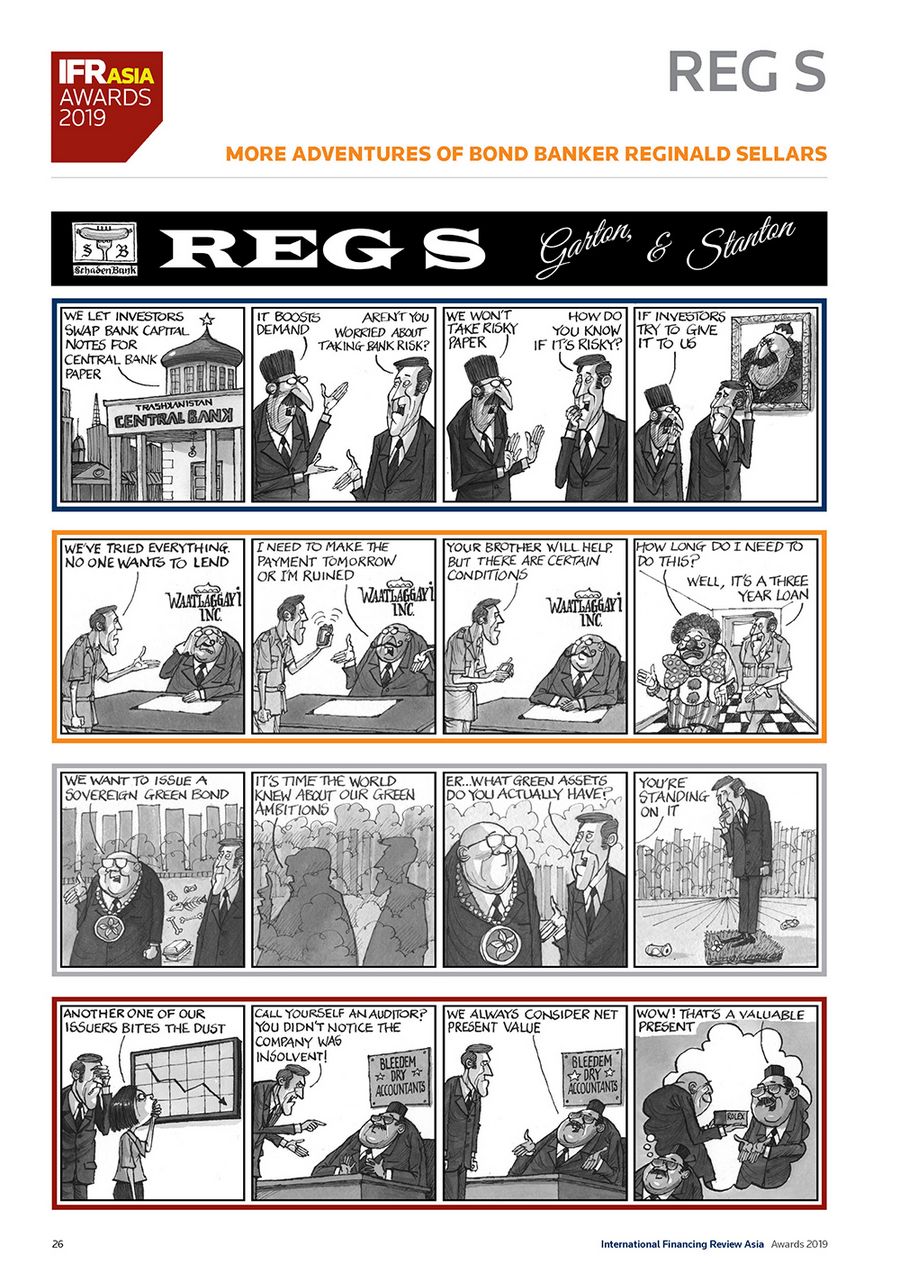

More adventures of bond banker reginald sellars

To see the digital version of this report, please click here

To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

To see the digital version of this report, please click here

To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

When it comes to China, Donald Trump is not shy about taking credit. The US President’s self-proclaimed list of achievements even includes convincing Chinese President Xi Jinping not to send troops into Hong Kong to deal with months of anti-government protests in the special administrative region, according to a rambling interview he gave to Fox News in November. As far-fetched as that may be, Hong Kong’s capital markets probably owe him some gratitude. The Stock Exchange of Hong Kong leapfrogged both the New York Stock Exchange and Nasdaq to...

There is a term in Japanese business circles for a market that has developed without the influence of external forces. Garapagosu-ka, which translates to Galapagosization, takes its inspiration from the quirks of nature found only in the remote Galapagos islands, almost 1,000km off the coast of Ecuador. It is a fitting description for the yen bond market, which has retained its own unique characteristics even as the global markets have evolved to become faster and more efficient. This fondness for isolation, however, is slowly fading. After six...

To see the digital version of this report, please click here To purchase printed copies or a PDF, please email gloria.balbastro@refinitiv.com

To see the digital version of this report, please click here To purchase printed copies or a PDF, please email gloria.balbastro@refinitiv.com

50-year JGBs Too unconventional, even for Japanese policymakers. AONIA A chronic condition suffered by Australian BBSW bankers fearing domination by the local risk-free reference rate. Aramco The world’s first domestic IPO to be preceded by an extensive multi-year global beauty contest. Berkshire Hathaway Your standard ¥430bn (US$4bn) debut Global yen issuer, borrowing for “general corporate purposes”. Blue chips A takeaway meal that has been sprayed by Hong Kong’s water cannon. Bud Light Alternative IPO strategy in case investors...

To see the digital version of this report, please click here To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com