JP Morgan, Nomura and BNP Paribas are among the banks racing to sell the first managed synthetic collateralised debt obligation since the financial crisis, according to people familiar with the matter, with sources signalling that a deal could land in the first quarter of the year.

Such a move would represent a further landmark in the rehabilitation of this controversial breed of structured credit investment that many associate with the kind of excessive financial engineering that led to the financial crisis of 2008.

Volumes of collateralised synthetic obligations – a type of synthetic CDO that carves up pools of credit-default swaps linked to corporate debt, rather than toxic sub-prime mortgages – have surged in recent years as historically low interest rates have encouraged money managers to delve into more complex investments. But a subsequent decline in the returns CSOs offer has encouraged banks to find ways to make them more appealing to investors.

CSOs until now have mainly been short-dated (up to two years in maturity) and static. That means the hedge fund investors that mostly buy these products cannot substitute credits in the underlying portfolio of CDS.

Banks are looking to change that by crafting longer-dated, managed CSOs that would offer meatier yields. Funds including Apollo Global Management and CQS are considering participating if such deals were to come to fruition, sources say.

Allowing the investor in the riskiest portion of the CSO to swap credits in and out of the portfolio should help mitigate the increased risk of defaults that comes with longer-dated investments. These structures would also bear a closer resemblance to the more mainstream collateralised loan obligation market, potentially bringing in a wider range of investors.

"There's definitely a focus on getting the first transaction completed. We're hoping that once we do a managed deal, the investor base can expand – the traditional CLO investors will look at CSOs too," said Sukho Lee, an executive director in structured credit trading at Nomura.

FIRE IT UP

The synthetic CDO machine loomed large over credit markets in the run-up to the financial crisis, helping to fuel the extraordinary growth in credit derivatives over that period. The CDS market expanded more than fourfold in the space of two years to reach a peak of US$58trn in 2007, according to the Bank for International Settlements, before shrinking back to US$8trn by mid-2019.

Synthetic CDOs crammed full of sub-prime mortgages haven’t resurfaced following the havoc wreaked across financial markets over a decade ago. But static and relatively short-dated CSOs have made a comeback in recent years amid a steep increase in the amount of negative-yielding debt, prodding money managers to take greater risks.

So-called bespoke CSO tranche trading reached US$80bn in 2018 and "continues to grow rapidly”, according to a report last autumn from risk and analytics firm Quantifi, referring to products based on hand-picked pools of corporate CDS.

Still, not everyone appears comfortable with the current shift towards longer-dated deals. Citigroup, one of the most prominent banks in bespoke CSO tranches, hasn’t been looking to do a five-year trade, according to sources, due to the increased counterparty risk involved in selling longer-dated deals.

SPREAD COMPRESSION

The move towards longer-dated deals (and the consequent requirement for the reference entities to be managed) is driven by the fact that credit spreads have compressed to near their lowest levels since before the financial crisis. That is partly a result (at least in shorter CDS maturities) of the rise in CSO issuance, as banks have sold CDS protection to hedge their positions.

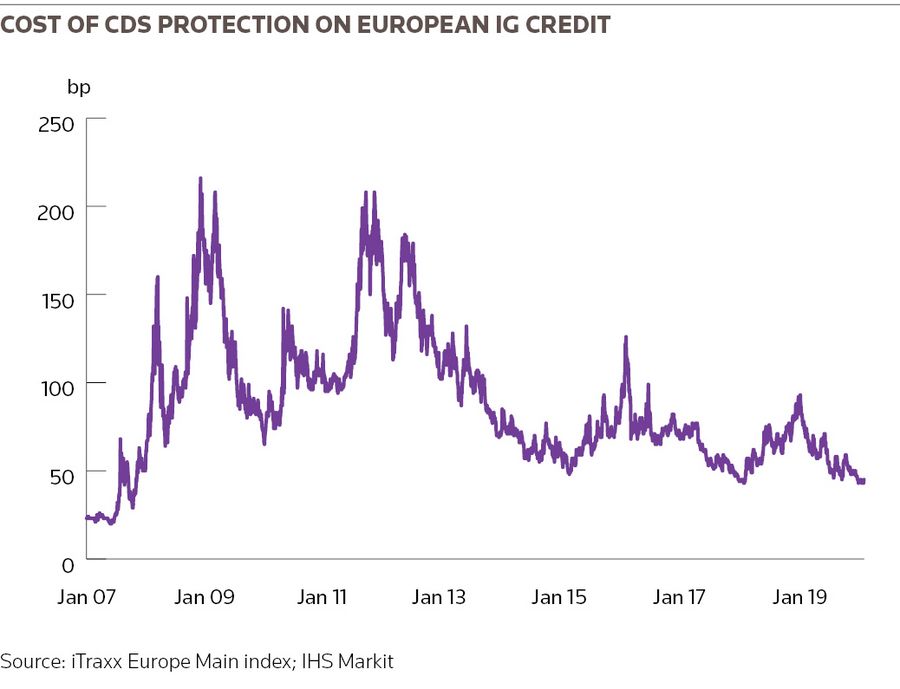

Today, five-year spreads on iTraxx Main, the European investment-grade CDS index, trade at nearly double the level of three-year spreads, according to IHS Markit. That compares with 1.4 times four years ago, showing how much further shorter-dated spreads have fallen during that period.

"Spreads have compressed so much that it's become very difficult to place two-year deals. The five-year product helps execution as you’re trading the more liquid part of the curve, but this obviously brings added risk of losses due to the longer duration,” said Ben Hammond, an executive director in credit structuring at Nomura.

“As a result, equity [investors] in particular are keen to look at transactions where they can substitute names over the life of the trade.”

A typical managed trade might be between US$500m and US$1bn and based on a portfolio of 100 CDS. These CDS will reference investment-grade and high-yield companies across both US and European credit markets. The portfolio is sliced into tranches with differing degrees of risk and return. This is usually an equity tranche and a senior tranche, although some structures may also have a mezzanine tranche wedged in between.

The equity investor will absorb any losses resulting from defaults in the underlying pool of CDS up to a certain level, typically on the first 5% or 10% of the portfolio. To mitigate that risk, the envisaged deals will allow them to switch some CDS in and out, usually less than half of the portfolio over the life of the trade.

HURDLES

There are still hurdles to getting a managed deal out the door. One sticking point is who pays the cost of those substitutions, given it usually involves swapping a poorly performing credit for a better one.

Senior investors appear reluctant to bear costs that could erode the roughly 35bp to 40bp spread they expect to receive on these deals. Equity investors will typically receive a much higher spread – 1,000bp or more – but they may argue that they shouldn’t have to shoulder all the costs for improving the resilience of the entire portfolio.

The low level of spreads could also make it tricky for the banks selling the deals.

“If you have a manager switching names all the time, the dealer will have to manage their backbook by adjusting their hedges. With spreads so tight right now, that could be a pretty expensive exercise for the dealer,” said Christian Adler, co-founder of structured credit hedge fund Astra Asset Management.

“The question is whether they can get the hedge costs and potentially the increased regulatory costs to a level where it all makes sense economically.”

Still, investment banks have a strong incentive to make these deals work so they can keep the CSO machine running. That means it could be a matter of when, not if, the first managed CSO comes back to the market.

"If dealers can demonstrate that it’s not their trading desk selecting the names but credit managers . . . that could help banks get more investors involved,” said Adler.