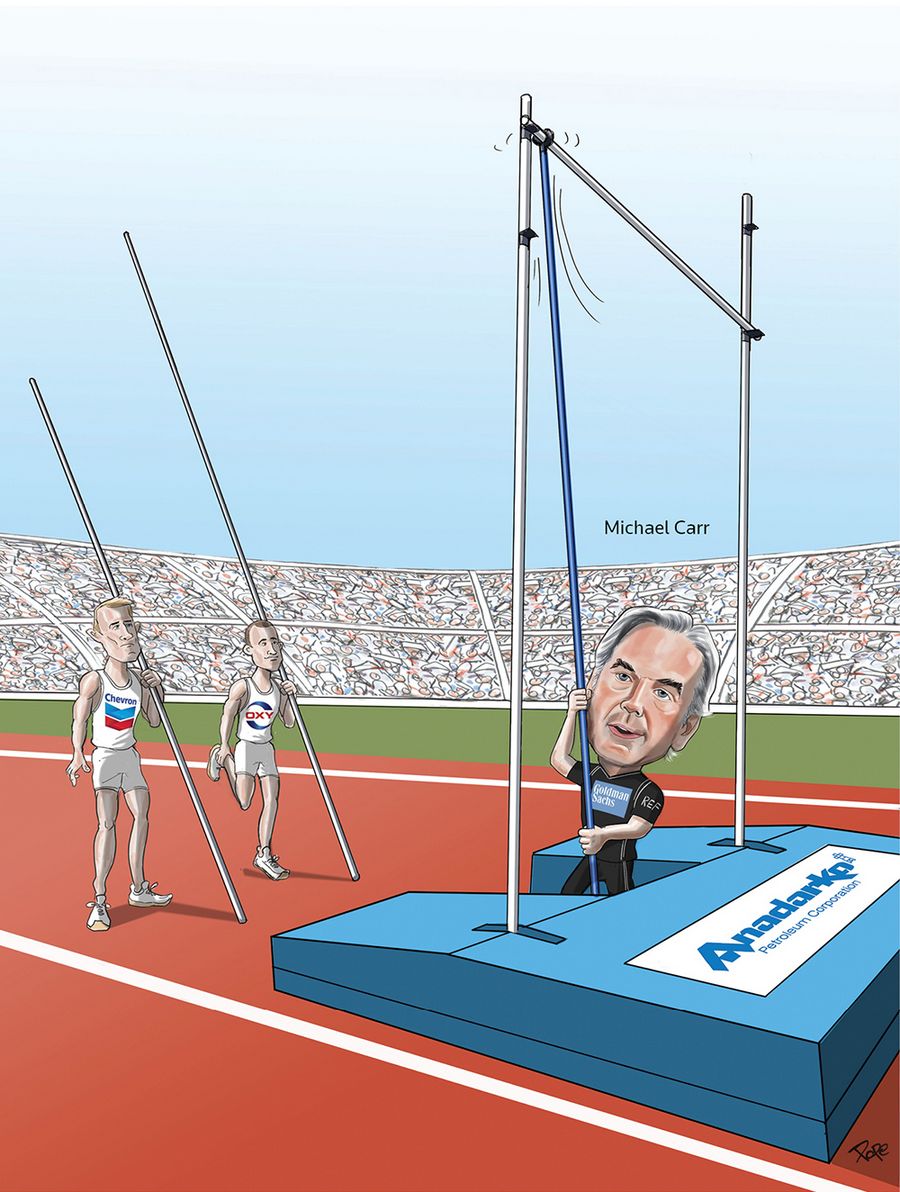

One of the most dramatic of these situations was the sale of Anardarko. Goldman acted for the oil and gas producer with shale assets in the Permian basin. Originally, the company agreed to a US$33bn offer, principally in cash, from sector major Chevron.

But within weeks of that agreement being announced, Occidental Petroleum managed to trump Chevron’s offer after Warren Buffett’s Berkshire Hathaway vehicle agreed to back a higher US$38bn bid with a US$10bn cash pledge. However, the majority of Occidental’s offer was shares.

