Comeback kid

Political volatility and a ratings downgrade made for a tumultuous 2018 for the Republic of Italy. But in 2019, not only did the sovereign return to capital markets, but it did so with flair, bringing record-breaking syndications and an electrifying US dollar comeback, making it IFR's SSAR Issuer of the Year.

By the time Moody's cut Italy's rating to Baa3, just one notch above investment-grade, in October 2018, European bond markets had been feeling the full force of sovereign-led volatility for months.

An unexpected alliance between the anti-establishment Five-Star Movement and far-right League following March 2018 elections had made for a fiery and disruptive mix.

But while the elections troubled bond markets, it was not until a row escalated between the government and the European Commission over the country's 2019 budget that matters came to a head.

The spat eventually resulted in the one-notch ratings cut in mid-October, with Moody's citing Italy's material shift in fiscal strategy paired with significantly higher budget deficits planned for the coming three years compared to previous expectations.

"Looking back at November 2018, the picture was very different [to now]," said Davide Iacovoni, director general in Italy's treasury.

"Italy at the time was engaged in very troublesome discussions with the European authorities, specifically the European Commission. Of course, things were not easy."

Trying to address some of this volatility was crucial for the sovereign given that it had an estimated €255bn of gross funding needs for the following year.

Difficult markets for the most part of 2018 also meant that the issuer had only conducted one institutionally targeted syndication that year, opting instead for less headline-grabbing auctions.

"We were trying to be as predictable and as regular as possible but at the same time, we were using all our tools," said Iacovoni.

"We did several exchanges and buybacks to help smooth the redemption profile for 2019 but at the same time, with the aim of smoothing some dislocations in the market, anchored as much as possible the short-end of the curve."

In early December 2018, the sovereign did a €3.2bn tap of the 2.3% October 2021 BTP alongside an accelerated tender offer that saw the sovereign buy back an equivalent amount of five other bonds.

GAME-CHANGER

But the game-changer came when the commission reached a deal with Italy over its 2019 budget, avoiding disciplinary steps against Rome.

"At the very end of December, we had a final agreement on the budget, which was approved by parliament," said Iacovoni. "And as we went into January, apart from the first few days when there was some geopolitical noise, market conditions were very good."

From a 2018 high of 3.78%, the yield on the 10-year BTP had dropped to 2.75% by the time the new year opened. The spread between 10-year Italy and Germany had also narrowed substantially over the same period, from 327bp to 252bp.

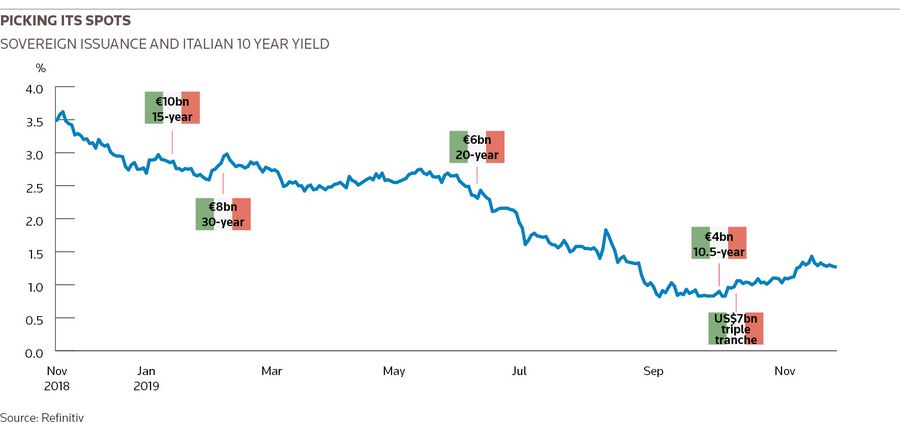

The sovereign was quick to seize on the sharp improvement in market conditions to bring a €10bn March 2035 trade in mid-January that marked the country's return to the syndicated market after a year's absence.

The transaction, Italy's biggest ever internationally targeted syndication, drew more than €35.5bn in orders.

Unusually for the sovereign, it was back in the syndicated market just three weeks later. With memories of 2018 still fresh, Italy grasped the opportunity to raise another chunk of funding.

"We were a bit reluctant to bring a transaction so shortly after the other one," Iacovoni said. "But we were getting strong feedback from the market. Also, at that time, there was a general change of expectations around interest rates given the negative data that was coming out of Germany. There was a general move in the market towards longer maturities."

That was clear to see in the order book for the €8bn September 2049 for which demand peaked at over €41bn.

The shift in expectations followed the European Central Bank meeting in January when president Mario Draghi suggested the ECB could resume its bond purchase programme, which had only just ended and under which the central bank had bought €2.6trn of assets.

RIDING OUT THE STORM

Just when it looked like it was going to be plain sailing for the issuer, volatility reared its ugly head again after the European Commission threatened to open a disciplinary procedure over Italy's public debt in the second quarter.

The renewed row was further inflamed by a government official saying the country may issue small-denomination bonds to help pay state debts owed to companies, with some seeing the so-called "mini-BOT" scheme as paving the way for an exit from the eurozone.

But Italy came out fighting, bringing a €6bn 20-year syndication that attracted more than €24bn demand.

By that point, the ECB's hints that more QE was on the way had become even stronger, with the central bank ruling out raising rates for at least a year and Draghi broadly opening the door to more stimulus.

Still, for Iacovoni, the ECB's role, while very important, should not be overestimated.

"It is the buyer of last resort but it's not crucial in stabilising the market, especially now that it is not buying €60bn–€80bn [a month] anymore," he said.

"At lot of what happens to Italian government debt depends on how the Italian economy and government perform."

Much market relief followed the EC's decision not to open a so-called excessive deficit procedure after the Italian government took action to appease the European authorities and said it would prepare a 2020 budget in line with EU fiscal rules.

"Things really changed," Iacovoni said. "That was an important agreement and avoided the EDP. This was a very strong message to the market. It's important to comply with the rules. More and more, politicians are more aware of this than they used to be even one year, or one-and-a-half years, ago."

Calmer waters meant that Italy was able to bring its biggest institutionally targeted inflation-linked syndication in more than five-years – a €4bn 10.5-year trade linked to eurozone inflation.

ELECTRIFYING MARKETS

After such a strong run in its home market, it was difficult to see how the sovereign would be able to top its trades.

Yet it did just that in October when it priced its first US dollar transaction in almost a decade, a US$7bn deal that re-established the issuer in the currency. It was its sixth institutionally targeted transaction of 2019, exceeding previous years.

The triple-tranche five, 10 and 30-year transaction marked the country's return to the international benchmark debt market after the eurozone sovereign crisis. Italy had not issued US dollars since 2010 and had not done a dual-tranche in the currency since 2003.

The sovereign had to put a collateralisation system in place (as well as the necessary credit support annex documentation) with all its primary dealers for new derivatives, something "complex and extremely burdensome", according to Iacovoni.

But months of work paid off and Italy was able to tap into an investor base that would not normally buy euro paper at little extra cost compared to its domestic market.

"Issuing dollars is a way to engage with investors who wouldn't normally buy our euro debt," Iacovoni said. "We were ready to pay extra given that we had been out of the dollar market for nine years and were rebuilding the curve but that really didn't happen as the interest was so strong. The deal priced more or less in line with BTPs."

That transaction crowned months of work and opens a new funding avenue for 2020 as the sovereign looks to tackle another multi-billion funding programme.

"The size was important. US$7bn was not obvious but what was extremely important was the wide range of new investors who showed up."

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@refinitiv.com