Open for bids

Latin American ECM in 2019 was defined by Brazil, as the region’s largest economy finally hit its stride after moderating interest rates ushered in a new wave of investment. But the rest of the region proved more challenging. For excellence across the continent, Bank of America is IFR’s Latin America Equity House of the Year.

Privatisation of state-owned businesses provided the seed for Brazil’s re-emergence on the global equity landscape this year, a trend that is only in its infancy.

Brazilian ECM issuance over the awards period more than doubled to US$22.6bn, of which US$14.6bn were secondary sales, predominately by government-owned entities. Suddenly moderating interest rates – the benchmark Selic rate stands at a record low 4.5%, down from 14% just three years ago – has seen an influx of foreign investment including into Brazilian equities.

Bank of America was central to that process by participating as a bookrunner on six government sell-downs during the awards year. That included disposal of a US$1.35bn stake in Petrobras in June and a US$2.55bn sale a month later by the state-run Brazilian petroleum company of its former fuels logistics unit, BR Distribuidora.

“Based on discussion we are having with corporations and government entities, we would expect to see R$200bn, or US$50bn–$55bn, of equity issued out of Brazil in 2020,” said Bruno Saraiva, Bank of America’s head of Brazilian ECM. “We are really leading the charge in Brazil among the international banks.”

BofA was a bookrunner on 18 Brazilian equity and equity-linked deals earning league table credit of US$2.4bn, giving it a 10.4% market share. The bank was a global coordinator or stabilisation agent in 16 of those situations, according to Sariva.

Neoenergia’s R$3.7bn (US$972m) IPO in June employed a streamlined underwriting syndicate. After a nine-strong syndicate of banks failed to take Neoenergia public in 2017, the Brazilian utility worked closely with just three banks on its 2019 IPO.

BofA was part of the trio pre-marketing Neoenergia’s IPO to institutions ahead of pricing 208m shares, all secondary and including subsequent exercise of the greenshoe, at R$15.65 apiece, the midpoint of the R$14.42-$16.89 marketing range.

BofA employed a similar pre-marketing strategy for Vivara, a Brazilian jeweller, by targeting the maximum 50 institutions allowed by Brazilian regulators before the IPO filing. The deal was twice covered at launch, culminating in pricing of 85m shares in October at R$24.00 each, the upper-half of the R$21.17-$25.40 range marketed.

Brazil is coveted by global investors for high-growth, disruptive companies, a desire BofA sated with bookrunning mandates on digital payments company PagSeguro Digital’s US$653.3m US-listed follow-on offering in October and a R$4.73bn primary follow-on a month later by retailer Magazine Luiza.

Afya, a provider of post-secondary education focused on medical fields, provided a similar growth angle on its IPO in July that was used to fund acquisitions. Having worked extensively on the company’s acquisitions, BofA earned outsized economics on Afya’s US$300m Nasdaq IPO in July.

BofA earned 35% of the US$18m IPO fees.

On the same night as it was wrapping up Afya, BofA was a bookrunner on a R$7.4bn government selldown in reinsurer IRB Brasil Resseguros as well as NYSE listing/re-IPO of Peruvian commercial bank Intercorp Financial, highlighting diversity across the region that was unmatched.

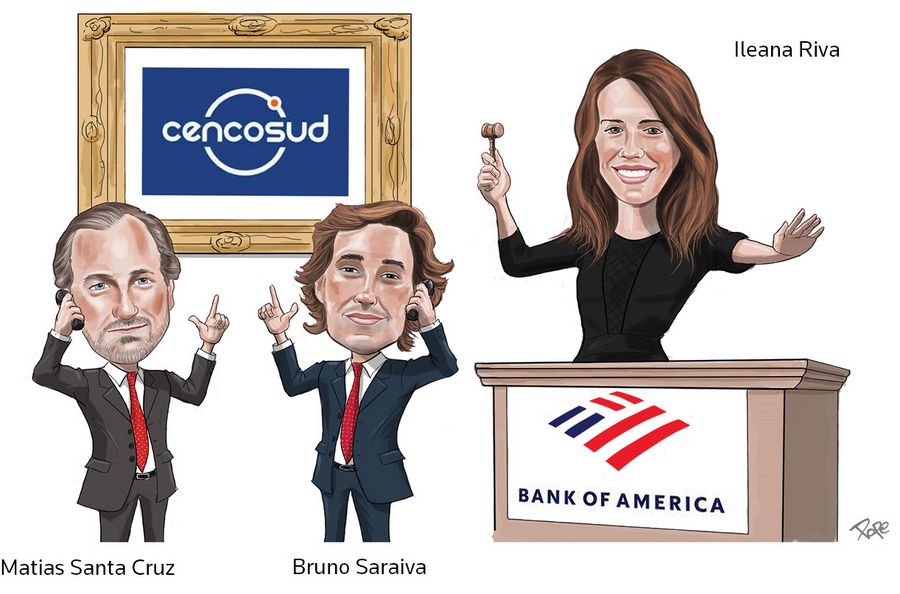

“The whole [Intercorp] deal was placed internationally. There is very limited liquidity in the local market,” said Matias Santa Cruz, who oversees LatAm ECM ex-Brazil.

“Structurally there was a lot of thinking about providing liquidity and closing the valuation discount for selling shareholders.”

Intercorp’s financing, a US$468.6m predominately secondary stock sale, was influenced by the IPO a month earlier for Chilean shopping mall operator Cencosud. Chilean securities laws required that the 472m shares on offer were auctioned off, a format that threatened to crowd out international investors.

BofA, one of two global coordinators on the IPO, devised a strategy to tier the auction process into buckets, including one dedicated to international institutions.

“We had to spend a lot of time educating and making institutions comfortable with the auction process,” said Ileana Riva, a VP on the LatAm ECM team. “There were concerns by some institutions about the demand from Chilean pension plans and local retail.”

The subasta, or auction, saw the 472m shares clear at Ps1,521, toward the lower-half of Ps1,475-Ps1,700 range marketed, with 20% allocated to international investors.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@refinitiv.com