That put Anadarko and its advisers in a dilemma. Chevron indicated that it was not prepared to raise its offer, believing its predominantly cash bid would ultimately be superior to Occidental’s largely share-based alternative, since it was more assured.

Anadarko’s shareholders took up the Occidental offer, which, thanks to Buffett’s contribution did not require backing from Occidental shareholders. That was seen as a controversial move.

Was the cash offer a better deal? With cash, the sellside adviser can walk away content that the price paid marks the success of a deal. With stock the ultimate success of the transaction is less certain.

Since the deal closed the combined entity’s shares have fallen, sparking pressure from serial activist Carl Icahn for Occidental management to reverse the decline by accelerating its plans to sell assets to help reduce debt incurred from the Anadarko deal.

STRIKING GOLD

The bank had a clearer view when it came to gold.

Goldman advised Newmont Mining on its defence from Barrick Gold’s unsolicited US$18bn offer in February. Barrick, which itself had just bought Randgold to create a US$23.5bn company, intervened just after Newmont had proposed its own US$10bn merger with Goldcorp. Barrick had hoped to stop that deal and instead consolidate with Newmont.

“This was a stock-for-stock deal where Newmont was buying Goldcorp in a friendly transaction. Along comes Barrick, which suggested, unsolicited, a merger of equals. Suddenly we find ourselves in a three-way situation,” said Carr.

“And so in the same chain of transactions where we are acting for a buyer, we are now defending Newmont.”

Discussions engineered by Goldman led to Newmont and Barrick agreeing to set up a joint venture for their extensive Nevada gold mining assets. That meant by working together they could still cut out overlapping costs in this area but remain two independent entities. And Newmont could still buy Goldcorp.

Rarely has a hostile approach ended up with the two warring parties collaborating to create a joint venture in their most competitive area. “I thought it was a pretty ingenious solution to resolve the situation, where all sides win,” said Carr.

NOT JUST JUMBOS

Goldman has been at the centre of the largest deals this year but it has also made its presence felt in smaller deals.

“We obviously want to do the biggest deals for the biggest clients,” said Pozzi. “But more and more we are trying to advise clients on new ideas: finding deals that make sense for them – that help them grow – and giving them support to unlock the deal.”

Among those “smaller” companies was France’s CMA CGM, the world’s fourth largest container shipper. The company, owned by the Saade family, launched an unsolicited cash offer to buy out other shareholders of Swiss freight forwarder Ceva Logistics, valuing it at US$1.67bn.

It was an aggressive move offering roughly the same economics as rival bidder Danish freight company DSV, whose overtures had previously been rejected.

“It was a hotly contested transaction, and we were in the room every step of the way,” Pozzi said.

CMA owned 33% of the listed shares but DSV was still very interested in buying the company putting the two at loggerheads.

“DSV was much larger than CMA and had more financial flexibility but tactics played a crucial role,” Pozzi said.

CMA got its deal across the line and took control of Ceva.

FAMILY FOCUS

The deal also shows that the bank with the largest share of M&A deals is not only interested in banking US$100bn companies but also helping family businesses grow. “It’s becoming more a theme for us,” Pozzi said.

Many banks tout their role as trusted adviser but Goldman demonstrated in 2019 that companies wading into M&A as either buyer or seller have consistently turned to them for counsel.

Even other banks have sought the firm’s advice. Goldman advised SunTrust as it sold itself to BB&T for US$28.3bn, the largest bank transaction since 2005. The banks agreed to merge in an all-stock deal to form the sixth largest US commercial bank.

On the buyside Goldman was a key adviser to the London Stock Exchange Group as it pursued IFR owner Refinitiv with a US$27bn offer, potentially the largest exchange group deal ever and the third largest acquisition of a private company.

Goldman claims credit for leading the deal, since LSEG chief executive David Schwimmer is a 20-year Goldman alumnus. On Goldman’s side, the bank said the deal represents its ability to bring clients fresh ideas on the buyside.

“More and more we are trying to advise clients on new ideas – that’s critical,” Pozzi said.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@refinitiv.com